Still Hearing Echoes

Still Hearing Echoes

Reviewing three months of notes and our outlook

This is the final free weekly note. We will be transitioning to a free summary and full note for paid subscribers format on June 1st. The response to our notes has been excellent, we hope you found the content helpful and hope you will subscribe and won’t miss any upcoming analysis. For those of you that require documentation for your internal process we have a description of our products and pricing invoice we can email at your request. Please send an email to bcknapp@ironsidesmacro.com.

Echoes of ‘88: The Recession that Wasn’t

In this week’s note, we will look back on the last three months and offer our thoughts on the outlook. We began our Ironsides Macroeconomics notes picking up an analog we first introduced in January 2018 at Guggenheim, we originally developed this idea during research at BlackRock in the summer of 2014; we dubbed it ‘Echoes of ’87. In short, there have been three non-recessionary, supply driven 65-75% oil price collapses in the last four decades. After the ’85-’86, ’97-’98 and ’14-’16 oil supply shocks when oil prices stabilized, corporate earnings growth recovered and the stock market rallied 50+% stretching the market multiple to the high-end of the historical range ~20. The drops in energy prices came relatively late in the business cycle and created surprising disinflationary shocks that lowered long term rates, in turn boosting consumer spending on autos and housing. We believe the ‘80s episode is particularly relevant given ’86 tax reform that boosted capital spending but disrupted the housing market for a year. Additionally a new Fed Chairman was tightening policy and hawkish the Reagan administration trade policy included a 100% tariff on select Japanese electronics. Stretched equity market valuation, hawkish monetary and trade policy created an unstable macro environment and the stock market crashed. Like the Crash of ’87, stretched equity market valuations in 2018 were not associated with leverage in the banking system or household sector, so the equity market crashes did not trigger a deleveraging cycle. While there was a transitory wealth effect that slowed consumer spending in 4Q87 and 1Q19, the economic impact of the Crash of ’87 and the 4Q18 stock market collapse were small, and the market recovered to new highs before the business cycle ended.

The calls for a serious 2019 economic slowdown appeared to be based on the median decline in the S&P 500 associated with post-WWII recessions of 21% and a view that the Tax Cuts & Jobs Act was Keynesian demand stimulus late in the business cycle that would lead to ‘overheating’ and a Fed policy mistake. Our Echoes of ’87 analog explains why we do not believe the stock market was a reliable leading economic indicator in 4Q18. Nor do we believe TCJA boosted consumer demand¹, instead a boom in investment in intellectual property products (IPP) and apparent end to the weak productivity conundrum created a supply-side shock that strengthened growth and lowered inflation. We really do not know why the mix of growth effects surprised market participants. Perhaps because for much of 2018 rates were rising, led by the front-end, as the Fed was both tightening conventional interest rate policy and contracting their balance sheet, the ECB was tapering asset purchases and the BOJ was weakening their yield curve control program. In essence investors looked only at the first order effects of fiscal and monetary policy and bought into the new-Keynesian former Fed staff economists spread across investment banks view that TCJA would temporarily boost consumer spending while leading to a more sustainable increase in the rate of inflation. Of course, these forecasts were incorrect; growth was strong due to investment rather than consumption, and inflation slowed. Monetary policy is not tight as evidenced by steepening in the back-end of the Treasury market, negative term premium and stable market-implied inflation expectations (‘breakevens’). Sure higher rates played a role in weaker housing in 2018, but the primary catalyst was disruption related to TCJA². The stock market crash was the eighth monetary policy normalization related correction this cycle, every other cycle had one, underscoring the downside to unconventional monetary policy. Monetary policy wasn’t and isn’t tight, we simply had another uncertainty shock due to unwinding unconventional policy.

¹https://ironsidesmacro.substack.com/p/how-you-doing-joe-6-pack

²https://ironsidesmacro.substack.com/p/housing-another-echo-of-88

Looking Forward – Trade Wars, Confidence, Dynamism and Productivity

By the spring of ’88, the Fed had resumed their tightening cycle and the trade battles continued prompting former advisor Milton Friedman to write that the Reagan administration has been “making Smoot-Hawley look positively benign.”³ The stock market had a series of 6-7% corrections amidst the continued macro instability associated with monetary and trade policy hawkishness. In this context, the selling this May after making a marginal new high as the Trump Trade War heated up seems an appropriate response. While we expect higher stock prices and bond yields later this year, the near term outlook for domestic and global economic data is mixed at best, and though monetary policy is accommodative, trade policy is likely to be hawkish. Still, there is are self-corrective aspects to trade policy; it should become painfully clear to the Chinese Central Committee that their export sector is dragging down the broader economy and targeted stimulus is ineffective. On the US side, the stock market is more closely linked to weak global trade than the economy, the costs of trade are specific, and benefits diffuse as evidenced by the pain in the politically important agricultural sector. Said differently the Trump administration is sensitive to the stock market and the costs of their trade policy being absorbed by the portion of the country the tipped the 2016 election to President Trump.

³https://object.cato.org/sites/cato.org/files/pubs/pdf/pa107.pdf

Confidence, Capex and Barriers to Trade

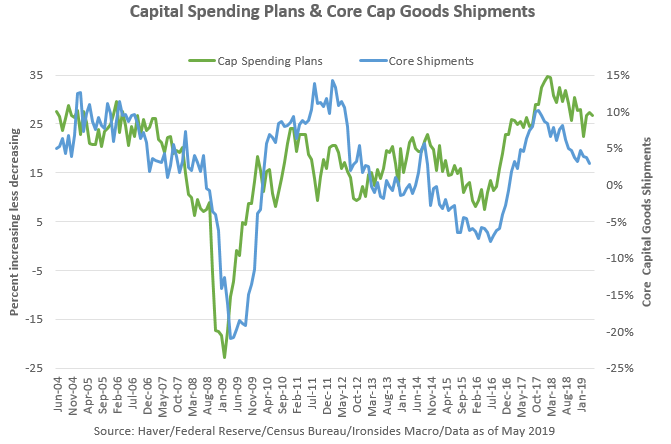

Business confidence, more specifically capital spending plans, have been recovering for a couple of months from the threat of tariffs at year-end and 4Q18 QT crash. It is too early to judge the effect of the breakdown of US/China negotiations; we have seen three of the five May regional Fed manufacturing surveys, strong capital spending plans imply the recovery is continuing, however, the flash Markit manufacturing purchasing managers’ index was soft. While markets have largely corrected for the Trump tariffs and associated retaliation thus far, the risks are growing alongside the size and scope of the tariffs. A 10% drop in the yuan was not disruptive to the Chinese banking system, a 25% drop would likely be globally destabilizing. We would like to make one important point, global trade imbalances were already on their way down well before the 2016 election. China’s current account surplus peaked at 11% of GDP in 2Q07, was 2.8% in 1Q19 after falling to zero in 1Q18. Unit labor cost convergence, rising transportation and energy costs and increased supply chain and exchange rate risks all contributed to global trade growth slowing from twice GDP in the ‘00s to the same rate as growth in the ‘10s. We believe there was only one necessary policy step after markets and prices did the heavy lifting to correct the extreme global current account imbalances that peaked before the global financial crisis, cutting the US corporate tax rate and changing from a worldwide to territorial tax structure. While TCJA triggered a surge in business confidence, trade policy has added to the risks of investment. For example the USMCA investor dispute settlement clause and quotas on unprofitable auto imports from Mexico are barriers to trade and therefore are an offset to corporate tax reform. The secular trend is to produce as close to final demand as possible, TCJA was an important step in making the US an attractive destination for fixed investment, and like the ‘60s and ‘90s when capital investment boomed, inflation volatility is low. Consequently, with these secular tailwinds, we remain confident in our strong capital-spending outlook in IPP, however, barriers to trade are near-term headwinds to the recovery in equipment spending evident in the April durable goods report Friday morning.

Investment in Labor, Subtle Deterioration

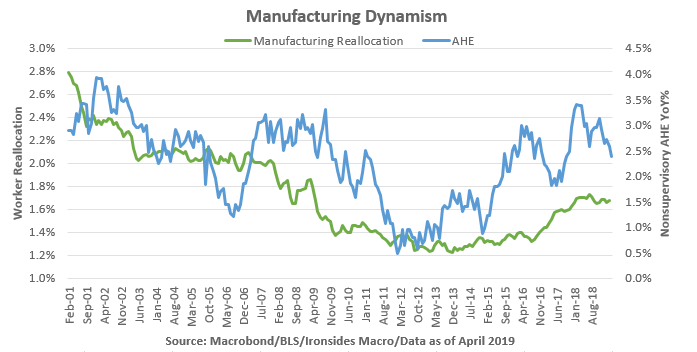

In the minutes of the April 30-May 1, 2019 FOMC meeting the participants “agreed that labor conditions remained strong over the intermeeting period.” We take some issue with their assessment given the deceleration in labor market dynamism derived by taking the quarterly sum of private sector hiring and separations as a percent of the labor force. This measure, also known as worker reallocation, leads wage growth by one year and is positively correlated with productivity. It surged from January through August of 2018 only to retrace 61% of the gains as hawkish trade and monetary policy impaired business confidence. We have been watching manufacturing sector dynamism closely for supporting evidence for our manufacturing renaissance thesis, from December 2000 through December 2013 manufacturing labor reallocation steadily declined. Late in 2016, a very noticeable recovery began that continued until stalling in August 2018. While there has not been much of a retracement, average hourly earnings of nonsupervisory manufacturing workers, which had recovered from 0.5% in early 2012 to 3.4% in March 2018, have slipped back to 2.4%. We suspect trade policy is the culprit. We remain optimistic that labor market dynamism will improve along with business confidence in the coming months, but would note that after August, wage gains due to the surge in dynamism in 1H18 will reverse, and wage growth is likely to stall.

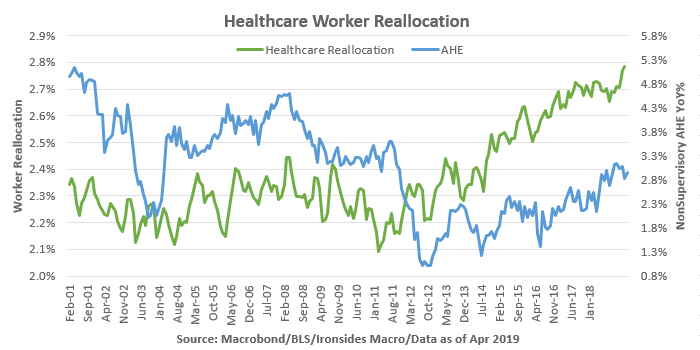

On a more positive note, healthcare sector dynamism is going up significantly. This sector is the biggest contributor to the job openings and hiring gap and is one of the biggest drags on productivity. Because the increased dynamism is due to surging voluntary separations and low firing, healthcare productivity could be on the verge of improvement. We will be watching sector and industry group margins to see if the multi-decade downtrend is showing signs of reversal. Such a development, given the valuation overhang associated with policy risks like ‘Medicare for all’, could make the sector attractive. For now, we remain underweight.

We got the stock market call correct, but what about rates?

In a recent Bank for International Settlements (BIS) working paper titled “What anchors for the natural rate of interest?”⁴ the authors argue that monetary policy is contributing to low rates while the central bankers believe low rates are primarily attributable to savings and investment imbalances.

“The paper takes a critical look at the conceptual and empirical underpinnings of prevailing explanations for low real (inflation-adjusted) interest rates over long horizons and finds them incomplete. The role of monetary policy, and its interaction with the financial cycle in particular, deserve greater attention. By linking booms and busts, the financial cycle generates important path dependencies that give rise to intertemporal policy trade-offs. Policy today constrains policy tomorrow. Far from being neutral, the policy regime can exert a persistent influence on the economy’s evolution, including on the real interest rate. This raises serious conceptual and practical questions about the use of the natural interest rate as a monetary policy guidepost. In developing the analysis, the paper also provides a specific critique of the safe asset shortage hypothesis – a hypothesis that has gained considerable popularity in recent years.”

⁴https://www.bis.org/publ/work777.pdf

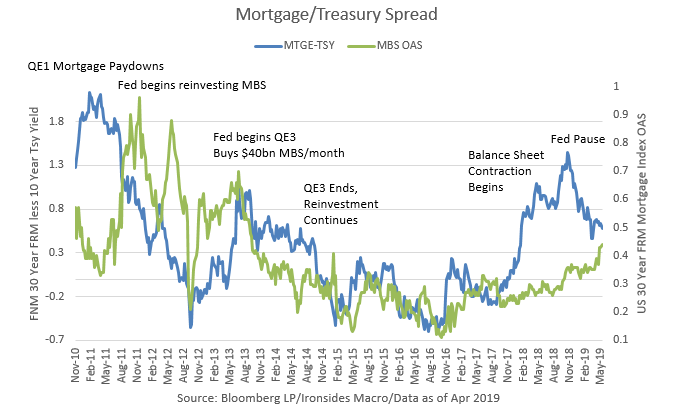

When we wrote ‘Fade the Fed’ following the March FOMC meeting we suggested buying bank stocks and that the yield curve would steepen led by long term real rates. Banks have done well due to another quarter of profitability well above the cost of capital, which we define as return on common equity well above 10%. The 5-year/30-year curve is little changed, however there has been a parallel shift in rates lower that literally interpreted, implies Fed policy easing later this year. Last week we went to a NY Economics Club lunch to listen to Boston Fed President Rosengren discuss policy. It was clear that the Phillips Curve operational framework is alive and well at the Fed as he discussed an unemployment well below the median and lowest FOMC participant estimate of the non-accelerating inflation rate of unemployment (NAIRU). He went on to discuss the range of estimates of the inflationary impact of tariffs, the transitory nature of the factors lowering core inflation, and stability of the Dallas trimmed mean near their 2% target. While his policy prescription implied no change to rate policy in 2019, he was biased towards hikes. On the same day, St. Louis Fed President Bullard took the opposite side of the debate and the market seemed to run with that. A day later, while the minutes of the last meeting offered no clues that rate policy was going to change in 2019, the staff’s presentation on the duration of the Fed’s Treasury portfolio offered two alternatives, both with shorter durations than their current holdings. So, while the next Fed move will be to end balance sheet contraction in September, they will continue to reduce mortgage holdings followed by shortening the duration of their Treasury portfolio. In other words, the Fed will be selling volatility and duration, which sounds like tightening to us. One final point, in a recent discussion with a client it was pointed out to us that there is massive demand for the 3-month to 18-month part of the curve. We noted that bank holdings of Treasuries have been surging since the Fed pause began and cash holdings are down 25% year-on-year, we suspect banks are getting positive carry on deposits investing in short-term Treasuries while continuing to meet post-crisis regulatory liquidity requirements. It might be that low 3 to 18 month rates might be less about expectations of Fed policy easing and more a function of market technical factors. There is a bear steepener coming, a temporary détente in the Trump Trade War is one potential catalyst.

https://ironsidesmacro.substack.com/p/fade-the-fed

We have been writing Ironsides Macroeconomics notes for three months; see the links to all of the weeklies below. We were consistently bullish equities until our April 27 note when we suggested a small correction in US equities and larger hit to the mercantilists – China, Japan, South Korea and Germany – due to a disappointing recovery in global trade. We still expect the US and China to reach an agreement, but do not believe the Trump administration’s aggressive trade policies will end there. Nor do we believe global trade will rebound sharply. We expect consumer spending to improve in 2Q and inventory destocking will boost manufacturing by Q3. Despite trade policy uncertainty, we expect higher stock prices and bond yields later this year. We continue to like banks, enterprise technology, and industrials. We would avoid bond surrogates, healthcare, and the export dependent equity markets. We are fine with high yield, the FOMC Chairman’s speech on corporate debt this week hit a couple of key points we agree with, first the banking system is not holding this risk, as was the case last cycle with the mortgage market. Second, the issuers are widely disbursed by sector. In a broad-based demand shock, leveraged loans, CLOs, BDCs, etc. will struggle, but, we think the probability of a large shock to consumption is low.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

May 18, 2019 https://ironsidesmacro.substack.com/p/how-you-doing-joe-6-pack

May 13, 2019 https://ironsidesmacro.substack.com/p/beggar-thy-neighbor-ii

May 6, 2019 https://ironsidesmacro.substack.com/p/worshipping-the-false-fed-idol

April 27, 2019 https://ironsidesmacro.substack.com/p/lets-make-a-trade-deal

April 20, 2019 https://ironsidesmacro.substack.com/p/housing-another-echo-of-88

April 13, 2019 https://ironsidesmacro.substack.com/p/earnings-season-3-themes-to-watch

April 6, 2019 https://ironsidesmacro.substack.com/p/china-malinvestment-central

March 30, 2019 https://ironsidesmacro.substack.com/p/the-transitory-growth-scare

March 23, 2019 https://ironsidesmacro.substack.com/p/fade-the-fed

March 16, 2019 https://ironsidesmacro.substack.com/p/its-a-profit-margin-game

March 9, 2019 https://ironsidesmacro.substack.com/p/central-banks-banks-and-currencies

March 2, 2019 https://ironsidesmacro.substack.com/p/echoes-of-87-and-now-88

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2019 Ironsides Macroeconomics LLC.