It's a Profit Margin Game

Disinflation is not a Monetary Phenomenon

Please enjoy our third weekly and kindly consider becoming a paid subscriber. For now the reports are available to the public, before long the full reports will available to paid subscribers.

This week’s US economic data and equity market strength were consistent with our ‘Echoes of ‘87 and Now ‘88 thesis¹ that equities will exceed the 2018 peak. The strength of software, IT services and semis shares this week, and year-to-date, are supportive of our view that investment in intellectual property products, partially attributable to corporate tax reform, remains strong.

¹https://ironsidesmacro.substack.com/p/echoes-of-87-and-now-88

In this week’s report we cover benign inflation, strong wage growth and the outlook for profit margins…

Consumer prices are not responding to diminished labor market slack and historically rarely have. The instability of this relationship calls the Fed mandate full employment and stable prices into question.

The wage Phillips Curve is alive and well, however, the 2018 acceleration in wage growth is better explained by greater labor market fluidity than lower underemployment.

Non-Monetary factors – excess global goods capacity and service sector technology adoption - are suppressing consumer prices as evidenced by low correlation of CPI categories.

Soft consumer price inflation and rising wage growth are raising concerns about margin pressures, stronger productivity growth is critical to extending the business cycle. We remain optimistic.

Sector Phillips curves and profitability metrics point to productivity gains in consumer and technology companies, and weak productivity in healthcare and housing.

The Price Stability Fed Mandate

We have long believed the Fed’s implementation of its mandate of price stability should be a low standard deviation of annualized changes in consumer prices, rather than a 2% target. Inflation volatility is low, near some of the best post-WWII levels and therefore we view the pause in the Fed tightening cycle as justified. Our first chart shows the both the standard deviation of CPI and the correlation of the expenditure categories of CPI. The correlation measure was constructed to determine whether endogenous economic factors like levels of unemployment and inflation expectations were impacting prices broadly or, alternatively, exogenous factors like global excess manufacturing capacity or technology adoption in select service sectors were influencing inflation. The data did not disappoint us, correlation was high in the ‘70s when inflation expectations rose sharply and poor public policy like wage and price controls failed badly. Currently correlation of the various CPI categories is non-existent. If disinflation was attributable to central bank credibility and low inflation expectations correlation could be high. We think the more probable explanation for low and stable inflation is global excess goods capacity and innovation in some, but not all, economic sectors.

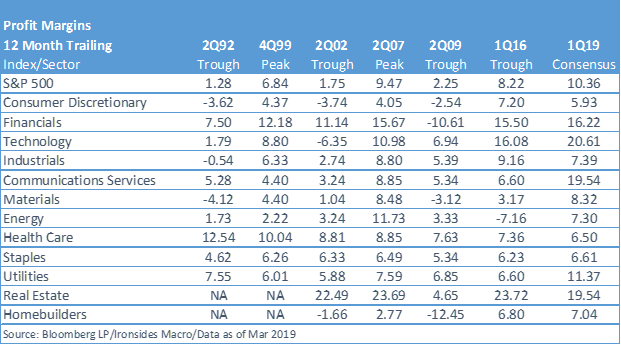

This week’s benign consumer, producer and core import prices reports juxtaposed with last week’s strong wage data, likely has some equity and credit investors concerned that rising wages and an inability to pass through the cost of goods sold will degrade profit margins. At a macroeconomic level, we believe the robust capital spending on productivity enhancing technology and improved labor market dynamism that is increasing labor productivity, will allow S&P 500 profit margins to hold at record levels if not even push higher. Still, there are a couple of critical economic sectors – healthcare and housing – where there is little evidence of productivity improvements. Those sectors have low profit margins and are a drag on US economic efficiency.

History is a Pack of Lies We Play on the Dead

The history of post-WWII inflation is an example of what Voltaire called ‘a pack of lies we play on the dead.’ The extreme inflation volatility in the immediate aftermath of WWII developed despite a return to fixed exchange rates and a gold standard. We believe the explicit cap on Treasury yields intended to monetize government debt until 1951, left consumer prices as the escape value for business cycle pressures. CPI peaked in 1947 at 19.7% before falling to -3% in the 1949 recession, little wonder capital spending to GDP ratio hit its post-WWII low. After the Fed won their battle with the Treasury in 1951 and slowly restored market forces to the setting of interest rates, inflation volatility dropped sharply setting the stage for the capital spending boom of the 1960’s.

The Great Inflation of the late ‘60s to early ‘80s is attributed to a weakening of central bank independence as LBJ and his ‘pre-modern monetary theorists’ pushed Fed Chairman William McChesney Martin – reportedly against the wall of a barn in Texas - to finance the ‘Great Society’ and Vietnam war simultaneously. This history provided the credibility for Keynesian economists to convince Congress in 1978 to officially expand the Fed’s mandate from lender of last resort. The new tri-mandate of full employment, stable prices and low interest rates, came under immediate stress due to stagflation. Two years earlier, Milton Friedman’s Nobel Prize acceptance speech “Inflation and Unemployment”² had raised serious doubts about the stability of the consumer prices Phillips Curve economic model.

²https://www.nobelprize.org/uploads/2018/06/friedman-lecture-1.pdf

We first studied economics as Fed Chairman Volcker waged his battle on inflation, his actions are credited with resetting inflation expectations and ending the Great Inflation. There were two other changes in economic policy implemented in the late ‘70s and early ‘80s that deserve some credit for changing inflation dynamics; Alfred Kahn’s deregulatory polices and supply side economics. One of the first policy changes the Reagan Administration implemented was deregulating the energy sector. These policies lead to a sharp recovery in US oil production and the ’85-’86 oil supply shock price collapse. Deregulation of airlines, trucking, telephone service and a host of industries contributed to the long period of disinflation.

Into the ‘90s the Fed continued to operate as if the relationship between consumer prices and unemployment was relatively stable. An excellent example is the exceptionally aggressive tightening cycle in 1993 when headline and core CPI were falling following the end of ‘jobless recovery’. The Fed’s aggressive actions nearly caused a recession. That episode may resonate with investors given the tightening of liquidity in 2018 when the ECB, BOJ and Fed’s balance sheets went from expanding by $2 trillion in 2017 to zero in 2018 and the Fed raised the policy rate at each quarterly meeting. Each of the these central banks has achieved relatively stable prices yet they all seem determined to reach a 2%, more or less, inflation target at any cost including – as discussed last week – the profitability of their banking system.

Consumer Prices are Not Responding to Slack, But Wages Appear to Be

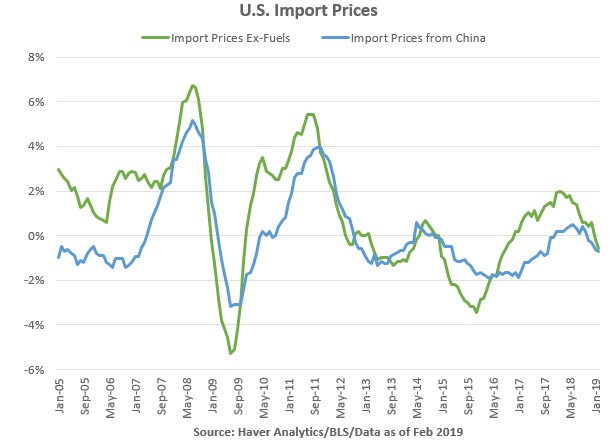

The next two charts illustrate our assertion that excess global manufacturing capacity is an external factor exerting pressure on goods prices. We dubbed the core goods prices relationship to unemployment, the Constanza Curve, because as unemployment goes down so do prices. New and used vehicles and apparel prices also have ‘Constanza’ or upward sloping unemployment curves.

This chart illustrates the external pressure on prices with China generally providing a deflationary impulse.

Here is a simple regression of our preferred measure for wage growth, the Atlanta Fed Wage Tracker and the U3 unemployment rate. The relationship remains strong and Friday’s release of the February Atlanta Fed Wage Tracker was close to the linear curve after a couple of months on the convex curve.

As we discussed in our February Employment Preview (https://ironsidesmacro.substack.com/p/february-employment-report-preview) the near term wage outlook is mixed. Last week’s February Average Hourly Earnings were stronger than expected at 3.4% from 3.2% in January, however our preferred measure, the Atlanta Fed Wage Tracker, fell to 3.4% in February from 3.7% in January. This week’s Job Openings (JOLTS) report pointed to a flattening out of wage growth in coming months. Although openings surged, the 2018 improvement in hiring and separations - reallocation - has pulled back in recent months. We strongly suspect trade and monetary policy concerns for the soft patch in labor market dynamism. If the business confidence is the culprit, hiring and quits should pick back up in coming months.

It’s a Profit Margin Game

Over the last year core producer prices have risen faster than consumer prices, wage growth has accelerated, yet, profit margins expanded. We strongly suspect that the faster productivity growth to 1.8% from the prior ten year trend of 1.1% played a significant role. This brings us to two interesting papers that offered insights on sector productivity. The first was presented at the Kansas City Fed Jackson Hole conference last August titled “Understanding Weak Capital Investment: The Role of Market Concentration and Intangibles”³, by Nicolas Crouzet and Janice Eberly. One of their interesting findings was that intangible investment is boosting productivity in the consumer and technology sectors, but in the case of the healthcare sector much less so. The second paper was from a Gallup economist in 2016 titled “No Recovery, An Analysis of Long-Term US Productivity Decline”⁴ that concluded there were three sectors responsible for slower productivity growth, healthcare, housing and education.

³https://www.kansascityfed.org/~/media/files/publicat/sympos/2018/eberly%20crouzet%20paper.pdf?la=en

⁴https://www.compete.org/storage/reports/gallup_norecovery_final_report_120516.pdf

Consistent with the sector research the S&P sector with the worst profit margin and return on equity trends is the healthcare sector and the one major CPI expenditure category that appears to be responding to slack, is shelter/housing. It seems likely that weak housing productivity growth and rising costs of construction, labor and mortgage money explain the 2H18 housing slowdown that played a significant role in the Fed tightening pause.

We have generally been positive on healthcare in recent years due to what we perceived to be a policy risk discount - Affordable Care, prescription drug price fixing - and a secular tailwind from demographics. We also expect productivity improvements, our labor market dynamism measure for healthcare has moved sharply higher over the last year hinting at labor productivity improvements. However, the aggregate profitability metrics for the sector, weak productivity growth and policy risks as the 2020 election process begins, warrant a sector underweight.

While we viewed the US economic activity as supportive of our positive economic and equity market outlooks, perhaps the best news this week was the stability in the inflation reports. Wage growth did accelerate and all things being equal could pressure profit margins, however, all things are not equal as productivity has improved with the exception of for healthcare and housing. We suggest being long enterprise tech and underweight healthcare.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

SEE IMPORTANT DISCLOSURES

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.