The Transitory Growth Scare

GDP Tracking Estimates, nothing in equals nonsense out

We have now completed our first month of notes, we are very pleased with the response. This weekend we will be rolling out an short audio summary of the note for paid subscribers. Next week we expect to have a term sheet for our institutional clients with multiple readers. Please consider becoming a paid subscriber, we expect to transition the notes to a free summary and full note for paid subscribers format in the relatively near future.

Here is commentary from Thursday’s Kansas City Fed March Manufacturing Survey.

The Federal Reserve Bank of Kansas City released the March Manufacturing Survey today. According to Chad Wilkerson, vice president and economist at the Federal Reserve Bank of Kansas City, the survey revealed that Tenth District manufacturing activity accelerated moderately, and expectations for future activity also increased.

"Factories in the region reported an uptick in growth in March, following three straight months in which the pace of growth slowed," said Wilkerson. "Plans for both hiring and capital spending picked up."

Our recent notes have made the case that the fixed income market is a less efficacious economic indicator than was the case prior to the ‘00s, however, for our sell bonds and buy bank stocks trade to be particularly effective, our view that the global growth scare will prove transitory needs to be correct. We acknowledge the weakness in China, Germany and global trade but are far less convinced there has been much more than a transitory confidence shock in the US. With that in mind, the focus of this week’s note is our outlook for economic output. It is time to make our case that the stock market, not the Treasury market is the better leading economic indicator.

We thought a good place to start in reviewing the economic outlook is to shine some light on the fascination with GDP tracking estimates. Perhaps the most widely followed is the Atlanta Fed’s GDPNow tracking estimate described on their website as follows: “GDPNow is not an official forecast of the Atlanta Fed. Rather, it is best viewed as a running estimate of real GDP growth based on available data for the current measured quarter.” We added the italics to make the point that the current 1.7% estimate is based on January data for retail sales, personal spending, trade, construction spending, durable goods, the PCE deflator and wholesale inventories. For import prices, employment and residential housing data we have seen January and February reports. Always missing from these estimates are capital spending on intellectual property products, while consumption of services are pretty questionable until the results of the quarterly services survey released after the first two Bureau of Economic Analysis GDP reports two months after the end of the quarter. We wouldn’t call it garbage in, just that there is little more than one month’s data in the model. Furthermore since the middle of March, the guesstimate has steadily increased from 0.5% to 1.7%. The trend is our friend.

Capital Investment: The Mix of Growth Matters

Let us begin by looking at our business cycle table. The first eleven rows show the average annualized growth rates for consumption, investment, productivity and price stability for post-WWII NBER business cycles, beginning after the introduction of the nation accounts data in 1947, measured peak to peak. The average row covers the entire sample, next is 2018 and the final two rows are the prior and latest 10 year periods. When President Trump signed the Tax Cuts & Jobs Act (TCJA) we wrote that we expected a small transitory boost to consumption, a much larger positive supply side shock to investment. Within the non-residential investment category, we expected stronger investment in intellectual property products (IPP) and structures over time, while any boost to equipment investment would be a second order effect of stronger business confidence rather than direct beneficiary of the tax bill.¹

¹https://www.cbo.gov/publication/52419

This week’s final 4Q18 GDP report told us 2.6% consumption was below the post-war average of 3.4%, and above this cycle’s average of 2.0%. Given the length of the expansion, improvement in labor market fluidity and associated acceleration in wage growth, continued household deleveraging, and structure of the changes in the individual tax code in TCJA, we would conclude the effects of tax policy were small. This is actually good news for the 2019 outlook, it implies there wasn’t much of a Keynesian stimulus boost. Keynes’ disciples seem to prefer government spending over tax cuts anyway.

Since very early this decade we have held the view that the necessary conditions for a capital spending boom like the ‘60s or ‘90s were in place. The sufficient conditions were improved tax policy and greater economic dynamism that was being restrained by public policy stabilization measures - monetary, regulatory and legislative - that had become counterproductive. To be sure, TCJA’s impact cannot be determined after one year; however, nonresidential fixed investment of 7.0% was double the prior ten year pace. Given that the reduction in the effective tax rate for equipment was marginal, but was significant for structures and IPP, we view the small uptick in equipment spending to 5.8% from the prior ten year average of 5.0% and increase in structures to 4.9% from -0.9% and IPP to 10.2% from 5.6% as strong evidence that TCJA worked as intended. One additional point, actual IPP has been well above our our capital spending plans model forecast. It seems probable that the lower effective tax rate explains the surge in software and R&D, the impact should persist in 2019.

The 4Q18 Confidence Shock

Fed Vice Chairman Clarida’s speech in Europe this week hinted that the board is gaining a greater appreciation for the ‘global dimensions of unconventional monetary policy’. Specifically he discussed global shocks and the growth in the sum of US external assets and liabilities from 25% of GDP in 1960 to 300+% today. We view this as consistent with our view that the risk off event in 4Q18 was largely a function of the drop in ECB, BOJ and Fed bond buying in 2017 of $2 trillion to zero in 2018 with the largest rate of change reduction in September. In essence, capital flows have a greater influence on markets and growth, therefore a Fed policy reaction function that minimizes financials conditions is flawed.

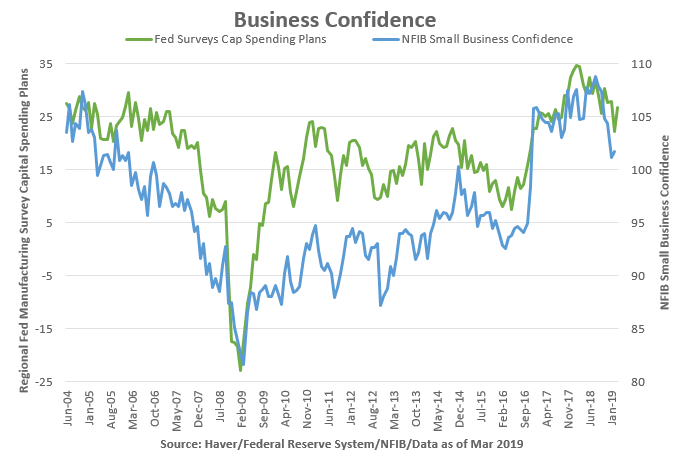

Like the Crash of ‘87, the 4Q18 risk-off event created a confidence shock that can be seen in the predicted value for core capital goods orders (green line) in our first chart derived from the forward outlook for capital spending from the regional Federal Reserve Bank manufacturing surveys. Our capital spending plan measure recovered in March after weakening for most of 2H18. The March NFIB Small Business Confidence Survey will be an important data point in determining if our view that the business confidence shock was transitory is correct. Both of these business confidence measures are at levels that compare favorably with the prior cycle, but need to recover in the coming months to be supportive of our bullish outlook.

Investment in Labor

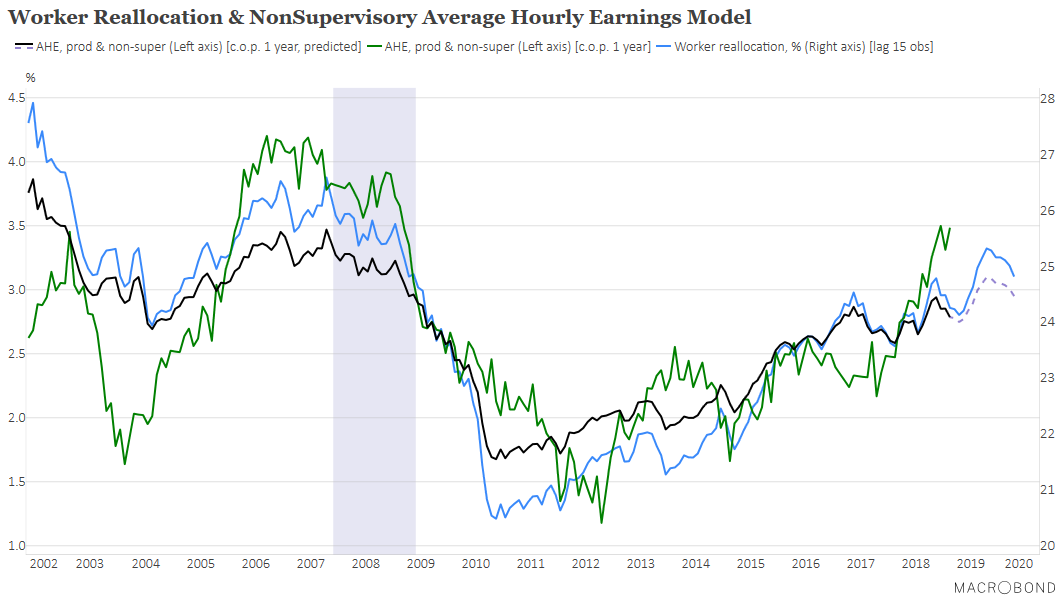

Improved labor market worker reallocation - the quarterly sum of hiring and separations expressed as a percent of private sector employment - slowed considerably in late 2017. In our view this was also related to the confidence shock, and it implies a flattening out of wage growth that lags reallocation by 2-3 quarters. As an aside, the surge in lower wage income growth is consistent with 2018 increase in fluidity. Two sectors; leisure & hospitality and retail comprise 40% of turnover but only 16% of wages. Increased dynamism and wages in these sectors also led the 2014/2015 wage growth after the end of extended unemployment benefits. Despite the recent setback, the outlook for labor market dynamism is favorable due to job openings and the hiring gap reaching new highs; still we will be watching the next few JOLTS reports closely to see if the openings get filled. One reminder, increased reallocation improves productivity. In our view, the late 2017/2018 increase in labor market dynamism was a key factor in the increase in labor productivity to 1.8% in 2018 from the prior ten year average of 1.25%.

The Other Guys - Residential Investment and Trade

There have been three major investment booms and busts in our career; the TMT boom began in the ‘80s, and peaked in the ‘90s. The housing boom originated in the ‘90s, and went parabolic in the ‘00s. Unconventional oil and gas exploration that broke the OPEC monopoly began in the ‘00s and peaked in the ‘10s. In each case when the bust came there was economic fallout that caused earnings recessions. The stock market recovery was generally ‘V’ shaped; however, the sector at the core of the investment cycle had a recovery that looked more like a square-root sign. Creative destruction took hold and the economy moved on to the next trend. Still, the industries that supported these booms including investment research, took longer to unwind leading to a tendency for market participants to focus on the last cycle. Specifically we recall pundits proclaiming the equity market ‘needed’ the tech sector to participate in the ‘00s to sustain a rally, the banks were a constant source of concern during the 2009-2016 pre-earnings recession cycle, and in the post the 2014-2016 oil collapse the energy sector and oil is an investor confidence drag. Additionally there is a tendency to look for another collapse in that sector that just went through a major bust.

We went on this slight diversion primarily to justify the lack of attention we pay to housing as a driver of economic activity. Further support for our boom/bust thesis is that this cycle is the only post-WWII expansion where residential investment failed to contributed 1-1.5% of GDP for at least year. The demographic dynamic of two exceptionally large cohorts at either end of the prime working age spectrum is likely depressing housing construction as well. Basically ‘Boomers’ are trying to sell expensive homes to ‘Millennials’ because there are not enough ‘Gen Xers’. One additional point we covered in our March 16th note², shelter is the only major CPI expenditure category responding to diminished labor market slack. In other words, this was by far the sector most vulnerable to the Fed’s Phillip Curve driven policy reaction function. Now that they have seemingly increased the weighting of financial conditions and inflation, housing investment should benefit from both lower financing rates and as GSE reform takes shape, potentially greater supply of credit. There is an ‘Echo of ‘87, and Now ‘88’ in housing; the 1986 Tax Reform Act significantly raised the after tax cost of mortgage finance, just as the increase in the standard deduction and capped of SALT deductions in TCJA did. The effect on housing proved transitory and 1988 was a recovery year. The risks for residential investment are favorable in 2019 at least and until bearish view on Treasuries unfolds.

²https://ironsidesmacro.substack.com/p/its-a-profit-margin-game

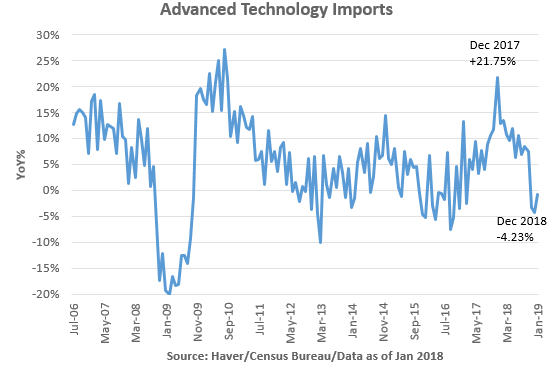

One interesting note on trade related to TCJA; the change from a worldwide to territorial tax system, and lower rate, reduced the incentive to book costs in the US and profits overseas. Transfer pricing of intangibles in the technology sector is fertile ground for this type of tax minimization strategies. Advanced technology imports spiked in late 2017 then fell sharply in 2018, however the aggregate impact on the trade deficit was swamped by strong relative growth in the US which boosted import growth. The risks are skewed towards a smaller negative contribution from net exports in 2019 as illustrated by the January report that boosted those infamous GDP tracking estimates.

The Coming Validation of the Equity Market Rally

As the fog caused by the shutdown of the government statistical agencies begins to lift and business confidence recovers from the ‘Echo of ‘87’ we expect stable consumer spending between 2.5-3%, strong business investment in IPP, a continued, albeit erratic, recovery in structures and stable equipment investment. Residential investment should improve, but, still not be a major driver to economic output, and trade should prove less of a drag in 2019. On that note we thought the surprisingly strong German February retail sales report underscores that although Germany is struggling with weaker global trade, they have the fiscal flexibility to spur domestic demand through lower tax rates. We expect a recovery in Asian export growth, though the secular trend is clearly towards producing where final demand resides.

So, after a month of Ironsides Macro notes we thought we would summarize our market views we have integrated into our work. We would strongly overweight equities over bonds. We clearly like financials, capital investment beneficiaries, technology and industrials, while we are negative healthcare due to margin pressures and weak productivity. While we haven’t written about the energy sector beyond our boom/bust cycles comment in this note, we expect a significant drop in energy price volatility over time given the increase in the elasticity of supply of oil associated with unconventional drilling. Diminished volatility in the final goods product should make equity part of the capital structure interesting over time, for now it is probably too soon after the bust for a sustainable overweight in the sector. Still, if we are correct the global growth scare passes, energy equities could continue their strong 1Q performance into 2Q. Bond surrogates, like bonds, should be sold.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2019 Ironsides Macroeconomics LLC.