Housing: Another Echo of '88

Tax reform related disruption should fade, but a recovery is a mixed blessing

This week’s note will focus on residential investment ahead of next week’s existing home and new home sales, advanced estimate of GDP and quarterly results from industry bellwether DR Horton. With the Mortgage Bankers Association New Purchase Index at a post-crisis high, the S&P Homebuilding Index up 26% in 2019, and strong orders guidance from Lennar and KB Homes in late March quarterly results, housing appears to be in the early stages of a recovery from the 2018 slump. We are broadly constructive and expect residential investment to provide some upside risk to GDP, however, the impact of a recovery in housing on inflation and monetary policy in 2H19 is a risk we doubt many market participants have considered.

The NY Federal Reserve Bank’s Liberty Street blog posted two interesting notes on housing this week. The first, titled “Is the Recent Tax Reform Playing a Role in the Decline of Home Sales” ¹, concluded that the limitation of state and local tax deductions (SALT) contributed to the decline in housing market activity. While this might seem intuitive, differentiating between tax reform and the impact of a 100bp increase in 30-year fixed rate mortgages is useful for our purposes. The second note, “Did Tax Reform Raise the Cost of Owning a Home” ² looked at effect of the increase in the standard deduction for lower income consumers and the SALT limitation and concluded that higher tax areas price appreciation was negatively impacted more so than low priced regions. In our ‘Echoes of ‘87’ thesis, a year long decline in housing from tax reform was an element in the macro instability that created the conditions for a market crash. The recovery in ‘88 was integral to why the ‘87 Crash did not mark the end of the business cycle. Interestingly the architects of the 1986 Tax Reform Act debated limiting the SALT deduction but ultimately did not. Nevertheless, it raised the after-tax cost of mortgage finance sharply due to the reduction in the top marginal tax rate from 50% to 28% when mortgage rates were ~10%. Given the progressivity of the tax code prior to the ‘86 Tax Reform Act we suspect the slowdown in activity was weighted towards the high end.

Let us compare the two periods. In 1987 housing starts fell from a 1.28 million seasonally adjusted annual rate (SAAR) in February 1987 to .92 million in January 1988 before rebounding back above 1.1 million in 2H88. In 2018, starts fell from 1.3 million to 1.1 million were they remained through 1Q19. Existing Home Sales fell sharply from a 3.9 million SAAR in December 1986 to 3.1 million in January 1988, conditions stabilized throughout 1988 to 3.7 million in December. The drop was a bit more than double the 10% 2018 decline. Home price appreciation (HPA) had been quite strong prior to the 1986 Tax Reform; the Case Shiller 20 City Index increased 9.4% in the year ending December 1986, HPA slowed to 7.5% in March 1988 where it remained until early 1989 when aggressive monetary policy tightening drove it to zero. The deceleration in 2018 HPA was similar to 1987, the CoreLogic Case-Shiller 20 City Index slowed from 6.25% to 4.14%. Like the 2018 slowdown, the Fed was tightening in ’87, the Crash led to some modest easing before the rate hike cycle resumed with a vengeance ending the cycle at a 9.75% funds rate from 6.75% when Alan Greenspan became Chairman in August 1987. Our primary conclusion from this episode as it pertains to the current period is that tax reform caused a one-year disruption in the housing cycle, however, with strong underlying consumer fundamentals – employment, wage growth, debt obligations – housing activity recovered strongly in ’88 as we expect in 2019. To be clear, we expect increased home sales and residential investment, but view a reacceleration in national home prices as unlikely though high priced areas should recover.

There have been several ‘it’s different this time’ explanations for the tepid recovery in housing since the largest housing crash since the Great Depression. The theories all have merit; student loan debt has reached a tipping point and the government takeover made debt restructuring far more difficult. The uneven demographic distribution – 76 million retiring boomers trying to sell homes to only 65 million Gen Xers while the 83 million millennials are likely scarred by their parent’s experience during the housing bust. Credit rationing due to the government takeover of supply and bank regulatory policy are all contributing factors in the only post-WWII cycle without a significant contribution to growth from residential investment. Even with a decent bounce in 2019, we think this business cycle will end without a typical cyclical contribution from residential investment. That said there is a decent case for residential investment to provide upside to GDP in 2019, however, based on Friday’s March housing starts report it appears that residential investment will not contribute to growth in 1Q19. Still, no contribution would be a sequential improvement from the negative contributions of -18bp in 4Q18 and -14bp in 3Q18.

Positive factors for a recovery in residential investment include:

· The 80bp drop in the Mortgage Bankers Association 30-Year Contract Rate Index from November 2018 to late March 2019 and monetary policy tightening pause at least through the September scheduled balance sheet contraction completion.

· The second-best year for household formation this cycle in 2018 at 1.5 million well above the 848,000 1Q19 average single family start rate. This is an erratic metric, however, the uptrend from the 2009 low is unmistakable.

· Our ‘Echo of ’87 and Now ’88 analog that implies the uncertainty shock from tax reform will fade. The recovery in the equity market strengthens our conviction in this analog.

· Improved labor market dynamism in late 2017 and most of 2018 boosted productivity and wage growth without an inflationary impulse. The health of the labor market has had the largest influence on housing in most academic studies.

· Only the second business cycle where the household sector did not add debt relative to GDP or disposable income and the lowest financial obligations ratios - interest payments relative to disposable income - since those series began in the early ‘80s.

· Loosening of the mortgage credit channel as new FHFA Director Calabria takes steps to encourage private sector lending. Residential mortgage loan growth in whole loans is improving even at the largest banks. Additionally, since the Fed pause securities holdings are improving, we suspect banks are buying collateralized mortgage obligations (CMOs) creating demand for non-bank originators.

Homebuilder equities look reasonable from a profitability and valuation perspective, so we would be long but would not expect to hold the position for the balance of 2019.

The Dark Side of Residential Investment

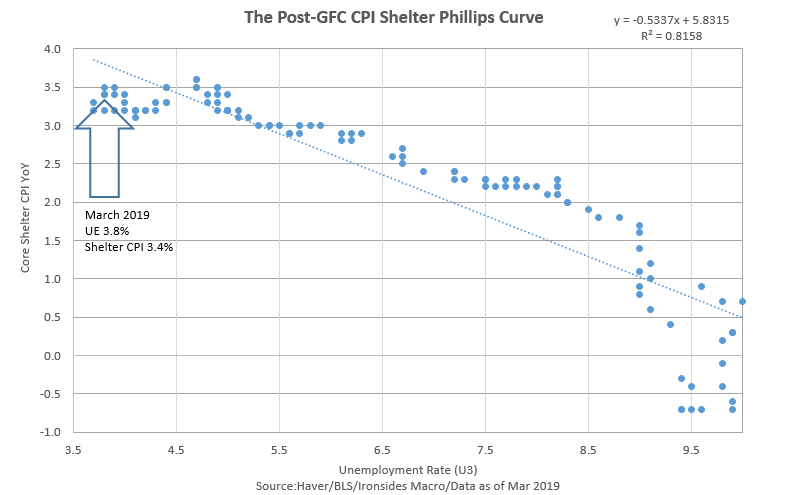

An increase in residential investment could cause a marginal deterioration in the mix of growth that was so favorable in 2018 – strong capital investment and stable consumption that boosted productivity without resulting inflation. A mini boom in housing would likely have negative implications for monetary policy though not until late in the year. First, CPI shelter is the only sector responding to diminished labor market slack implying upside risk to inflation if housing does strengthen notably.

Second, given the Fed’s goal of transitioning their balance sheet to all Treasuries, an increase in net supply of mortgages from increased purchase and refinance activity would accelerate this process. As the Fed’s control of the mortgage market falls, the duration and implied volatility of the private sector will increase. In other words, the interest rate risk of the private sector would increase at a time when Fed policy may be shifting back towards rate hikes. That dynamic in the late ‘80s contributed to the S&L Crisis and end of the business cycle. We think it is safe to assume that a shift in Fed policy is highly unlikely until the end of balance sheet contraction in September, nevertheless longer-term rates and implied volatility are likely to grind higher between now and then. We continue to like yield curve steepeners.

Observations from the holiday shortened week

In our March 30 note³, we argued that the global growth scare would prove transitory and the focus on GDP tracking estimates were misleading largely because there was quite a bit of missing data in those models. This week’s February Trade and March Retail Sales reports boosted the Atlanta Fed GDPNow model to 2.8%; it was 1.7% when we wrote that note and only 0.5% in mid-March. When strategists and economists look back on the 4Q18 equity market crash they are going to struggle to find any negative wealth effect. The growth scare was global and though Chinese industrial production, investment and exports strengthened, we were not particularly impressed due to weak ordinary imports and the production and investment gains being concentrated in heavy industry and real estate. The weakness in ordinary imports is evident in weak German Manufacturing PMI, in our view Germany needs to reduce individual income and/or consumption taxes and restructure from their export model. Perhaps the reduction of the economics ministry’s 2019 growth forecast to 0.5% will act as a political catalyst. We have not given up on a recovery in Asian trade activity. We are hearing constructive anecdotal commentary from contacts about Chinese reformers benefiting from the trade negotiations, we have long believed there would be a deal because it is in China’s interest. We do not expect them to give up on state control over the means of production and finance and erect a statue to Hayek; nevertheless, the heavy industry hard landing and now export sector slump, leave them little choice. In our view the Chinese only choose market-based solutions to economic problems when central planning fails.

³https://ironsidesmacro.substack.com/p/the-transitory-growth-scare

With 14% of the S&P 500 reporting, earnings surprise of 4.2%, by Bloomberg’s accounting, compares favorably with 4Q18 and 2017 reports, while sales growth relative to expectations at 0.3% is soft. Despite the slow start for revenue growth, we were impressed by organic sales growth from Honeywell (8.0%) Danaher (5.5%) and Dover (8.3%) on Thursday. The strong start to earnings surprises alongside better macroeconomic data should end the talk of an earnings recession. We have been asked when we think the equity market is likely to have a setback; our current thinking is that if a trade deal with China gets completed in another one or two months, global trade data has stabilized, and the S&P 500 is at a new cycle high, the market will be vulnerable to ‘sell the news’ sentiment-driven ~5% move lower.

In March 16 note⁴, we outlined our negative view on the healthcare sector based on weak productivity, a secular downtrend in margins and public policy uncertainty as the Democratic Party’s Presidential nomination process began. Despite our view, the negative reaction to a comment on Wednesday’s earnings conference call following what appeared to be strong results from healthcare provider UnitedHealth Group about the risk from ‘Medicare for All’ was shocking even for us. Fading public policy uncertainty, that is positioning for political outcomes far more benign than their rhetoric is one of our favorite themes. In our view it is too early to get long Healthcare, however, extreme reactions like last week should peak contrarian’s interest.

⁴https://ironsidesmacro.substack.com/p/its-a-profit-margin-game

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp