Let's Make a Trade Deal

Let's Make a Trade Deal

The earnings recession that wasn't & the next concern

We will be transitioning the notes to a free summary and full note for paid subscribers format on June 1st after a three month free trial for our initial list drawn from our readers at Guggenheim, Barclays and Lehman. We realize some of you signed on later, we hope another month is sufficient for you to assess the value of our product. Our client chart book will be available to our paid subscribers this weekend, it will be updated monthly. Additionally a short audio summary of our weekly gets sent to our paid clients. We expect to add additional products over time and as our long time readers know, we are always responsive to inquiries.

In this note, after reviewing earnings season and the most recent macroeconomic data we are going cover the next major issue after earnings season winds down we believe market participants will focus on, U.S./China trade negotiations and the disappointing recovery in global trade.

With just shy of 50% of the S&P 500 reporting, sales growth is tracking 3.7% and earnings are beating consensus by 5% taking the growth rate to 2% basically eliminating the risk of an earnings recession. The level of surprise compares favorably with 3.9% for 4Q18 and the 2017 average of 4.7% though well below first three quarters of 2018. The magnitude of the beat underscores the analyst reaction function/bias to stock prices and is a sentiment positive that contributed to a new closing high this week. Less favorable are revenues, which are only matching expectations and are tracking 3.7%, below the 5% level that we believe provides positive operating leverage. The sector mix is more favorable, despite some notable struggles with companies exposed to the auto supply chain – MMM and ITW for example – industrial revenues are tracking 4.7% and consumer discretionary sales are growing 6.8%. Financial sector revenues beat expectations of flat sales growth at 1% due to very tough comps, but return on assets and equity held at the 4Q18 levels which were the best in years. Most of the sales miss was in energy and materials. We also thought the difference between the large cap Russell 1000 earnings tracking 2.2% on 3.6% sales and small cap Russell 2000 earnings running at 6.2% on 3.9% revenues was notable. These results taken together with advanced estimate of 1Q19 GDP, are consistent with a couple of our core themes; productivity in the consumer and industrial sectors is improving and globalization is no longer expanding.

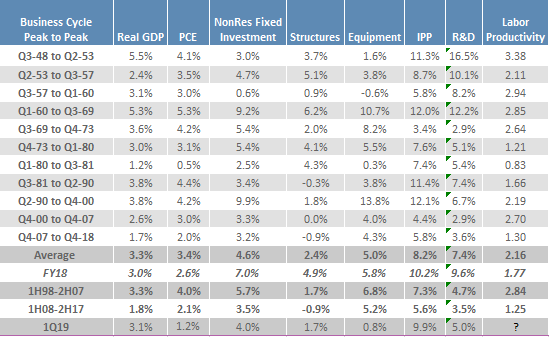

Before we move to global trade, we want to comment on the strong contribution from intellectual property products (IPP) investment in the advanced estimate of 1Q GDP. We got ourselves into a bit of a ‘proxy fight’ following the release by emailing the anchors of CNBC Squawk Box who subsequently asked their guest and my former colleague, Ethan Harris, about the strength of intellectual property products investment. Dr. Harris struck a cautionary note due changes in the Tax Cuts & Jobs Act (TCJA) that reduced the incentive to book intangible investment in low tax jurisdictions like Ireland. This is certainly true and partially explains why net exports positively contributed 1% to GDP this quarter, however, it is not the entire story given how much S&P 500 capital investment has strengthened since TCJA passed. S&P 500 capital investment at 11.9% year-on-year, up from 2.4% in December 2017, implies the government’s estimate of 8.6% growth in IPP in 1Q19 was not all about accounting, immediate expensing and a lower corporate tax rate boosted the underlying spend rate. Additionally the transfer of intangible investment to the U.S. from low tax regions does not imply current output is overestimated, rather output and productivity were underestimated prior to TCJA. The implications are profound; stronger growth pre-TCJA driven by IPP investment and productivity could explain why the unemployment rate is 3.8% and inflation is quiescent. One final note on 1Q19 GDP, the slowdown in consumption and inventory build was the same pattern as 4Q87, by early 1Q88 consumption rebounded and inventory liquidation had no discernible impact on growth. Based on recent spending data, 2019 is following a similar pattern.

Clashing Over Commerce

While some of our readers may be familiar with our views on trade and globalization, in the first two months of Ironsides Macroeconomics notes we have only tangentially covered the topic that was so pervasive in 2018. During our research we found a fascinating book; “Clashing Over Commerce, A History of US Trade Policy” by Douglas Irwin that made it quite clear that trade tensions are the rule not the exception. Long before we read Irwin’s book, in the early ‘10s we had become believers in the manufacturing renaissance thesis described by the Boston Consulting Group in a paper called “The Tipping Point”¹. Their argument was that unit labor cost convergence, increasing transportation and energy costs as well as increased supply chain and exchange rate risks had degraded the benefits of US corporate outsourcing to China of re-exporting for domestic consumption. Later we found “Demographics will reverse three multi-decade global trends”, by Charles Goodhart and Manoj Pradhan² and had the opportunity to meet Professor Goodhart. In short, their work detailed the impact of a 120% increase in the global supply of industrialized labor from 1990 to 2010 due to the integration of China and the Soviet Bloc into global goods supply chains. The massive increase in the global supply of labor created decades of wage disinflation in the developed world, and reduced wage inequality between the developed and developing world. Within the developed world and the more open economies in particular – the U.S. and U.K. – wage inequality was the price for cheap goods and reduced geopolitical risk. Unfortunately, as the Berlin Wall fell and a decade later when the WTO admitted China, a classic trade policy effect of diffuse benefits and acute costs left blew a large hole in the U.S. and U.K. manufacturing sectors.

²http://eprints.lse.ac.uk/84208/1/Goodhart_Demographics%20will%20reverse_2017.pdf

Politics Lag Economics

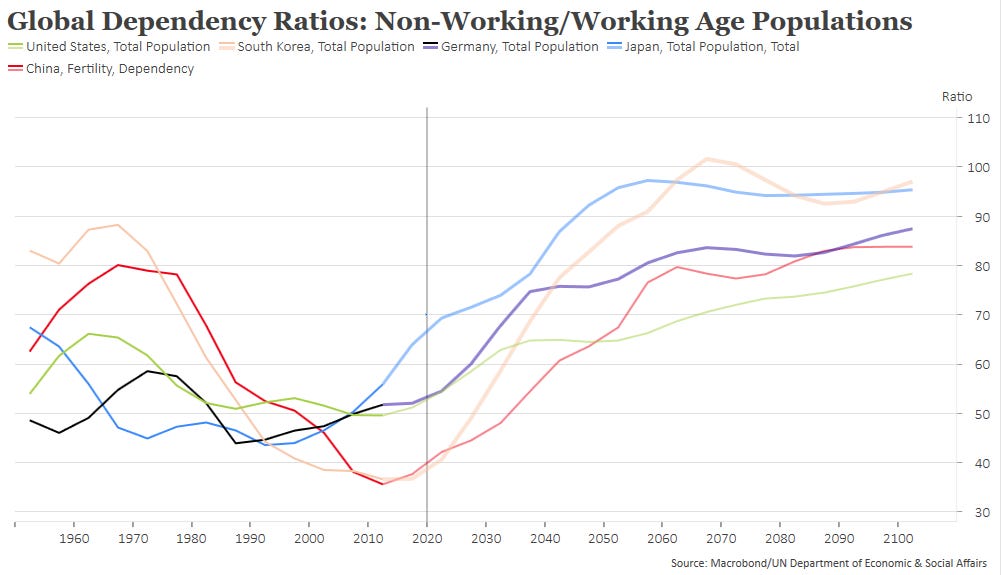

Last October we spoke at the University of Colorado’s Burridge Center Conference along with the Deputy Dean of the University of Chicago’s Finance Department about globalization and populism. While Professor Veronesi’s research³ linked populist politics to globalization, our analysis concluded that markets for labor, final and intermediate goods had largely diminished the benefits from developing world production. Our more controversial conclusion was that political markets would clear with a lag. In other words, populist anti-trade policies would lose momentum as it became clear that the world’s mercantilist systems – China, Japan, Germany and South Korea – were struggling with excess capacity and economic systems dependent on export driven growth. World dependency ratios – the percent of young and old divided by the working age population – bottomed in China, Germany, Japan and South Korea marking a turning point in the supply of labor and will rise more rapidly than the US for decades.

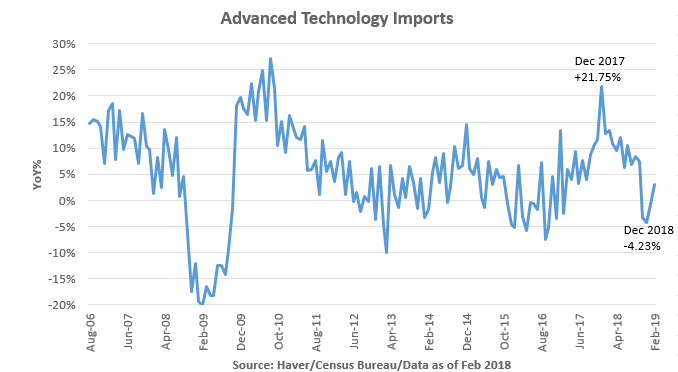

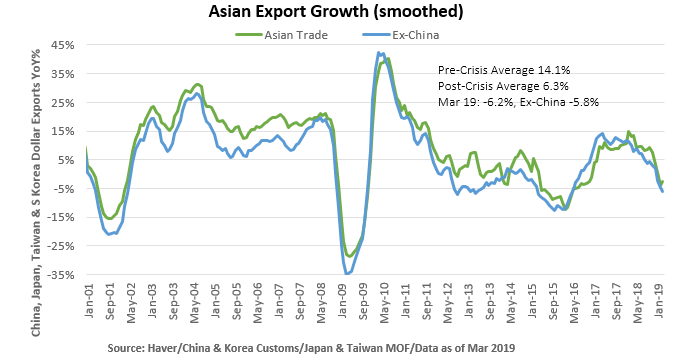

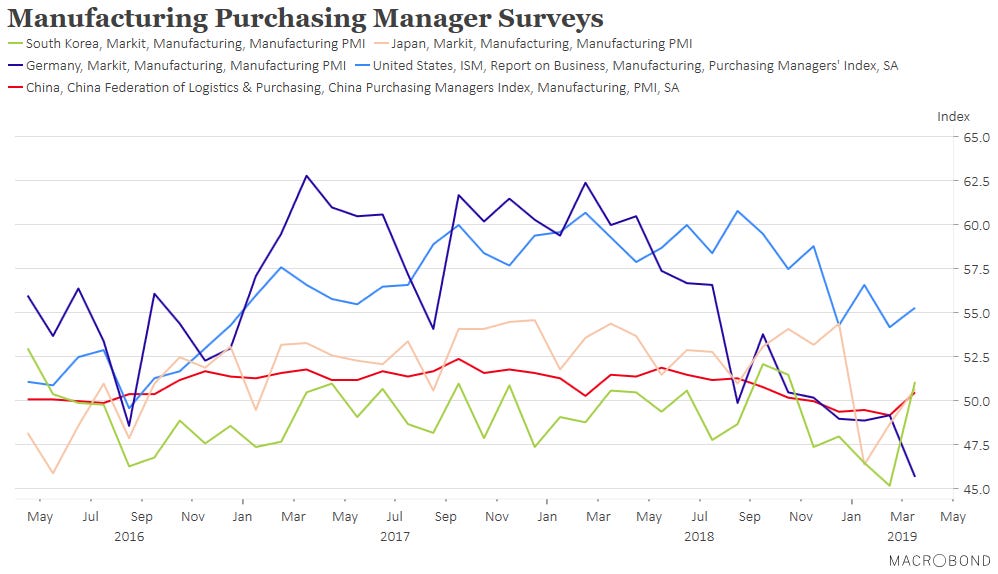

One approach to illustrating the deceleration in global trade is the growth of Chinese, Japanese, South Korean and Taiwanese exports in the ‘00s expansion of 14%, roughly double nominal world GDP (NGDP), slowing to 6% in the ‘10s close to the growth rate of NGDP. Since we gave our presentation in Boulder last October global trade data has dropped in a manner that implies globalization was not just no longer expanding, but actually reversing. While initially we viewed the plunge in global trade as exacerbated by stockpiling ahead of the US threat of tariffs on Chinese goods, the lack of a rebound after the end of the Chinese New Year implies the underlying trend might be even weaker than we thought. Recent weak data includes South Korea’s 1Q19 GDP 0.3% contraction due to a negative 2.6% contribution from exports, April 1-20 day South Korea exports -8.7% year-on-year, Taiwan’s March Export Orders -9.0%, German April Manufacturing PMI at a recessionary 44.5, and China’s March ordinary imports contracting 11.7%. Meanwhile back in the US, the advanced estimate 1Q19 GDP had a 3.7% increase in exports and 3.7% drop in imports for a net positive contribution to GDP 1%. While we view the expenditure method of the three approaches to estimating output as the least meaningful for investors, the positive contribution from weak global trade underscores the flaw in the logic of those expecting slowing global growth to lead to a US recession. We suspect when the Bureau of Economic Analysis releases gross domestic income and later still gross output, the impact of weak global trade evident in corporate sales growth slowing from 10% in 2Q18 to 4% in 1Q19. Still, most Asian Manufacturing PMIs turned up in April so we still expect a bounce in global trade. The strength of the bounce will be important following the signing of a trade deal.

Despite our view that transfer pricing of intellectual property products resulted in an artificially large trade deficit, we are not dismissive of the damage done by IP theft, forced technology transfers, beggar thy neighbor currency policy, state subsidies for heavy industry and exporters in violation of WTO rules. A wise person once said – we forgot which one - the Japanese invented non-tariff barriers and the Chinese perfected them. We are convinced the market has corrected many of these problems and China’s state directed capital allocation has led to two ‘malinvestment’ busts in five years; heavy industry state owned enterprises (SOEs) and now the export sector. We hear from contacts in China that reformers who recognize the strongest periods of Chinese growth occurred when the private sector flourished, are quite supportive of many of the US positions in the trade negotiations because it will reduce reliance on SOEs.

President XI’s speech at the One Belt, One Road conference Thursday implied the Central Committee is getting pulled towards reform, here is a sampling of Bloomberg headlines: “China won’t pursue yuan depreciation that harms others.” “China to further lower tariffs.” “China has great potential for consumption.” “China to improve law, rules of IPR protection.” “China to push forward supply side reform.” “China to further expand foreign investment market access”. “China to continue opening up.” Now we do not believe the Central Committee will give up control over the means of production unless they have no other choice, however, these headlines point to end of state support for heavy industry and exports, allowing foreign investment in services sectors and encouraging innovation. We find the headlines somewhat credible because we have concluded they have no other choice but to allow market forces as was the case in the late ‘90s when growth slowed and SOEs were dismantled.

While in many ways the current trade war is similar to the ’71 and ’85 battles with Japan and Germany that were resolved by currency agreements as described in Irwin’s excellent book, China’s problems are far more intractable than Japan or Germany. The size of the population relative to their natural resources implies that there is no way to maintain political stability without global trade. The last 6 months of economic data makes it clear that the US is far less dependent on global trade than China, Germany, Japan, Taiwan, and South Korea. You do not have to be a game theorist to understand a substantive deal between the US and China is likely, however, the secular trends are also clear. Perhaps the more interesting question is will Japan, South Korea and Germany restructure their economic models. The Japanese imposition of a VAT tax hike and Germany’s only fleeting discussion of tax cuts after the last election imply it might be more difficult in nations that have relied on the same export model since WWII to restructure their economic models.

As we observe the S&P 500 pushing to new highs as the earnings and GDP handily beat expectations with generally favorable drivers of growth; cyclical sectors for earnings and investment and net exports for GDP albeit with an inventory overhang, we are becoming concerned that our expected cyclical bounce in trade has not materialized in the macro data. Equity market price action is not completely convincing either, the Korean Kospi is one the weakest relative global equity index relative performers, the Japanese Nikkei is well behind the US, Chinese equities have stalled over the last month and Germany is lagging the rest of of Europe. When earnings season ends with the S&P most likely at new cycle highs, the focus will shift to trade. While we are optimistic the terms of the deal will have positive structural effects, it seems likely that the recovery in global trade could disappoint in the near term. Absent significant improvement in Chinese imports, Asian exports and later German manufacturing confidence, we expect a global market pullback sell the news of a deal outcome. In that scenario the US should outperform, we probably would not cut much US risk because of the momentum in capital investment and productivity that implies non-inflationary growth at least until later in the year. We would cut risk in Asian equities on a rally following the announcement of a US/China trade deal.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2019 Ironsides Macroeconomics LLC.