Fade the Fed

Rates, the Curve, the Dollar, Banks and their Forecasts

We hope you have been enjoying our notes. In coming weeks we will introduce products for paid subscribers and hope you will consider upgrading your subscription. In this week’s note…

Fed Policy is a lagging indicator

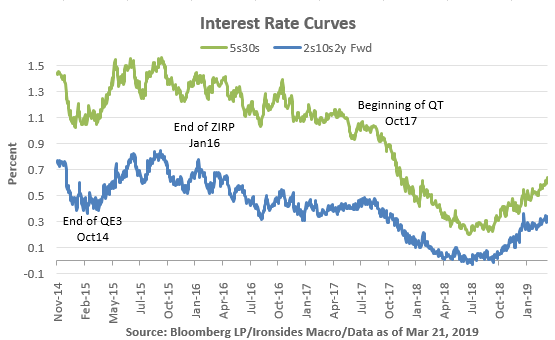

Conundrum 2.0: yield curve inversion is a false positive

The Fed wants to end credit easing: unwinding the mortgage book

The Fed reaction function: Keynes vs. Laffer

Our favorite ‘Fade the Fed’ equity trade: buy banks

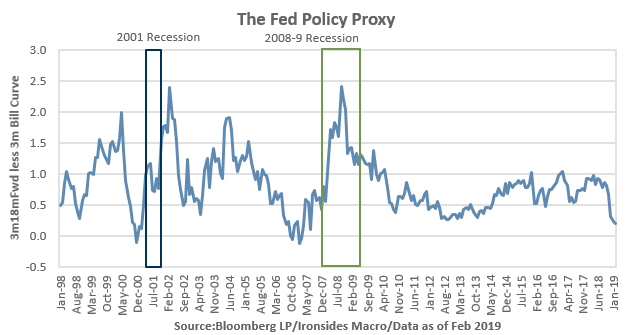

This week’s FOMC meeting was unequivocally dovish. Contained in the summary of economic projections (SEP) was a significant reduction in the forecast for the policy rate, and to a lesser extent; growth, employment and inflation that the Treasury market overreacted to. Despite Chairman Powell’s explanation that the SEP is not a committee decision, in other words there was no return of forward guidance or commitment to not hike the policy rate in 2019, our Fed policy proxy - the 3 month rate 18 months forward less the current 3 month rate - dropped 20bp by Friday morning and is now pricing a partial probability the next move is a cut. It struck us that ‘artificially intelligent’ investors created an opportunity for those of us willing to consider second order effects.

While the Treasury curve with the most academic research about recession forecasting, 3m10y, inverted, the very back-end of the rates curve steepened and interest implied volatility caught a bid on Friday. The ‘artificially intelligent’ algorithmic trading systems also sold the dollar, by the morning after the meeting the dollar was emulating the euro following the ECB’s surprisingly dovish meeting two weeks ago and rallying. The dollar bid despite a surprisingly dovish outcome is further evidence that the currency channel of monetary policy is weak. The negative equity market response to the December FOMC lasted three sessions, following the Fed was good for a quick 6% drop, fading the Fed meant capturing the subsequent 20% recovery. We view the sharp drop in Treasury yields similarly, investors overreacted to this week’s meeting; just as equities quickly reversed after the December hawkish FOMC meeting, Treasury yields are likely to bottom after this week’s events.

Fed Policy is a Lagging Indicator

We have long viewed Fed policy as a lagged dependent variable in the investment process. To be clear we are not being dismissive of Friedman & Schwartz’s criticisms of the Fed’s role in downturns in our all time favorite economic history book, “A Monetary History of the United States, 1857-1960. It should also be noted that we are on the email list for research from every branch in the Federal Reserve system. In other words, the Fed gets too much blame for downturns and credit for recoveries. Our career began shortly after the 1978 Humphrey Hawkins Law expanded the Fed’s mandate and the Volcker Fed was credited with crushing inflation. Since that time the Fed has evolved from being a referee in the background, to perhaps the central figure in investors’ investment outlook. We are not saying we view policy as inefficacious, rather the effects are less persistent, more subtle and investors would be better served by developing views about the economic outlook and assuming that Fed policy is more effect than cause.

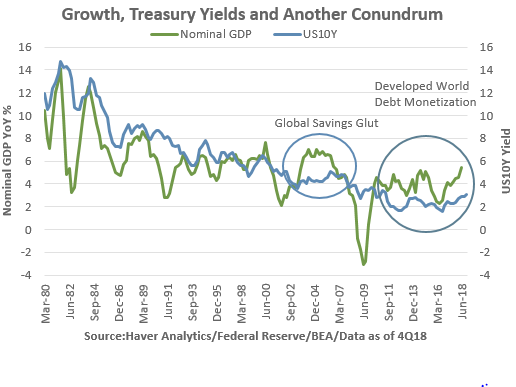

Conundrum 1.0 & 2.0

Right about the point when modern portfolio and risk management became widely accepted in the ‘90s and ‘00s and utilized by traditional fundamental equity investors, the global labor supply shock, modern mercantilism and related developing nations savings glut were driving driving Treasury yields persistently lower than nominal GDP for the first extended period since World War II. In other words at the point where the rest of Lehman Brothers trading floor added the government hoot - we always had it on the derivatives desk - the signals from the bond market were getting distorted by exogenous factors. Following the Global Financial Crisis, central bank large scale asset purchases played a major role in a second Conundrum. We are sympathetic to the demographic theories about low term premiums and real rates, however, in our view policy is a more significant factor than demographics in the post-crisis period. Nevertheless, trends in growth and rates are still positively correlated though not as strongly as was the case in the ‘40s - ‘90s. The information content in yield curve inversions in short-dated securities where central banks have direct influence, or longer maturities where the Fed, ECB and BOJ have large percentages of the outstanding stock, cannot possibly be as robust as was the case prior to the Global Financial Crisis.

Most academic work on longer term yield curves and recessions utilized the 3 month bill and 10 year rates; some recent work increased the robustness of the signal by adding the term premium¹. This approach implies the current flattening may prove to be a false negative similar to 1966, 1994 and 2005. A negative term premium implies that financial conditions are not tight and the credit cycle is far from complete.

¹https://www.chicagofed.org/~/media/publications/working.../wp2018-15-pdf.pdf

The Fed Wants Out of CE (Credit Easing)

Investor focus on rate policy and the Treasury portion of the balance sheet misses the bigger picture. The Committee voted to attempt to restructure the balance sheet from it’s current composition of $2.17 trillion of Treasuries and $1.61 of mortgages to ~$3.5 trillion of Treasuries. The next chart should give anyone thinking they will achieve this objective pause; the spread between the yield on a Fannie Mae 30 year fixed rate mortgage and 10 year Treasury blew out to 2% in 2011 when the Fed was not reinvesting mortgage paydowns, subsequent programs drove the spread negative and the option adjusted spread close to zero. While we completely agree with the policy objective, we suspect that the taper of the Treasury taper while mortgages prepayments are allowed to continue and then get reinvested in Treasuries, should push these spreads considerably wider. Higher fixed income implied volatility is likely to be a key factor in cheapening of mortgages relative to Treasuries.² Additionally Chairman Powell stated that the next major Committee decision is the duration of the Treasury portfolio, it seems likely their objective will be to shorten the duration to at least the same duration as the outstanding stock of Treasuries if not even shorter. Once again we are skeptical they will achieve their objective, but, between here and there the curve is likely to steepen as the Fed begins ‘Operation Reverse Twist’.

²https://ironsidesmacro.substack.com/p/fomc-preview-forget-the-dots

The Fed Reaction Function: Keynes vs. Laffer

The FOMC did not vote to pause rates for the entirety of 2019. We have written and spoken at length about the economic ideological struggle within the FOMC between Phillips Curve Keynesian disciples, and participants more sympathetic to supply side factors. President Trump’s announcement on Friday that he will nominate Stephen Moore is quite consistent with this struggle. In our view the surge in capital spending and rebound in productivity was a significant factor in 2018’s stronger growth and quiescent inflation. Chairman Powell addressed a question about corporate tax reform by describing the effects as clearly boosting demand and hopefully having longer term supply side effects. Given the Fed’s confidence in demand side effects and uncertainty with respect to the supply side, if global trade stabilizes as we expect in 2Q19 and US business confidence rebounds, we suspect there will be a solid constituency of FOMC participants who will move their ‘DOTS’ back into rate hike territory. There is little question that the distribution around the Fed reaction function is skewed towards easier policy, furthermore policy path changes can be thought of as turning a battleship. So, we are not suggesting rate hikes will be debated prior to the balance sheet contraction completion at the end of September, however, we still expect a hike in 4Q19.

The FOMC did vote to stop unwinding the balance sheet and to divest their holdings of mortgages. The vote to reduce their holdings of mortgages by $1.6 trillion implies completely transferring the mortgage prepayment option back to the private sector where it will need to be hedged by entities that have much tighter regulatory and leverage controls than the two largest pre-crisis holders - Fannie Mae and Freddie Mac - did. The Fed did the GSEs one better, they didn’t hedge at all. Of course if the rates markets becomes unhinged they can always stop the unwinding their mortgage holdings, but, the market will need to move significantly to make them change course. In the meantime if you are long the back-end of the rates market, particularly real rates (TIPS), you had better be quite convinced that the economy will weaken enough to overcome the central bank premium in government securities. We don’t believe the economy will weaken to the Fed’s forecast, we penciled in 2.5% growth in the CNBC Fed Survey this week. If we are even in the ballpark you have a couple of ways to win by positioning for higher rates in longer maturity fixed income.

Our Favorite Equity Market Fade the Fed Position - Long Bank Stocks

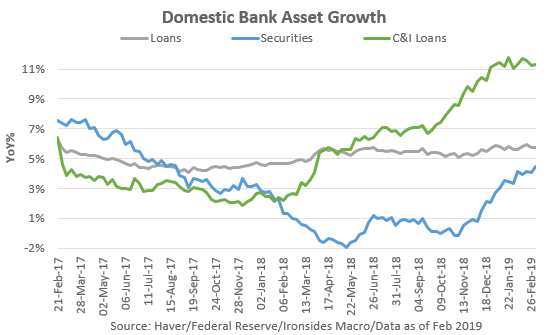

Bank stocks fell sharply in response to this week’s FOMC meeting just as European banks did following the ECB meeting two weeks ago. In our view the pullback is an overreaction and a buying opportunity for investors. There are two key factors in our positive view on financials; the first is a significant improvement in asset mix resulting from looser regulatory policy and unwinding unconventional monetary policy. The second factor is improving loan growth from the commercial & industrial (C&I) category and a 2019 recovery in residential lending after the temporary disruption from tax reform and monetary policy tightening. While the FOMC decided to stop the balance sheet contraction by the end of 3Q19, they also set the policy goal of reducing their mortgage holdings which should improve lending spreads for the banking system. Banks were never going to earn their cost of capital holding Treasuries, lending to the private sector has always been the key and the effective government takeover of the mortgage lending as been a consistent drag on bank profitability since the financial crisis.

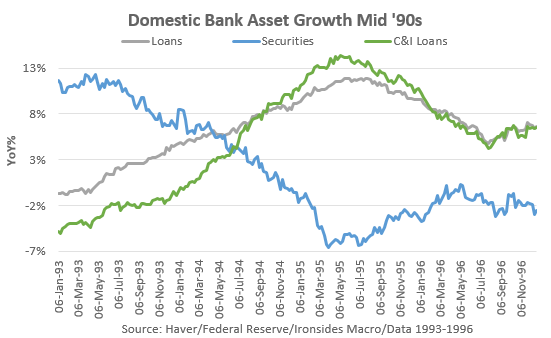

We have long believed that investors’ place too much emphasis on the yield curve and the impact on net interest margins. We frequently site the mid ‘90s to support our view. From February 1994 to February 1995 the FOMC increased the federal funds rate from 3% to 6% and the 2s10s Treasury curve flattened from 2.3% to 0.10%. Throughout most of the 1994 tightening cycle financials struggled, however, following the 0.75% hike in November they rallied 60% over the subsequent year trailing only technology stocks during the sharp 1995 equity market rally. In our view the catalyst was loan growth.

To be sure the fundamental picture isn’t quite as clean as was the case in the middle ‘90s, while we continue to be optimistic about the capital spending and resulting C&I loan growth, residential lending continues to be a drag on profitability particularly for the large banks - small bank residential loans are growing 6%. Still, as the Fed pushes forward with their intention to get out of the mortgage market, and following Mark Calabria’s confirmation as the new head of the FHFA, housing finance reform should finally begin moving forward which should further improve profitability on residential lending. We strongly recommend fading the Fed, the curve is likely to steepen, bank stocks will quickly recover and there is no recession within the investable time horizon.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2019 Ironsides Macroeconomics LLC.