The Bursting Bond Bubble

Correlation fever, the government bond bubble, shackling central banks, recession fake news, earnings risk fully discounted

The One Variable Market

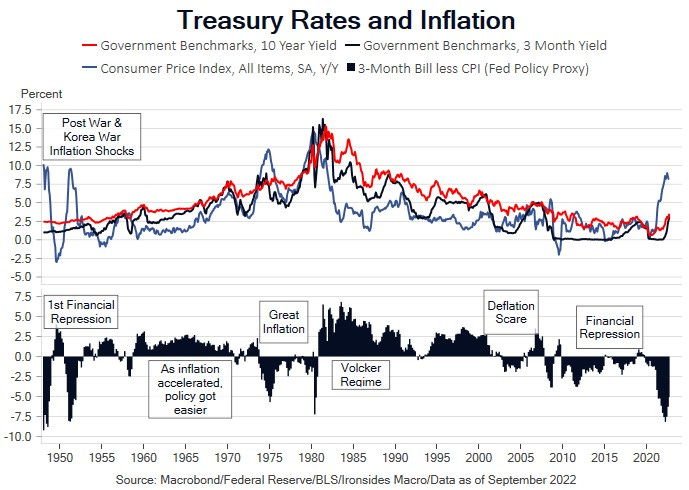

The correlation between stocks, bonds, commodities and the dollar relative to G10 currencies is approaching one (perfect correlation) due to the investment process being reduced to a single variable, Federal Reserve tightening. While stocks, bonds and the dollar are moving together, the fever is most acute in sovereign bond markets. Every economic, inflation or corporate earnings report is analyzed in terms of the implications for the Fed policy. Soft home sales, single family housing starts, and builder confidence lowered the correlation fever. Strong corporate earnings from consumer companies due to decent demand and pricing power raised the fever. Japanese September CPI caused a spike in the fever Thursday night with a sharp selloff in 30 and 40-year Japanese government bonds (JGBs), not subject to the Bank of Japan’s yield curve control, and the yen fell below 150 despite intervention threats spilling over to global yields. A Wall Street Journal story from Fed reporter Nick Timiraos that is consistent with our developing dovish dissenters view triggered a 130-point spike rally in S&P 500 futures Friday but left the back end of the Treasury market behind with a 26bp steepening of 2s30s (2s down 14bp and 30s +12bp). Later Friday morning, the Bank of Japan, on behalf of the Ministry of Finance (an important distinction) intervened for the second time since the September FOMC meeting and the yen rallied from 152 to 146. Global bond markets are chaotic, and the Fed appears to be on the verge of a blink.

Decades of buying of US Treasuries by central banks (CBs), beginning with Asian exporters suppressing currency appreciation in the ‘00s, and followed by developed world CBs after the global financial and European sovereign debt crises, facilitated massive growth in sovereign debt outstanding. Government debt liquidity collapsed due to the combination of the end of global QE, falling current account surpluses from the largest foreign holders of Treasuries due to the energy crisis and slowing goods exports, and regulatory policy that reduced the amount of capital available to trade government debt. The Federal Reserve and Bank of England, the two largest current account deficit countries that require capital inflows to finance government spending, are the largest contributors to global government bond chaos. Even as the correlation breaks with the coming Blink 2022, the shifting political winds are likely to restrict central banks degrees of freedom otherwise known as independence. We are headed towards an environment where markets determine the cost of investment capital, with reduced malinvestment, increased creative destruction, and faster productivity growth, but we need the central bank most responsible for the fever to recognize that with correlation going to one there is likely to be collateral damage.