Blink 2022

Markets reject forward guidance, house prices and rents fall, Fiscal Theory of Inflation, Deglobalization and Capitulation Update

Note: We will be back in New York City the week of October 10th, on the 11th and 12th we are attending the Robin Hood Investors Conference. We have been contributing to this high-quality charity for decades, the conference agenda looks excellent.

The Keynesians’ that spurred us on

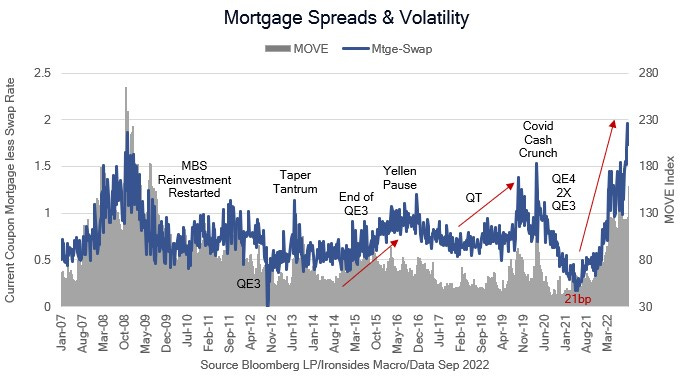

Global markets are rejecting the Fed’s reintroduction of forward guidance and attempt to reduce fiscally driven inflation with monetary policy. Attempts to deflect responsibility for the post-FOMC exponential tightening of financial conditions by blaming the new UK government’s tax cuts misses the real cause of exchange rate instability. The UK, Japan, China and Europe all have large energy trade deficits that are being made worse by exchange rate devaluation relative to the dollar. China and Northern Europe run large, but falling, trade surpluses that act as something of an offset in their balance of payments as the energy deficit surges. Japan’s trade surplus is largely gone, and the UK has a large trade deficit rendering them most vulnerable to the Fed’s faster pace of tightening (rates and QT). Since the FOMC meeting, all four of these currencies plunged, the Japanese intervention the morning after the FOMC meeting was their largest single day intervention at $20.9 billion, the PBoC has taken a series of steps as the offshore yuan fell to its lowest level since introduction below 7.25, the Sunday night pound flash crash to 1.04 and gilt pension fund LDI (liability driven investment) meltdown led to the BOE cancelling QT outright sales and restarting support purchases, and the euro fell well below parity. As Treasury Secretary John Connally famously said at a G-10 meeting in late 1971 after President Nixon ended gold convertibility, effectively ending the Bretton Woods exchange rate regime, ‘the dollar is our currency, but it is your problem.’ Were the only instability in exchange rates, the response of US policymakers that the strong dollar is helping reduce inflation might be excusable. However, mortgage basis spread widening, sharply higher fixed income implied volatility, tightening in swap spreads, a rapid increase in the Fed’s RRP balance and reduction in Treasury liquidity are compelling evidence that the Fed is moving too fast, is not regaining credibility, rather losing financial stability credibility. Instability in US fixed income markets are the consequence of a number of factors in addition to aggressive rate hikes that can all be traced back to the Federal Reserve, QT, GSIB increased stress capital buffers, and the supplementary leverage ratio. Our dollar, your problem, our mortgage and Treasury markets, our problem.

Our macro views remain intact, supply shock inflation has peaked making the path from 8 to 4 clear, and if there is a recession it’ll be a real, not nominal contraction that will have less impact on earnings than bank financed credit contractions (‘91, ‘01, ‘08-’09). Additionally, a recession is fairly discounted by the equity market given that the median decline associated with post-war recessions is 24%. Breakeven inflation got crushed this week, supply shock related inflation (goods, food and energy) has peaked and as we will discuss later, house price and apartment rent reports this week confirmed that housing inflation has as well. That said, the Fed’s reintroduction of forward guidance (4.5% or bust) risks a policy mistake as large as the Treasury and Fed’s massive 2021 liquidity injections and fiscal stimulus, when it was clear the recession was over. Monetary policy works through financial conditions, since the FOMC meeting, the tightening has accelerated to an exponential pace. It’ll be hard to put money to work in equities or bonds if and when they blink, we suggest adding exposure. We closed our Eurodollar December 22/23 steepener and IEF October 100/103 put spread, both trades worked well and while we do not believe the markets will allow the FOMC to realize the DOTS, if they insist on continuing down the current path, they will be cutting rates in 2023.

Brainard: Important to Consider Cross-Border Consequences of Tighter Policy

Brainard: Higher Risks Premiums Could Kick off Financial Deleveraging Dynamics

Brainard: Shallow Liquidity in Some Markets Could Amplify Further Adverse Shocks

Brainard: U.S. and Global Financial Conditions Have Tightened Rapidly

Vice Chair Brainard's speech was more of a wink than a blink