Appropriate Adjustment

Correction likely over, policy inflexibility, GDP gaps, S&P margins and capex

Appropriate Adjustment

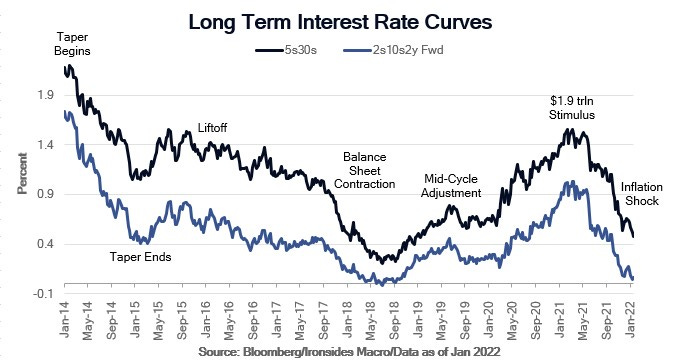

In last week’s note, Bills Only Policy, we detailed our framework for an appropriate adjustment to a significant inflection in Fed monetary policy normalization. There is a good deal of business cycle history enhanced by eight risk-off episodes during the Fed’s start/stop attempts to normalize policy following the largest financial crisis since 1931. That history implied an average 11% drop in the S&P 500, as of Monday mid-day the index was down 12%, Nasdaq -17%, and the Russell 2000 small cap index -21%. Bitcoin had rallied from $30,000, when the Fed expected below 2% inflation, to $65,000 when they acknowledged their forecast failure, then plunged back to $35,000 as the political winds shifted and Fed policy pivoted sharply. Turns out, bitcoin worked well as an inflation ‘hedge’, though based on what we heard last week we are less than convinced this Fed has the political will or technical skill to use their tools effectively to stabilize prices. In other words, our '60s analog, when the costs of being the world’s reserve currency became politically prohibitive, remains on track despite the Fed’s hawkish pivot. The bitcoin as digital gold due to monetary debasement thesis is not dead yet.

A week ago, Friday, we were not quite ready to declare the policy normalization correction complete due some missing characteristics of a full risk-off episode. By Monday morning, the term structure of the VIX curve (1-month less 6-month future) inverted sharply, the VIX spiked to 39% and our aggregate equity index volatility risk index was 3 standard deviations above its longer-run median. All the parameters of a Fed policy correction had been met. Some argued that Chairman Powell’s press conference was more hawkish than expected. We view his commentary, and the rates market reaction, as marginally unfavorable to risk assets, but not enough to justify a further decline in equities. More thoughtful responses to questions about the Fed’s balance sheet could have prevented curve flattening that exacerbated concerns that the Fed is tightening into slowing growth.