Bills Only Policy

Risk-Off, trading a bounce, Fed put strike, bills only policy, China eases

Risk-Off!

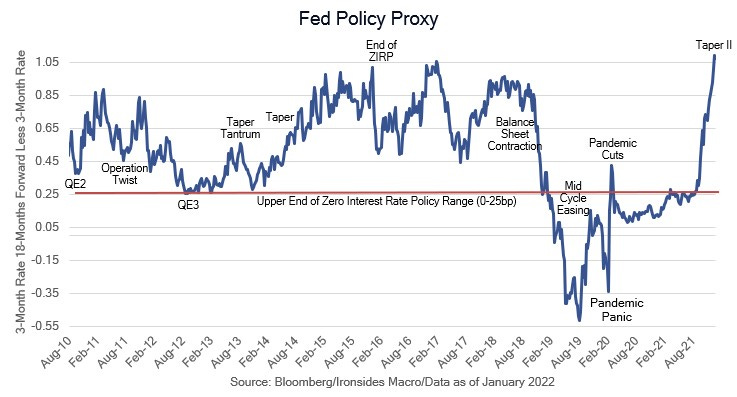

The equity market pullback broadened to most of the reflation cyclical sectors on Tuesday and Wednesday, while the sharp drop in concept stocks and negative cash flow technology drew in the higher quality free cash flow tech companies as well, as Nasdaq is down 13% and S&P 500 down 9% from the highs. There are some missing pieces of a typical risk-off episode, examples include energy stocks, commodities and the Chinese yuan that have been resilient. Recall our work on Fed hawkish pivot uncertainty shocks, where pre-QE correlation across equity market sectors and asset classes was much lower than the eight monetary policy related shocks last cycle. Additionally, the magnitude of the move is still less than the average of Fed policy normalization uncertainty shocks (10-12%), despite an expected policy path that is increasingly looking like the ‘94 cycle when the Fed increased the policy rate from 3% to 6% in a year despite the CPI remaining stable at 3%.

We are getting close to our S&P 500 down 10-12% ‘fat pitch’ target, along with elevated measures of risk including the VIX above 30, the VIX futures curve (6-month less 1-month) inverting by a couple of hundred basis points, and VVIX above 140, to deploy fresh capital or trade the market from the long side. In other words, down 10-12% is a necessary, but not sufficient condition for an attractive entry point. We will look for confirmation from our measures of risk to confirm that positioning is better balanced.