Unhealthy Broadening Out

Unhealthy Broadening Out

Correlation Spike Risk, Earnings Season Phases 2 & 3, Our Financial Conditions Framework, The Big Four Macro Reports & Monetary Policy, Retesting 5%

When Chaos Hits the Fan

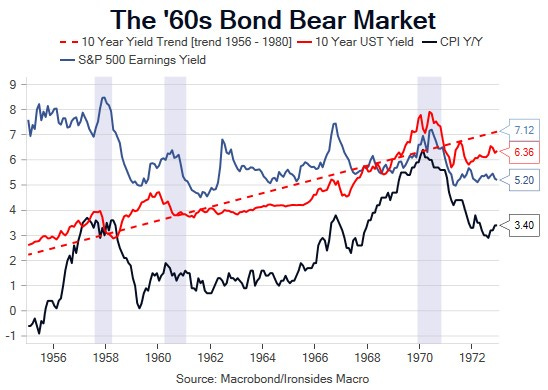

One of our key themes for 2024 is that until and unless the FOMC begins a reasonably aggressive rate cutting cycle to our estimate of the natural policy rate at 4%, a ‘healthy broadening out’ of the technology-, industrial- and energy-led equity market rally to small caps, financials and rate sensitive stocks, was improbable. Strong March economic activity and inflation data from the ‘big four’ reports (ISM manufacturing, payrolls, CPI and retail sales) rendered null and void the thesis that the hot January and February reports were a statistical aberration attributable to pandemic policies distorting seasonal adjustment factors. The combination of increased Treasury coupon supply, the pushing back of the timing of the start of policy rate normalization, the delay in expectations of reaching the natural rate that would disinvert the 3m10y banking business model proxy yield curve and increase in market expectations of the natural rate to close to our estimate from ~3%, kicked off yet another real rate driven bear steepening Treasury market correction. Since the Fed pause and pivot bias relief rally in Treasuries ran out of steam at the end of 2023, 10-year real rates (TIPS yields) increased 65bp to 2.24%, retracing 70% of the rally. Real rate shocks have plagued markets during the QE era; the end of QE1, QE2, QE3 also referred to as the Taper Tantrum, zero rate policy, the two QT shocks in 2018, 2022 and August-October of ‘23 are all examples of sharp moves higher in 10-year real rates leading to increases in equity market and cross-asset correlation, risk-off episodes.

The latest real rate shock last August-October unfolded in waves, and this one may have reached the eye of the storm as earnings take center stage from macro data and policy, for a week. As we detailed in our earnings preview in our April 6 note, Higher and Steeper, earnings season is likely to unfold in three waves. The first wave is bank earnings, profitability is under pressure as return on equity and assets, net interest margins and income are sharply lower than a year ago, and with no visibility to yield curve disinversion that outlook is negative. The second wave, industrial earnings, in the coming week, is likely be more favorable. The sector has performed well and is historically expensive, however expectations are low, both cyclical and secular trends are positive, and the early results (10% of the sector reporting) are impressive with earnings tracking 11.3% above a year ago. The market reaction has been positive — according to Bloomberg the average one-day reaction is +1.1%. The third wave is technology and related sectors, those reports will dominate investors’ attention this week. Unlike industrials, expectations are elevated implying a higher hurdle rate, however, like industrials, the cyclical and secular tailwinds are strong.

This brings us to the macro factors that are driving the increase in real rates. Next week’s only data with the potential to impact the policy outlook is Thursday’s advanced guesstimate of 1Q24 GDP and Friday’s March personal consumption deflator report. In both cases, many of the components has already been released, thereby reducing the probability of a surprise and with the FOMC thankfully in their pre-meeting quiet period, a reset of expectations is unlikely. The risk of a belly ache, as Treasury auctions $69 billion of 2s, $70 billion of 5s, and $44 billion of 7s, increases from $66 billion, $67 billion and $43 billion from the last month’s belly of the curve auction week, is elevated given the reset of monetary policy expectations. If the ‘chaos is going to hit the fan’ as one of our Lehman colleagues for whom English was a second language once said, it’ll be the subsequent week. The week kicks into gear on Tuesday with the most robust wage indicator, the 1Q24 employment cost index. Wednesday brings the April ADP employment report, March Job Openings and Labor Turnover Survey, April ISM Manufacturing, Treasury’s Quarterly Refunding Announcement and FOMC press conference. The week culminates with the April employment report. Treasury market ‘chaos could hit the fan’ in early May, leading to a highly correlated equity market and cross-asset risk-off unhealthy broadening out.

In this week’s note we dive into earnings season, detail our unstable equilibrium financial conditions framework, dig into the macro data and offer a preview of the critical employment cost index on the first day of the FOMC meeting and assess the risk of an unhealthy broadening out where an extensive of the increase in real rates leads to a highly correlated sector and cross-asset correction.