Macro Regime Change

Macro regime change, Super Core Momo, QT Clarity, Allocation Update

Macro Regime Change

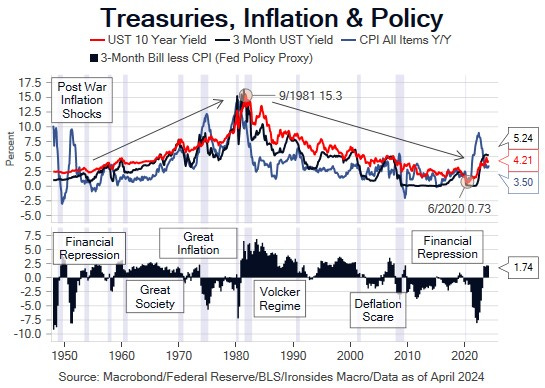

In the early stages of the pandemic, we concluded that policymakers and market participants utilizing the financial crisis as a model for the policy response were missing two major differences; the pandemic was an inflation and productivity shock, the antithesis of the financial crisis. The pandemic policy response accelerated several nascent related trends at different stages including inflation, a secular bond bear market, monetary and fiscal policy accommodation, supply chain derisking, a recovery in structures investment and accelerated technology innovation adoption. In essence, monetary and fiscal policymakers attempted to smooth the massive disruption to economic activity caused primarily by nonpharmaceutical interventions (lockdowns) through money creation funded by debt, while the dynamic private sector utilized technology to restore output. The fiscal transfers were particularly problematic, as detailed in A Fiscal Accounting of COVID Inflation and Three world wars: Fiscal–monetary consequences. Massive fiscal spending financed by debt, with no indication that the transfers would be reversed through reduced spending or higher taxes, created an increase in aggregate demand that could only have one outcome, a faster rate of inflation.

The implications of the fiscal theory of the price level came to a head Wednesday. CPI was hotter than expected. The 10-year Treasury auction 3bp tail highlighted our concerns that with a deeply inverted yield curve, the banking system was in no position to help the government finance the growing debt pile without a clear line of sight to a 4% monetary policy rate. Finally, Treasury released the March budget statement, revealing that for the first 6 months of the fiscal year the deficit was $1.06 trillion, essentially unchanged from $1.10 trillion for the first 6 months of the ‘23 fiscal year. Thursday morning’s PPI report offered a brief respite due to idiosyncratic factors like the treatment of auto insurance in PCED. The BEA uses the cooler PPI measure rather than the hot CPI index, implying a cooler PCED that may keep hopes alive for a summer initiation of a Fed policy rate cut. Longer maturity nominal and inflation-protected Treasuries correctly looked right through PPI and were immediately back under pressure as a price concession to absorb a 30-year auction.

When the 30-year auction on Thursday only tailed 1bp there was a relief rally in equities. Given that we just absorbed two major negative catalysts (payrolls and CPI) that led to a major re-pricing of the monetary policy path, and a 61.8% Fibonacci retracement of the Treasury issuance and Fed pause relief rally in 10-year Treasuries from 5% in late October to 3.80% by year-end, back to 4.58%, a consolidation of the losses in Treasuries is a reasonably probable outcome. We would avoid the temptation to add duration at these levels; the lack of visibility for the timing of either the first cut or a 4% policy rate that disinverts the 3m10y banking model proxy curve is likely to exacerbate the negative Treasury supply/demand technicals. Treasury will be increasing longer maturity issuance (fewer bills, more notes), Tax Day will drain liquidity from reserves and/or the RRP program, and the weakness in JPY, CNH and other Asian currencies is likely to further reduce demand for Treasuries particularly if the MOF or PBoC decides to intervene. One view we heard expressed by a rate strategist was the longer the policy rate remains at restrictive levels, the higher the probability of slower growth/higher unemployment, consequently, longer maturity Treasuries are attractive. The flaw in that thesis is accommodative fiscal policy that is boosting growth, and needs to be financed.

While we don’t expect more than a brief respite in USTs, equity market stability ahead of what is likely to be a decent earnings season (though not for regional banks) seems likely. Like the August through October real rate-driven bear steepening, the initial equity market reaction to an improving economic outlook is favorable due to the associated increase in earnings expectations, until and unless either the rate of change in real rates becomes disorderly or reaches a level that pressures valuation. From the early March low in 10-year TIPS at 1.79% following the February employment report, the rate increased 34bp. If we retest the late October 2.52% high, an outcome that seems more likely than not sometime in 2Q, we would be stunned if there is a not a cross-asset class risk-off episode that includes a 10% equity market correction. As much as we like the ‘95 analog for capital spending, productivity and the technology sector, we are in a reflationary secular bond bear market regime, the antithesis of the mid ‘90s and the two decades that followed.

In this week’s note we will review inflation week and the role of fiscal policy on the inflation outlook, discuss the FOMC minutes implications for the balance sheet, and provide our thoughts on asset and equity market sector allocation.