The Treasury Market is Over its Skis

The Treasury Market is Over its Skis

The Fed isn't, or at least shouldn't be, as close to a cut as the market thinks

We are making this morning’s flash update available to our free and paid subscribers, if you are not yet a paid subscriber please consider becoming one today. The button below allows you to subscribe using a credit card, for institutional group rates or to pay using research votes please contact us directly.

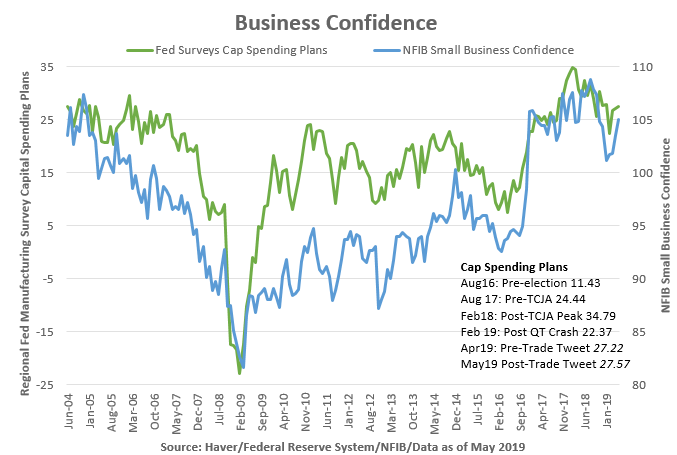

This morning’s NFIB Small Business Survey put an exclamation point on the recovery in business confidence in May as the end of the inventory destocking mitigates trade policy uncertainty. In other words domestic demand is more important than external demand.

https://ironsidesmacro.substack.com/p/flash-business-confidence-update

The release of China and Taiwan’s May trade data Sunday night showed some stabilization in Asian trade. To be sure global trade is decidedly weak and the effects of additional barriers to trade don’t bode well for a robust recovery. Still, it should be noted that Asian export growth remains stronger than during the 2014-2016 Chinese heavy industry hard landing related slump.

We are unconvinced by Friday’s May employment or last Wednesday’s ADP report that the labor market weakened significantly. We find the obsession with net payroll gains one of the greatest follies in finance; 75,000 net jobs divided by 151,095,000 total employed is 4.96 basis points. April’s Jobs Opening and Labor Turnover Survey (JOLTS) reported 5.562 million private sector hires, up from 5.345 in March, 5.234 million separations vs. 5.171 million, 3.3 million of the separations were voluntary (quits). The increase in hiring and quits marginally increased the quarterly turnover rate to 24.79% after a period of retracement following very strong increases in late 2017 and most of 2018. You read that correctly, nearly 25% of the labor market is reallocated every quarter, yet, the market obsesses over a 5bp net change in monthly payrolls. Our measure of labor market dynamism leads wage gains by 12 months and is productivity positive, as opposed to unemployment or other measures of slack, that degrade productivity.

We get how JOLTS is reported with a one month lag relative to the monthly employment report, however, the job leavers measure in the May employment report increased from 12.6% in April to 13.5% and the median duration of weeks to find a job dropped to 9.1 from 9.4 in April and 9.6 in March. The May Conference Board’s jobs plentiful and jobs hard to get survey questions improved to the best levels in two business cycles. Taken with the business confidence measures, it seems likely that turnover improved further in May and has regained positive momentum.

We think the narrative that growth has slowed is likely incorrect due to placing too much weight on the rates market relative to equities and international relative to domestic demand. It appears to us that business confidence improved sufficiently to reinvigorate investment in capital and labor. The completion of the inventory destocking process from the sharp drop in domestic demand in response to the 4Q18 QT Crash is more important to the US economy than soft global trade. Friday’s May retail sales report is the next important data point in determining if domestic demand has recovered sufficiently to work off excess inventories in turn restarting domestic industrial production.

Importantly, an increase in capital investment and labor turnover are both favorable factors for productivity, this implies non-inflationary growth. So, this mix of growth is not a reason for the Fed to tighten policy. The monetary policy mistakes last year were underestimating the productivity gains and the effects of quantitative tightening by the ECB and BOJ on their balance sheet contraction. Still, with equities close to their highs and the domestic economy in better shape than the bond market implies, rate cuts are far from a sure thing. No question the Fed changed their bias to ease, however, we are not confident they will do so and suggest front-end steepeners, and in equities, selling bond surrogates.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2019 Ironsides Macroeconomics LLC.