Flash Business Confidence Update

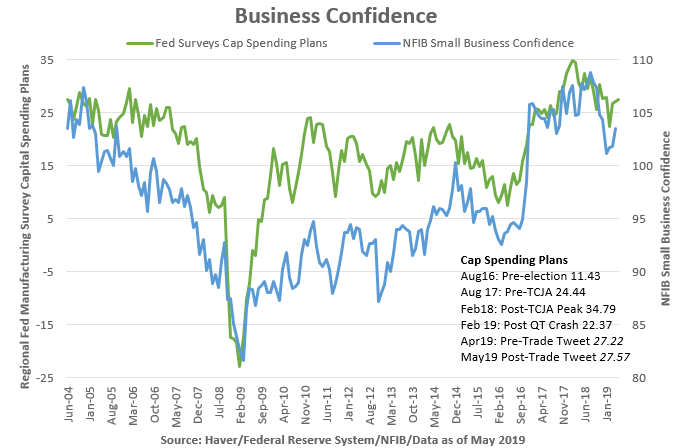

Despite the Tariff Tweet, Capital Spending Plans Held Up in May

Saturday’s note will be the first where the full note is available to paid subscribers only, the price is $89/month for individuals. Please subscribe online today or contact us for payment information to avoid missing future updates.

As we stare at a screen of red stock prices due to trade policy concerns we wanted to pass along a couple of positive observations. The Richmond Fed’s May Manufacturing Survey was the last input into our capital spending plans model and we were surprised that capital spending plans continued to recover from the 4Q18 QT stock market crash. While it is likely that capital spending plans will weaken in coming months due to the administration’s trade policy, given that the equity market has been declining for the entire month of May, the ‘tariff tweet’ was on May 5th and there was no pattern of deterioration as through time in the five regional Fed surveys released from May 15 through May 29, the marginal uptick implies the business sector might be more sanguine about trade than the markets.

A recovery in capital spending plans is crucial to our view that strong intellectual property products (IPP - software, R&D) investment will extend the recovery in productivity allowing margins to remain near all-time highs and the economy to expand without an inflationary impulse. Our capital spending plan index has decent forecasting value for investment in structures, capital equipment and IPP one quarter forward. Bottoms-up S&P 500 capital investment remains in double-digits, while the April core capital goods report was soft, we expect a recovery as the inventory destocking cycle decelerates. Business confidence remains vulnerable to the trade war, however, at least in May capital spending plans held up. The secular tailwinds driving capital for labor substitution in services are strong, the software investment boom is likely to continue.

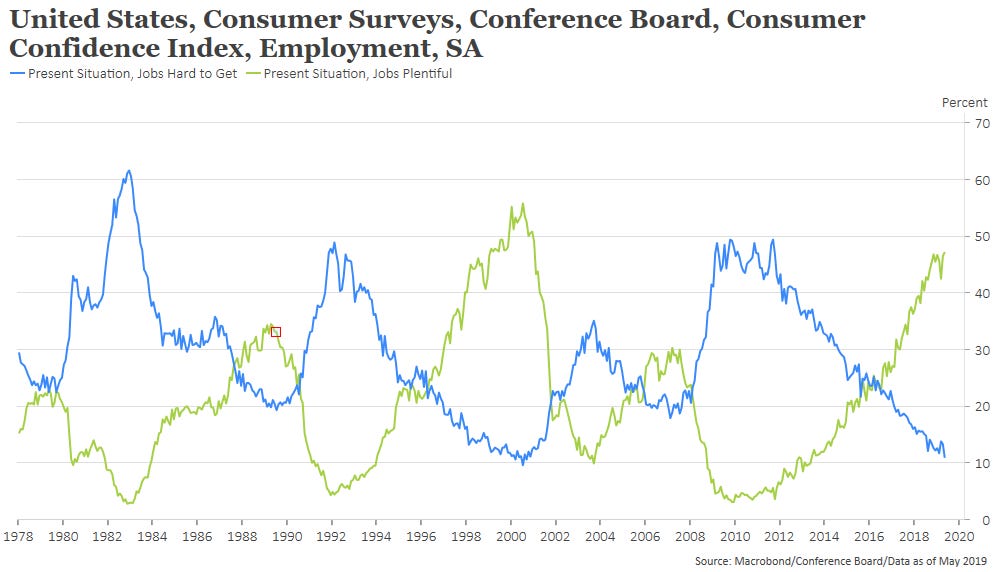

One quick note on yesterday’s the employment component of the May Conference Board Consumer Confidence report. The percent of survey respondents who described ‘jobs as hard to get’ fell to the cycle low and those who said ‘jobs are plentiful’ increased to a cycle high. Both levels were better than the peak of the labor market in the ‘00s expansion, close to the best ever levels at the end of the ‘90s business cycle. The improvement implies labor dynamism improved in May, this is another good sign for productivity and non-inflationary growth.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2019 Ironsides Macroeconomics LLC.