The Stock and Flow of M2

M2 stock, flow, velocity, bank reserves and asset mix, February data likely to soften.

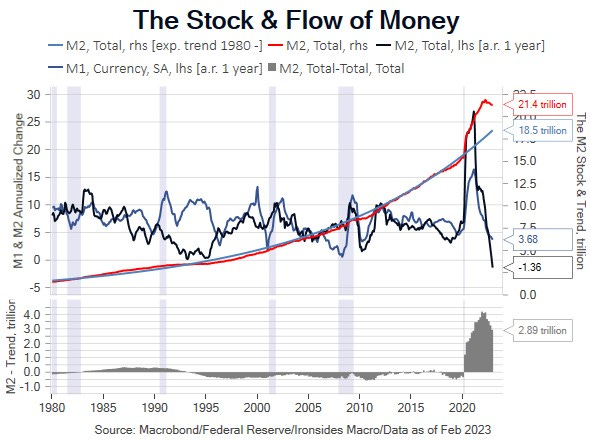

The Monetary Debate: The Stock or the Flow

Of the various bearish economic outlooks, one that resonates with us is annualized M2 growth contracting at the fastest rate in at least 70 years. After decades in derivatives our instincts are to focus on the rate of change; in the case of the money supply, we are referring to the flow of money, or more generally, system liquidity. This concept was integral to our bearish 2022 outlook, where we expected both the Treasury and Federal Reserve to drain liquidity by increasing Treasury issuance and ending QE and beginning QT. The Treasury drained $900 billion in the first four months of 2022 and then The Fed began QT in June, this liquidity reversal was a primary driver of last year’s negative fixed income and equity returns. While we believe that easy monetary policy primarily creates asset inflation, we are not arguing there is no real economic impact of tighter monetary policy. The most direct monetary policy channel to real economic output is of course housing, and there were no long and variable lags in 2022, with the exception of the BLS and BEA’s goofy shelter inflation indices, housing demand dropped 37% (existing home sales) and demand 31% (single family starts). In other words, the impact of the Fed’s tightening process that caused mortgage rates to spike more than 4%, on both housing supply and demand, were immediate. Global manufacturing and trade also contracted in 2022, though monetary policy did not appear to play a role, instead it was the most extreme inventory restocking/destocking cycle since the late 1940’s.

The question at hand is whether the stock of money, measured here as total M2 relative to an exponential regression trend beginning during the Volcker Fed in 1980, remains excessive and subsequently is an offset to the sharp decline in the growth rate. This question is crucial for the near-term outlook for monetary policy and Treasuries, as we detailed last week in Iceberg Risk, January labor market and consumption reports were the primary catalyst for the sharp flattening in the cleanest yield curve recession indicator, the near-term forward spread, that flattened further this week to -12bp, 101bp from its low in January, and increase in 10-year Treasury yields from the mid-January low of 3.32% to nearly 4% this week. While our forecast is for the economy to skirt a recession in 2023, expecting the labor market and consumer spending to be unaffected by the extreme reversal in the flow of money is an ‘it’s different this time’ thesis that troubles us. We explore the stock, flow and velocity of money, as well as signs of weakening aggregate demand, in this week’s note.