The Good Place

Increasingly Narrow Equity Rally, Transitory Disinflation, The Fed's Good Place

Ironsides Macro on Forward Guidance

An interview on the macro-outlook with some broader thoughts on the current monetary and regulatory regimes origins in the financial crisis.

Unhealthy Broadening Out

Our rule of thumb is three months of relative equity sector performance is a reasonably efficacious economic indicator; on that basis, the year-to-date weak relative performance of consumer discretionary, small caps, regional banks and rate sensitive sectors has spread to larger cap financials, industrials, energy and materials. In essence the strong performance of the technology and communication services sectors is obfuscating an unhealthy broadening out that appears to be signaling a slowing of aggregate economic output. The pattern of underperformance of all but the two sectors benefitting from the Gen AI investment boom was particularly evident this week, but is also the case over the last one and three months. Good old Dow Theory is consistent with these trends, with transports down 6% over the last month and 3% this week. The now 3-month long unhealthy broadening out, likely due to weaker economic demand, accelerated this week in the equity market as evidenced by tech outperforming industrials by 8% as of Friday morning, was also consistent with strong 10 and 30-year Treasury auctions before and after Wednesday’s cool CPI report and hawkish FOMC Summary of Economic Projections (SEP) ‘24 policy rate forecasts.

This week’s Treasury market rally, despite an FOMC not prepared to act preemptively, appeared to render a verdict on the Tale of Two Surveys discussed in last week’s review of the May employment report in favor of the higher unemployment rate due to a drop in employment in the household survey. There were a couple of additional factors that supported the rally in USTs, including Macron’s gambit and the widening of French sovereign debt relative to Germany and of course, better than expected inflation data this week. Were the equity market unhealthy broadening out not persistent and picking up steam we suspect the strong payroll headline increase and delay in the SEP forecast for beginning the path to 4% would have offset the cool inflation reports and French sovereign debt widening.

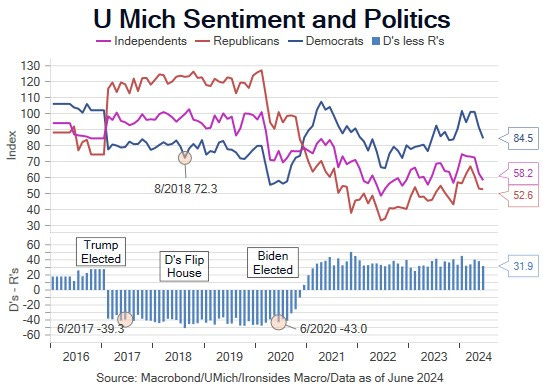

The Fed’s data dependent driven policy process means trends that become clear to market participants, such as a cross-asset reduction in the market implied growth outlook, will not trigger a start to rate normalization until there is a preponderance of evidence that demand for labor has fallen below the growth in supply. Chair Powell suggested he is sympathetic to the thesis that the establishment survey (Current Employment Statistics) is overstating labor market demand, nevertheless he characterized the labor market as strong. During next week’s Fed speak flood we will be listening for additional clarity on the Committee’s consensus view of the balance of labor market risk. For anyone who questioned our view that a growth scare that triggers an equity market correction will precede Fed rate cuts, in other words the equity market will not look through weak data in a ‘bad (data) is good (for markets)’ outcome, needs to check their bias after the FOMC looked right through Wednesday morning’s much cooler than expected CPI report.

In this week’s note we review inflation week, explaining the following views. First, that falling inflation volatility (price stability) is favorable for equities. Second, fiscal policy and the ‘complicated’ housing market pointing to hotter trend inflation despite the Chinese deflationary goods impulse are unfavorable for Treasuries. We also dig into the FOMC’s reaction function: in short, the labor market is the most likely catalyst to begin the path to 4%, the level that we expect to disinvert the curve and reopen the bank credit channel. We end, as usual with our updated thoughts on sector and portfolio allocation.