Healthy Broadening of Disinflation

Price Stability, Broader Disinflation, July Should be on the Table, QRA, Financialization and the Small Cap Bounce

Note: The next two weeklies will be released on Monday morning rather than our standard Saturday delivery. We have back-to-back golf member guest tournaments.

The Cost of Price Stability

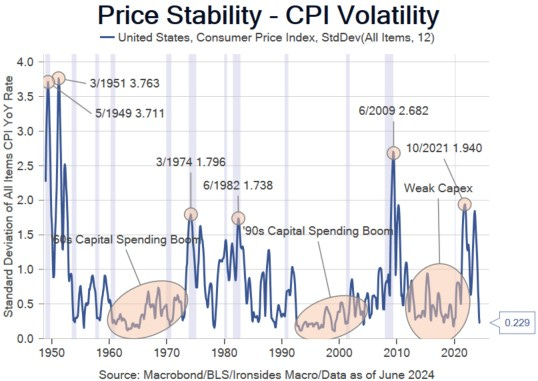

While all items CPI cooled from 9% in June ‘22 to 3% in June ‘23, firmed modestly to 3.7% in 3Q23, before returning to 3% in June ‘24, our measure of price stability, the standard deviation of annualized all items CPI, has been steadily declining to the 4Q19 average of 20bp. Inflation volatility persisting below 50bp annualized is relatively rare; it occurred in the early ‘60s and in the late ‘90s, and both periods were very favorable investment environments in terms of real capital investment and equity market valuation, earnings and returns. The FOMC’s mandate is not 2%, it is price stability. With the Supreme Court striking down the Chevron Deference Doctrine, perhaps the FOMC should be pressed on the 2% target and their holdings of longer maturity securities. The markets have been discounting price stability since October ‘23 as evidenced by the decline in the MOVE Index (Treasury implied volatility) and the VIX (S&P 500 implied volatility). Now that 2Q24 inflation has cooled sufficiently to give the FOMC confidence that they can begin the process of disinverting the banking business model proxy 3-month 10-year Treasury curve, this begs the question: will the damage attributable to their suboptimal tightening process that caused the deepest curve inversion since Volcker become increasingly evident? With next week’s start to 2Q24 earnings dominated by banks, we should get a sense of whether the market can look through what is likely to be weak profitability.

On our way to a September rate cut there is likely to be a series of soft economic reports, beginning with next Tuesday’s June Retail Sales report. During a CNBC appearance, Bank of America reported their retail sales measure fell 0.5% in June, the first decline in 4 months. Amidst steadily weakening consumption data through 2Q, the Atlanta Fed PCE tracking estimate has cooled from an initial estimate of 4% quarterly annualized to 1.5%. As we discussed in Slowdown last week, the labor market is flashing an important warning sign and total hours worked barely increased in 2Q. In Earnings Crunch Time three weeks ago, we detailed expectations for a broadening of the earnings recovery from the 4Q22 through 2Q23 earnings recession to the nine ex-technology and communication services (Gen AI) sectors. We saw numerous reports characterizing the economy as strong due to record levels of air travel, only to learn on Thursday that the CPI airfares index fell 5.0% in June after a 3.6% monthly decline in May. Unsurprisingly, Delta guided lower due to a drop in revenues per seat mile. Price is the ultimate measure, if it is falling, unit sales are of little consequence.

Notably another factor in the CPI downside surprise was a 2% monthly drop in lodging away from home, adding more evidence to the slowdown thesis. Airline stock prices have been signaling weaker profitability for months; the airline industry may be a microcosm of our concerns about the persistent weak relative stock price performance (3-months is our benchmark) of economically sensitive sectors like transports, small and mid-caps, industrials, materials, energy and homebuilders. The timing of the first cut matters, but the time it takes to get to 4%, the level we believe would painlessly disinvert the 3m10y curve, matters more. We suspect the FOMC will take their time getting to 4% unless the labor market data deterioration accelerates. If it does, concern the Fed is behind the curve/pushing on a string/made a policy mistake, will likely drag equities lower.

In this week’s note we will review the CPI report utilizing Chair Powell’s core goods, rent of shelter and non-housing services inflation framework, offer some initial thoughts on earnings and expand on a Fox Business live studio audience appearance where we asserted a series of policy tradeoffs had serious unintended consequences. As usual we will conclude with our portfolio allocation thoughts, but spoiler alert we do not expect the ferocious Russell 2000 short covering rally and long technology liquidation on Thursday following the CPI report to persist.