Slowdown

Slowdown, Time to Cut, Trumpflation, Sector Change Ahead of Earnings

Note: We will be in NYC Wednesday and Thursday

Slowdown

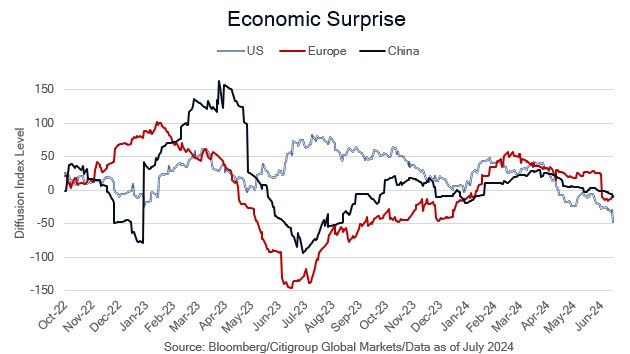

The Atlanta Fed GDP tracking model for 2Q24 peaked over 4% in early May following the release of April employment, retail sales and the ISM Manufacturing and Services surveys, but has fallen through June and early July to 1.5% after weak June ISM surveys. As we will discuss in this week’s note, the June employment report was unequivocally soft with a range of leading components, including a key recession indicator, making a September rate cut probable. In short, the economy came into 2Q like a lion and is going out like a lamb. The internals of the equity market over the last 3 months are consistent with slowing growth as small caps, industrials, transports, materials, energy and homebuilders are all lower, while the Gen AI boom rages on with sharp increases in technology and communication services. Earnings season kicks off on Friday with the big banks, and as we noted in our June 22 note, Earnings Crunch Time, this is the quarter where the recovery from the 4Q22 to 2Q23 earnings recession is expected to broaden beyond the technology and communication services sectors that accounted for all of the 8% 1Q24 earnings growth. Stock price performance and earnings estimate revisions in economically sensitive non-tech sectors suggest it is likely to be a disappointing earnings season.

While the front-end of the Treasury market rallied in response to the weak ISM surveys and employment report, the long end lagged ahead of next week’s auctions of $58 billion of 3-year notes, $39 billion of 10-year notes and $22 billion of 30-year bonds due to concerns that an increasingly likely second Trump Administration and GOP sweep will run larger deficits than a Biden Administration unlikely to control the Senate. As we will explain later in the note, although we suspect some of the Trump agenda inflationary concerns are misplaced, we remain firmly convinced that we are in a structural bond bear market until and unless the government runs a primary surplus and the Fed returns to a ‘bills only’ balance sheet policy.

In this week’s holiday shortened note we will recap the employment report with an eye towards the Fed’s reaction function, discuss the 16 ‘Nobels’ letter voicing concerns about a second Trump administration, and provide a portfolio update.