Targeting 10s

The More Dangerous of the Evil Twin Deficits, the Centrality of Spending, Population Out of Control, Adding More Financial Sector Exposure

“Based on current projected borrowing needs, Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.”

Quarterly Refunding Statement, U.S. Department of Treasury

“In discussing issuance recommendations, the Committee uniformly encouraged Treasury to consider removing or modifying the forward guidance on nominal coupon and FRN auction sizes that has been in the refunding statement for the past four quarters.”

Report to the Secretary of the Treasury from the Treasury Borrowing Advisory Committee

Looking for Volatility in All the Wrong Places

A funny thing happened on the bear steepening (higher rates led by longer maturities) grind to a retest of the October ‘23 5% peak in 10-year Treasury, the Treasury Secretary’s office transitioned from a labor economist who never saw a rate cut she didn’t like, to the first macro hedge fund manager ever to be Treasury Secretary. Assigning all of the attribution for this week’s pre-payrolls short squeeze of Treasury short duration that turned the bear steepener into a bull flattener (lower rates, also led by longer maturities) to Secretary Bessent and President Trump’s pivot to 10s from the Fed’s policy rate, simplifies the narrative, is incomplete, but is significant. The UST rally began with a sharp drop in December job openings ahead of a January employment report that has had big upside surprises the last three years largely due to the pandemic corrupting season adjustment factors (see our Payroll Preview: Another Big January? for details). The rally intensified when Bessent’s first Quarterly Refunding Announcement (QRA) provided guidance that note and bond issuance increases market participants were expecting were on hold, likely until the ‘big, beautiful reconciliation bill’ was completed. The rally may have been fueled by the realization that the DOGE effort might actually build momentum towards returning spending to 20.5% of GDP. Consequently, by the time Secretary Bessent and President Trump made it clear they were less interested in the Fed’s policy rate, and are targeting the 10-year, the short duration, Trump Administration policy skeptics were on the defensive. The rally stalled following the BLS employment Situation report on Friday, but as we explain, the report was a mess and didn’t change our view that the supply of labor is abundant.

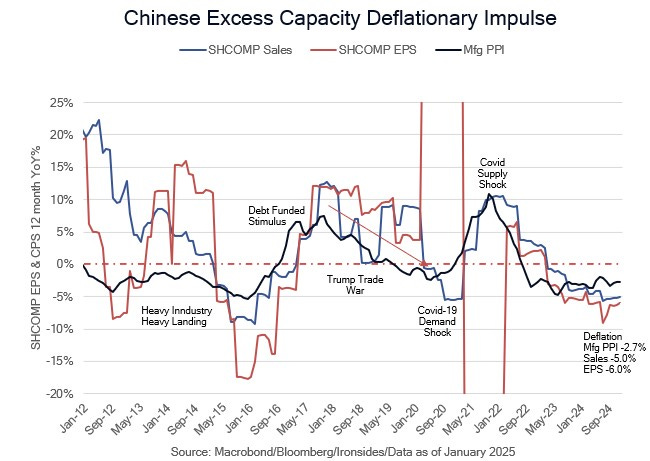

Late Sunday evening, with the S&P’s down 120 points, in discussions with clients, and in our audio and abbreviated video summaries of our weekly Monday morning, we articulated our view that of the evil twin deficits, the larger risk for US equities and Treasuries is not the trade deficit and Trump Administration trade policy, it is our spending problem. Said differently, in our view, the probability increased tariffs cause a negative demand shock that leads to a growth scare and lower stock prices is much lower than a real rate shock like the August to October ‘23 episode. Treasury Secretary Bessent’s analysis of global imbalances during a Bloomberg TV interview on Thursday was astute, large imbalances can result from currency valuation, trade restrictions and interest rate repression, China has the largest imbalance in history and is struggling with manufacturing deflation. That deflation is compelling evidence that until and unless they are willing to rebalance their economic system away from export dependency (mercantilism), they will be forced to absorb tariff increases, leading to additional pressure on earnings, revenues and margins. As Brad Setser from the Council on Foreign Relations (a good X follow if you are interested in global trade and capital flows), posted this week, and we are paraphrasing, all of China’s rhetoric about diversifying their exports is a mirage, China’s massive global current account surplus and the US giant deficit implies they are reliant on US final demand. We agree with Treasury Secretary Bessent, China will absorb the majority of tariff increases in margins, which will deepen their manufacturing deflation.

In this week’s note we cover the Trump Administration’s spending plans, the implications of the massive revisions to employment and the size of the population, and our case for increased exposure to the financial sector.