Payroll Preview: Another Big January?

Why Payrolls Matter, Seasonal Struggles, Underestimated Slack, The Churn Collapse and the Price Theory of Labor Demand

The Payroll Report Still Matters

There are three statistical data smoothing factors that decrease our confidence interval around our standard analysis ahead of Friday’s January employment report. First, during the four years prior to the pandemic, unadjusted employment averaged a loss of 3 million jobs, the last three years we’ve had large upside surprises in the seasonally adjusted report (average forecast beat 301,000) due to much smaller unadjusted declines, for example last January’s unadjusted decline was only -2.635 million. Smaller seasonal hiring is at least partially attributable to the 5.5% increase in ecommerce market share of retail sales to 20.1% from ‘19 to present. BLS seasonal adjustment factor changes could mitigate the effect, the upsides surprises have been smaller each year (416,000 in ‘22, 319,000 in ‘23 and 168,000 in ‘24). The second factor is the annual population control adjustment, a year ago the headline of our discussion of the January report, “Population Control: Where Did Everybody Go?”, we were curious about how the population contracted 625,000 despite the surge in immigration. This adjustment is the divisor for the unemployment rate going forward, but BLS does not revise the rate based on the change. This year there could be a large catchup increase, but we really have no clue. Finally, we get the final annual benchmark revision to the monthly establishment survey, the first estimate in August of -818,000 was a crucial factor in the Fed’s decision to begin the policy rate recalibration (rebalancing) process with a 50bp cut.

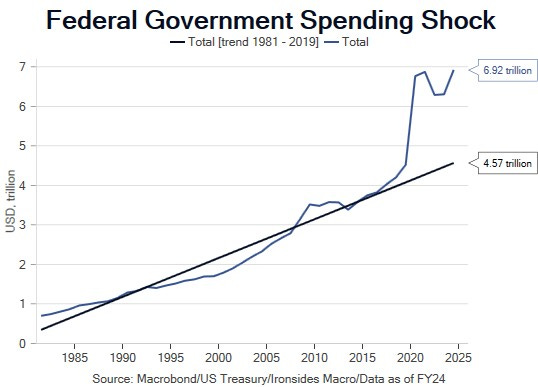

Now that we’ve begun our note with a giant disclaimer, let’s discuss why the report matters. First, we have returned to the twin deficits of the ‘80s, but in much bigger size. Despite all the consternation about the ‘dumb trade war’, as the Wall Street Journal editorial board and a number of economists and market participants characterized the inevitable increase in tariffs (see our explanation on CNBC Asia Monday evening), the trade deficit matters much less for markets than the Biden Administration and 117th Congress’ fiscal expansion that put spending on a path that cannot be financed by receipts, growth, productivity and inflation. As we discussed at length in Nothing Works Without Spending Cuts, the path of least resistance for the Treasury market is bear steepening (higher longer maturity rates), until and unless spending is put on a path to return to the 1981-2019 median of 20.5% of GDP. DOGE is moving fast and breaking things, however, cutting spending that doesn’t align with our foreign policy or political objectives is not sufficient, and most investors we talk to are skeptical that Congress and the Administration can return spending to a sustainable pace. Consequently, the only factor that can keep the bear steepening in check in the near term is weak demand for labor, or disinflation, that prompts the Fed to restart the policy rebalancing process.

On balance, January Regional Federal Reserve Bank Services Surveys, the Conference Board’s Labor Differential Survey, the Atlanta Fed Wage Tracker and Employment Cost Index suggest Chairman Powell’s declaration that ‘downside risks to the labor market have abated’ was premature. That said, the BLS holds all the cards on Friday, data smoothing should resolve the considerable divergence between the resilient current employment situation monthly payroll numbers and much weaker household survey to the downside, but we’d keep our risk in check ahead of the report.