Nothing Works Without Spending Cuts

Inauguration Euphoria, Nothing Works Without Spending Cuts, FOMC 2H25 Recalibration Resumption, Growth Mix Matters, UST Belly Ache, Big Earnings

The Intersection of Trade Policy and Economic Growth with Barry Knapp

Mining Stock Daily

Barry Knapp discusses the current economic landscape following the recent US presidential inauguration of Donald Trump, focusing on trade policy, the treasury market, and inflation. He emphasizes the importance of balancing fiscal and monetary policies, the implications of tariffs, and the need for infrastructure investment. The discussion also touches on the challenges of rebuilding after disasters, energy demands, and the overall outlook for capital expenditures in the context of changing economic conditions.

Inauguration Euphoria in Equities, Treasuries Not So Much

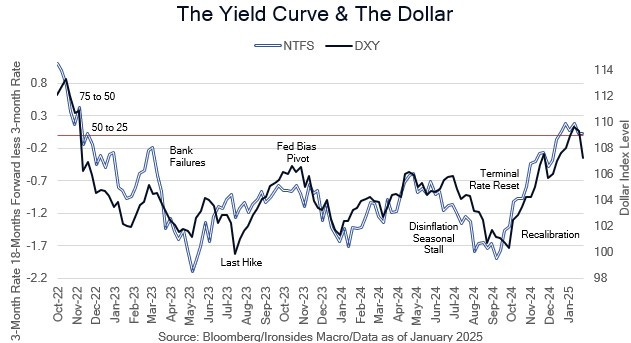

The Bessent nomination hearing and CPI relief rally in Treasuries stalled this week for no obvious reason, the 20-year auction had robust demand, there was no data that impacted the economic or monetary policy path outlooks, the Fed was in their pre-meeting quiet period, nor were there any fiscal policy developments that drove the bear flattening of the curve. The market ended the week with a better tone following a drop in the S&P Global Services Survey. The price action was consistent with our intermediate term view that until and unless Congress proves to the markets that they can place government spending on a trajectory to return to its 50-year average of slightly more than 20% of GDP, the path of least resistance for longer maturity yields is higher as the buyer base evolves from two decades of central bank and exchange rate reserve manager price insensitive buyers to a customer base that expects to get paid for taking maturity risk. The Yellen Treasury and Powell Fed attempted to stall term premium normalization (maturity risk premium) by financing $2 trillion deficits with 30+% short term securities (bills) and a passive reduction in the FOMC’s pandemic ‘emergency’ large-scale asset purchases, but those temporary measures added economic stimulus and exacerbated the largest inflation shock since the late ‘70s. Both issuance and the Fed’s balance sheet restructuring are necessary conditions to stabilize the rate of inflation over the long run, reducing government spending is the sufficient condition. In short, President Trump’s economic team (Bessent, Hassett and Miran) face a formidable challenge, the good news is a retest of 5% for 10-year Treasuries is likely to act as a call to action that forces Congress to forget about approaches like scoring the reconciliation bill based on current policy, rather than current law or using tariff revenue to offset tax cuts, and instead return spending to its longer run rate.

Given these daunting Treasury supply challenges and the constraints implicit in Congress taking something away from the public (cutting spending) relative to giving something to voters (cutting taxes or increasing spending), 5% 10s are probable. Another real rate, higher term premium rate shock would likely be accompanied by the euro below parity, the yen making a 50-year low below 162 and CNH (offshore yuan) at an all-time low below 7.38. Given the tendency for economically sensitive cyclical sectors to struggle when USTs come under pressure, the equity market will likely pullback in a highly correlated fashion that takes no prisoners (yup, even tech). We anticipate buying that correction given the improving outlook for capital spending, productivity and an improved mix of growth resulting from the business confidence post-election surge. Earnings are off to a strong start and the business confidence post-election surge is showing no signs of cooling based on the January regional Fed manufacturing and services surveys. Whether you reduce risk is a function of your investment process, we have a healthy cash hoard we will look to deploy.

In this week’s note we begin with President Trump’s trade, tax and spending policy before previewing the FOMC meeting and monetary policy outlook, as well as the narrow path to a March resumption of the rate recalibration cycle that runs through BLS seasonal adjustment factors. We discuss the advanced estimate of 4Q25 GDP and 1H25 outlook for a better growth mix. We also recap our early thoughts on earnings ahead of big tech and energy reports before ending with our market outlook, including the ability to absorb next week’s Treasury belly supply (2s, 5s & 7s).