Sustainable Disinversion

Equities want 50, Crumbling Labor Market Foundation, Sustainable Disinversion, Recalibration Reconciliation

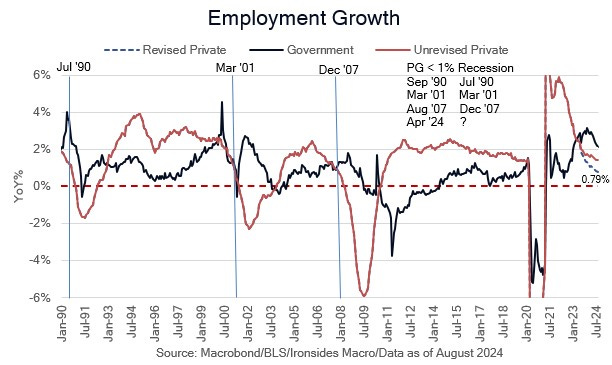

Revisionism

While the equity market briefly took some degree of comfort from the August employment report, it turned sharply negative following the opening of cash trading as it became increasingly clear the Fed is late beginning the recalibration cycle. This week’s labor market reports strengthened our conviction that the small business foundation of the labor market continues to deteriorate. The persistence of negative revisions, combined with this week’s August ADP small business employment and NFIB Small Business Survey suggests by the time the Quarterly Census on Employment & Wages provides a more robust employment estimation; it is reasonably probable that the overestimation of small business employment has increased since March. As we discussed last week in On the Ledge, the upward revision to 2Q GDP to 3.0% is far less meaningful than the first estimate of 2Q GDI at 1.3%, due to GDI’s superior history in measuring the business cycle in real time. Additionally, slow income growth is consistent with slower capital and labor investment. In short, labor market data, adjusted for the overestimation of small business employment, and deceleration in gross domestic income, implies the economy has slowed to stall speed. As we stated on CNBC two weeks ago, we would not be shocked if the economy were in recession by election day.

This brings us to the debate that will intensify during the FOMC quiet period, how will the equity market respond to a 25bp or 50bp initial rate cut. We are increasingly convinced that a 25bp cut will be closely followed by increasing evidence that the soft landing, or Chicago Fed President Goolsbee’s ‘golden path’, is slipping away. Consequently, the Fed is behind the curve narrative will intensify and equities are likely to fall further after the meeting. We reject the idea that a 50bp would trouble the equity market beyond a brief initial rection, the Fed themselves do not purport to know more than the spontaneous economic order. The price action on Friday, the sharp pullback, bounce on headlines from Governer Waller’s speech that appeared to open the door to a 50bp cut, followed by resumption of the selloff as participants read his speech that in our view, suggested the Fed is likely to start the recalibration process with a 25bp cut, implied the market agrees with our view the Fed is late. As we will discuss later, the Treasury market is all in on an aggressive rate cutting cycle, equity investors appeared to come back from the beach and have a collective epiphany this week.

“Determining the pace of rate cuts and ultimately the total reduction in the policy rate are decisions that lie in the future. As of today, I believe it is important to start the rate cutting process at our next meeting. If subsequent data show a significant deterioration in the labor market, the FOMC can act quickly and forcefully to adjust monetary policy. I am open-minded about the size and pace of cuts, which will be based on what the data tell us about the evolution of the economy, and not on any pre-conceived notion of how and when the Committee should act. If the data supports cuts at consecutive meetings, then I believe it will be appropriate to cut at consecutive meetings. If the data suggests the need for larger cuts, then I will support that as well. I was a big advocate of front-loading rate hikes when inflation accelerated in 2022, and I will be an advocate of front-loading rate cuts if that is appropriate. Those decisions will be determined by new data and how it adds to the totality of the data and shapes my understanding of economic conditions. While I expect that these cuts will be done carefully as the economy and employment continue to grow, in the context of stable inflation, I stand ready to act promptly to support the economy as needed.”

The Time Has Come, Governor Christopher J. Waller, September 06, 2024

The overarching issue from an equity investor perspective is 2025 expected earnings growth of ~13% and a market implied monetary policy rate of 3%. The probability of both of these outcomes is exceptionally low, as we will explain in the note, we think equity investors are offsides. The reconciliation of a rapidly deteriorating labor market and elevated earnings estimates won’t need to wait until 2025, Q4 estimates look elevated as well and with our sector net revision models heading south across cyclical sectors, the modest decline in the ‘24 S&P 500 estimate from 243 in April to 239 in August, seems likely to fall further. At 5000 for the S&P 500, an increasingly likely outcome in the near term, we will consider putting some of our healthy cash allocation to work. At current levels, the equity market is exceptionally vulnerable to our 3 ‘E’s’, the economy, earnings and the election.

In this week’s note we will review the employment report and implications for monetary policy and markets. Next week we plan to dig into tax policy as the contours of the presidential candidates takes shape. The only positive development for equities this week was the significant reduction in the probability of a Democratic administration and the associated risk of an increase in the corporate and capital gains tax rates.