On the Ledge

The "3 E's" and our negativity, Income and Investment, August Labor Demand Looks Weaker Still, Jackson Hole, Beyond Powell's speech

Please Talk Us off the Ledge

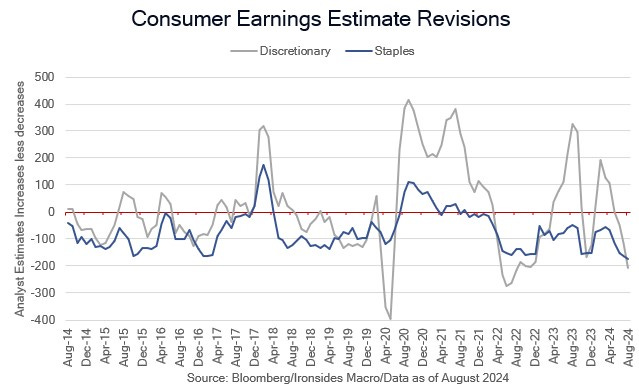

We made a video this week with Dean Curnutt, the CEO of Macro Risk Advisors, for MRA clients, ‘The “3 ‘E’s” and Arguing for Equity Protection’. In short, our outlook for earnings, the economy and the negative skew to the range of election outcomes, suggest the price of protection is cheap. S&P 500 earnings estimates have flattened over the last couple of months, are expected to decelerate sharply in 3Q largely because they are no longer being compared to the trough of the 3-quarter earnings recession, and net earnings revisions are contracting in the consumer discretionary, staples, industrial, energy and technology sectors. Incoming data this week on the labor market, manufacturing, services, capital investment and housing were weak, implying the risk of a not-so-soft landing are growing. The soft-landing proponents, basing their views on an outlook that looks like a consensus given strong equity market performance since the last employment report and the sharp contraction in the price for portfolio protection (VIX is the most widely watched measure), combined with a stalling of the 10-year UST yield at the ‘24 low, will take comfort from the upward revision to 2Q GDP due to stronger consumption. However, the first estimate for the better measure of the business cycle, gross domestic income, was below potential growth due to a sharp deceleration in the net operating surplus of private sector enterprises.

As we will explain in this week’s note, income drives investment, consequently, the average quarterly annualized 1.35% gross domestic income growth rate for 1H24, combined with slowing investment in labor and capital, implies the BEA’s GDP estimate is likely to meet the same fate as BLS’s monthly employment growth numbers. In other words, a large downward revision. Finally, with Vice President Harris’s surrogates actively promoting an increase in the corporate tax rate, capital gains rate and wealth tax, combined with a modest lead in the betting markets, the only potential check on a very negative outcome for the equity market is the Senate where the betting markets are still leaning heavily towards a change in control to the GOP.

The only contra arguments we can construct are policy related. Perhaps the Fed’s change to an abundant reserve regime and the associated $3.3 trillion in bank reserves, long duration holdings that the KC Fed estimates are suppressing the 10-year yield by more than 1%, and the 7% federal budget deficit with spending at 24% of GDP (a record level for a non-recessionary period) are all supporting asset prices and muting the information content and discounting of a deteriorating earnings and economic outlook.

In this week’s note we will discuss the income and investment outlook, work through the latest labor market data ahead of next Friday’s crucial August employment report, review the Jackson Hole Economic Policy Symposium research agenda with an eye towards the Fed’s framework review, and of course, offer our thoughts on asset and sector allocation.