Straight to the '70s?

Policy driven rates instability, deeper and wider inflation, adjusting capex for R&D

We are introducing a new tactical trading recommendation product this week intended to supplement our strategic sector and asset allocation recommendations.

Policy Driven Instability

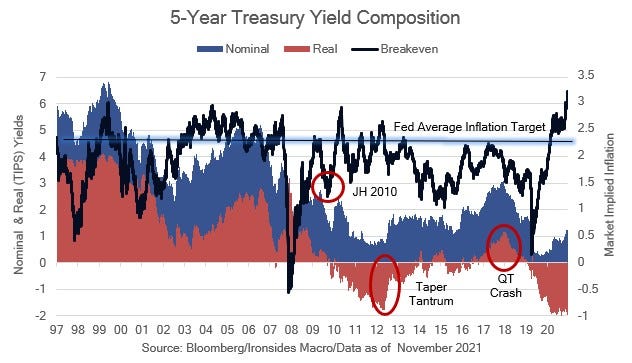

Since the Fed’s optionality assertion at the November FOMC meeting, labor market and inflation data (as well as markets, as evidenced by rallies in bitcoin, gold and inflation breakeven rates) are strongly suggesting the Fed should exercise the option to accelerate the reduction in Treasury and mortgage-backed securities purchases and speed up rate policy normalization. The part of the Treasury curve in the sweet spot of Fed purchases is undergoing a historic divergence as the Fed prepares to begin reducing purchases. 5-year inflation breakeven rates reached an all-time high of 3.17%, and 5-year real rate (TIPS yields) are at an all-time low. The message from the belly of the Treasury curve is that the reduction pace is too slow given the inflation outlook (breakeven rates up) and the Fed is continuing to cause an extreme imbalance in the market (real rates down). Also, our Fed policy proxy moved up by an additional 16bp last week, almost another rate hike over the next two years. Equities struggled with the inflation data, but rebounded led by reflation sectors due to the improving growth outlook, favorable seasonality, and perhaps a naive expectation that the Fed will get around to focusing on price stability.

As we discussed in last week’s note, Credibility, and during a CNBC appearance immediately following the CPI report, the Fed is headed for a crisis if they continue with the current passive taper pace and the data continues to exceed expectations. The combination of the latest round of inflation data, and the Fed’s complacent response, gave a modest shake to our confidence that a benign period of reflation will precede ‘70s style inflation. In other words, the policy risks are rising and the post-FOMC round of speeches gave no indication that they would exercise the option to speed up the taper even if the November employment and inflation data continued the momentum evident in the October reports released after the FOMC meeting. They do not appear to be data dependent.