Credibility

Growth is good, Fed optionality assertion or credibility crisis, small cap upgrade

We were traveling late this week, please excuse the reduced number of charts and tables

Growth is Good

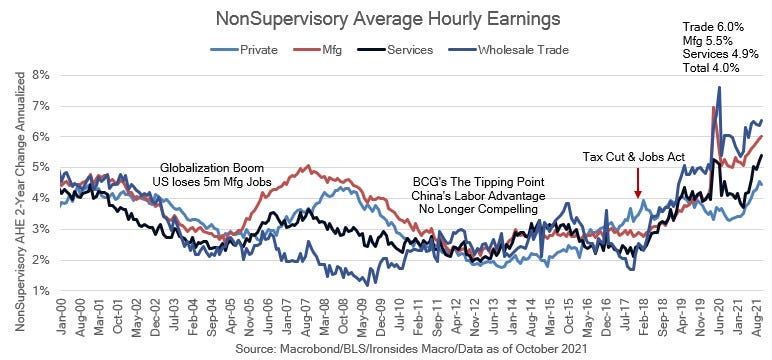

As we expected, October employment gains beat the street and the previous two months were revised higher by 235,000. Additionally, wages were strong and the unemployment rates fell by more than expected. The employment ratio for prime age workers continued to improve but aggregate participation fell likely due to retirements and other factors including increasingly generous government support programs and slower immigration slowing growth of the labor force. We will do a deeper dive when we get the JOLTS report next week, however, measures of labor slack continue to show a tight labor market led by the most important measure, wage growth. Nonetheless, while the Fed attempted to add optionality to the taper process, the market isn’t buying it as evidenced by Friday’s equity and Treasury rally led by real rates. For now, the combination of favorable seasonality for equities, an improving growth outlook and easy monetary policy is favorable for risk assets.