Powell Reappointed: 1st Thoughts

Powell Reappointed: 1st Thoughts

One small step for independence

We are making this flash update available to all subscribers, if you are only receiving the free summaries please consider upgrading ahead of our three-part outlook series coming in December.

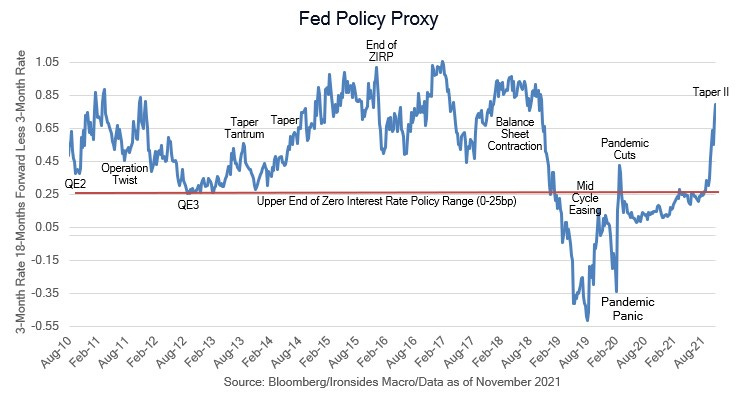

President Biden’s reappointment of Fed Chairman Powell and promotion of Governor Brainard to Vice Chair for Monetary Policy was incrementally positive for Fed independence and reduces the probability of a Fed credibility crisis. As we wrote in Saturday’s note, another politically motivated Fed Chair appointment following President Trump’s replacement of Chair Yellen with Powell, risked a repeat of the Nixon/Arthur Burns ‘70s scenario that was a major factor in the Great Inflation. That said, market participants still believe the Fed needs to accelerate the pace of reduction of asset purchases as evidenced by a sharp rally in front-end TIPS yields (real rates) and move higher in Fed policy rate expectations. In other words, the Fed’s optionality assertion needs to be exercised at the December FOMC meeting. Wednesday’s November FOMC minutes may offer insights as to whether the optionality assertion was merely a concession to the handful of FOMC participant hawks or an actual shift from the measured removal of policy accommodation 2004-2006 innovation that has been characteristic of policy normalization since.

The immediate reaction was favorable, equity reflation sectors rallied despite a sharp move higher in front-end real rates. The dollar rallied against other major currencies, bitcoin and gold, but was flat against emerging market currencies. This combination speaks to market participants views on Fed credibility. There are additional appointments to come as well as two regional bank presidencies. The trajectory of bank regulatory policy remains likely to tighten, the vice chair of supervision remains open and there will be considerable pressure from Senators Warren and Brown to appoint a regulatory hawk particularly if the Omarova OCC nomination collapses. Questions about a Fed payments system, a central bank digital currency (CBDC), a Fed deposit system and other intrusions of the central bank into the private sector are far from resolved. Additionally, when analyzing the outlook for monetary policy, the differences between Powell and Brainard’s views are less important than Clarida and Brainard. We wrote earlier this year that Governor Brainard was the third person in the leadership rather than NY Fed President Williams, given Powell’s lack of monetary policy credentials, Brainard becomes even more influential in monetary matters with Clarida’s departure. The Fed will be under pressure through the cycle to facilitate the growing federal debt. The ‘60s analog when the Fed was ‘independent within, not of the government’ and the dual mandate bias shifted from inflation to employment is intact, though it does not appear we will not skip straight to the ‘70s. This is good news for the reflation bias of our tactical portfolio, but the Fed remains on a path towards less credibility in 2022.

Barry C. Knapp

Managing Partner

Director of Research

Ironsides Macroeconomics LLC

908-821-7584

bcknapp@ironsidesmacro.com

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.© 2021 Ironsides Macroeconomics LLC.