Payrolls Preview: Remain Calm

Bad is good for bonds, and probably stocks as well

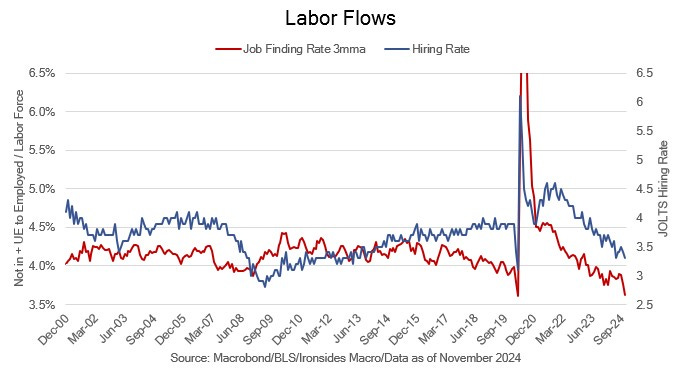

Negative Skew

In last week’s note, Beware January Reversals, we detailed our view that the benchmark 10-year Treasury note remains overvalued, even after a 100bp increase in yield since the FOMC’s 50bp kickoff of the rate recalibration (cut) process. Decomposing the 100bp increase in rates, only 20bp is attributable to expected inflation, conversely the real rate (TIPS yield) increased 80bp and the Adrian Crump & Moench term premium model increased 83bp. In short, the sharp repricing of longer-term Treasuries is attributable to a combination of market implied growth and supply. The early stage of the selloff was driven by a strong September employment report and sharp increase in the annual benchmark revision to gross domestic income. More recently, economic surprise weakened, and the supply outlook deteriorated. Recall the very large tail of the 5-year TIPS auction following the December FOMC meeting when the Committee cut the policy rate 25bp bringing the total ‘recalibration’ to 100bp. Characterizing the 100bp increase in 10s, while the FOMC cut rates 100bp, as unusual is an understatement. We are in the midst of our third major warning sign the US is reaching its fiscal limit, the first was 1Q21 during the Biden Administration’s $1.9 trillion stimulus process. The second was 3Q23 when the Yellen Treasury attempted to increase issuance of notes and bonds by $500 billion. A combination of Activist Treasury Issuance and monetary policy easing stopped the first two bear steepening shocks, it’ll be more challenging this time.

This brings us to Friday’s employment report, while a weak report seems likely to stop the selloff, it probably won’t result in a continuation of the FOMC rate recalibration process in January. First of all, a number of the Committee members view the Trump agenda as inflationary and a risk management approach to policy implies a pause in the cutting cycle. Secondly, the Committee is probably smarting from criticism they overreacted to this summer’s growth scare when they kick started the process with a 50bp cut in September. The last two January employment reports have been exceptionally strong, setting them up for a repeat of September when their cut was immediately followed by a strong employment report. Although the pandemic policy panic’s impact on seasonal hiring patterns and the BLS data are easy to explain away, we doubt FOMC participants want to risk spending the majority of their post-meeting speeches discussing the vagaries of BLS data.

Consequently, although we continue to view demand for labor as weak, the balance of risks for Treasury and equity investors is skewed negatively. In other words, the Treasury market is likely to continue its path towards 5% on 10s on either an inline or stronger than expected report. Additionally, as we explained in last week’s note, the equity market is not looking through the bear steepening of the Treasury curve as evidenced by weak relative performance of the equal-weighted S&P 500 (-6.7% from the late November high) and cyclical sectors over the last month. If 10-year nominal and real rates approach their October ‘23 highs at 5% and 2.58%, a highly correlated across equity market sectors and asset classes risk-off shock is probable.

Our inclination is to add risk if that scenario unfolds, in part because we expect it to sharp the focus of the incoming Congress and Administration to address the core problem, record non-recessionary deficits and spending and aggressive debt management. But first let’s discuss the outlook for Friday’s December employment report.