It’s What They Pay

Realizing a lower VIX, Political Calculus, Finally the FOMC Quiet Period, Manufacturing rebound, A Decent Start to Earnings

It’s What They Pay, Not What They Say

The decline in the CBOE Volatility Index, known by its symbol as the VIX, to 16.2 on Wednesday led to some excited reporting and commentary about investor complacency. We disagree with this interpretation for a number of reasons. First, the median since the VIX was introduced in 1990 is 17.88, so the current reading is less than .2 standard deviations below the median. Second, as we noted last week, since the Silicon Valley Bank collapse, 5% one-month out-of-the-money call implied volatility dropped 3% while 5% out-of-the-money puts are unchanged. The CBOE Skew (puts relative to calls) Index is 1.9 standard deviations above its longer-run median. Third, the spread between 6-month and 1-month VIX futures widened from a brief inversion in early May to 6.8%, nearly one standard deviation steeper than the longer-run median. In other words, while short-term VIX futures dropped, longer term futures remained expensive relative to 11% actual or realized market volatility over the last month.

Low realized volatility is at least partially attributable to the abundant liquidity regime we discussed last week. On balance, the premium of puts relative to calls (skew) and longer maturity index options relative to short term options (term structure) implies investors are willing to pay a high price for portfolio insurance. The price investors are willing to pay for protection combined with rich valuation of defensive sectors points to cautious investor positioning, not complacency.

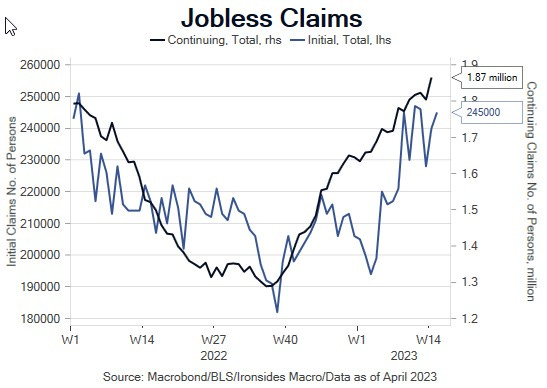

Another way to think about the decline in the VIX is that the abundant liquidity regime is reducing realized volatility in equities, fixed income and exchange rates, but as we described last week, and will discuss further this week, liquidity is likely to undergo another tightening shock following a debt ceiling deal. Additionally, the latest round of Fed speak implies the FOMC is going to hike an additional 25 basis points in early May, despite acknowledging that demand for labor is cooling and credit is tightening. With the timeline for reaching the debt ceiling pulled forward by lower tax receipts (capital gains), and the Fed willing to wake up more sleepy depositors and deepen the curve inversion further pressuring bank net interest margins, the abundant liquidity regime that is reducing realized market volatility is likely to deteriorate by early June.