Incredibility

Fiscal stagflation, currency chaos, the Sahm Rule and who will buy the bonds

Fixing Fiscal Profligacy with Monetary Medicine

“Under the third scenario – when the monetary authority responds to inflation as in the Monetary-led regime but without fiscal backing – not only does inflation increase persistently, but it takes an explosive path. The shock to spending determines an increase in the fiscal burden, causing inflationary pressures. The central bank reacts by increasing rates, causing a recession. The recession and a higher cost of financing debt further increase the fiscal burden that in turn generates additional inflationary pressure. In this case, not only is the central bank unable to lower inflation, but by increasing rates it is causing even more inflation and economic stagnation. We call this outcome fiscal stagflation.”

Inflation as a Fiscal Limit, Francesco Bianchi, Leonardo Melosi

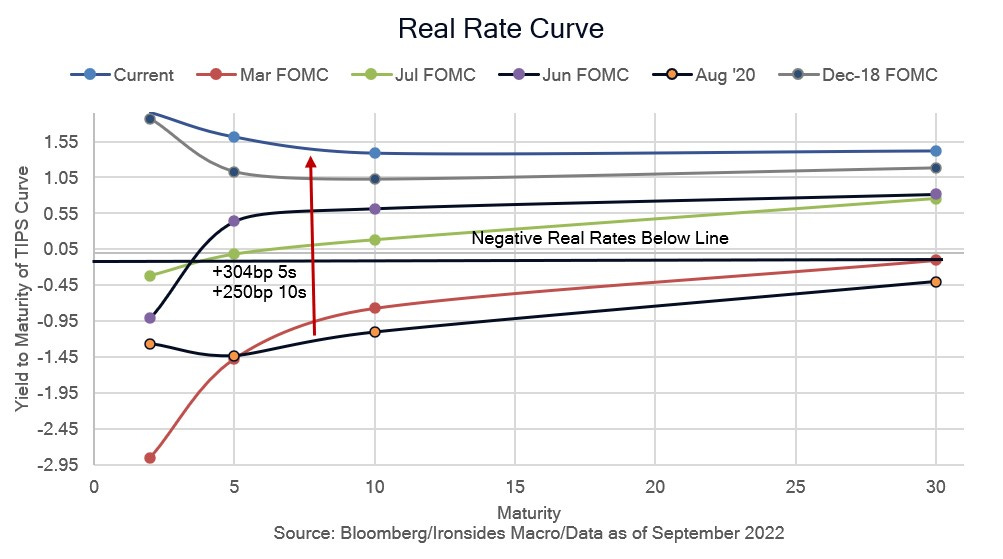

We’ve been referring to this paper since its presentation at the Kansas City Fed Economic Symposium (Jackson Hole) due to its consistency with our '60s analog and the reversal of transitory disinflation in housing, healthcare, education and the labor market, from pandemic support programs to fiscally driven services inflation. The reaction to the FOMC meeting, with yield curve flattening and sharply lower equities, was a taste of fiscal stagflation. In our meetings in Boston and New York we received little pushback on our forecast that the path of 8% CPI to 4% is fairly clear: core goods, food, and energy are highly likely to negatively contribute while base effects from white hot inflation in 4Q21 and 1Q22 will push all items CPI sharply lower. However, with transitory pandemic policy disinflation in core services transitioning to more intractable fiscal driven shelter, medical and education inflation, combined with deglobalization and the resultant end of two decades of goods deflation leading to significantly higher trend inflation, this will create a major hurdle for markets in 2H23 into 2024. The markets will hit a wall of high yield and leveraged loan maturities that financed a large amount of private equity malinvestment, much of which won’t make sense with significantly higher financing rates.

While the Fed has regained inflation fighting credibility, they have not regained forecasting credibility. Consequently, though we think the message they delivered with the DOT plot was not warranted by the data since the last FOMC meeting, and the risk of a macro mishap was evident less than 24 hours later when the BOJ was forced to intervene to strengthen the yen, our base case remains a recovery in equities as inflation falls towards our 1H23 4% forecast target. Sentiment is even more extreme than when we commented on it several weeks ago, as the AAII survey bullish less bearish investors is at the most bearish reading in the history of the survey. Add equity exposure with the understanding that the likely catalyst for a near term change in outlook for monetary policy requires a disorderly tightening of financial conditions — in other words more downside in equities. As we move into October, we expect the inflation data to improve, however, the Fed does not appear particularly data dependent and is already breaking things. Monetary and fiscal policymakers made an absolute mess of the pandemic, now they are making a mess of the recovery.