Governance

Risk on, governance not grievance, the path from 9 to 4, China still uninvestable, another big week for macro

Let ‘em Rip

Of all the impressive elements of last week’s risk-on rally, the dollar index (DXY) is arguably the most comprehensive macro measure and is down 5.3% since the FOMC meeting when the Committee tentatively agreed to slow the pace of hikes. The move accelerated this week due to a softer than consensus consumer price index, with a bit of help from the news that the Russians are retreating from Kherson and the Chinese Central Committee is retreating from their Zero Covid policy. The path from 9% to 4% consumer price inflation has been clear to us for months, and following the October CPI report it should be obvious to FOMC participants as well. As we discussed in last week’s note Three Questions, the Committee had already decided to slow the pace prior to the October employment report, and the Chairman’s view that the terminal policy rate was higher than the September summary of economic projections forecast was not shared by the entire committee. FOMC participant appearances this week appeared to confirm that there is a debate about how far to hike. We believe that a 25bp hike in December and a pause is a possibility, assuming two things. First, if the weakness that was evident in the October employment report (slowing wage growth, flows from employed to unemployed and out of the labor force report and the drop in the household survey) leads to further deterioration in the November report. And second, if the November CPI, released the day before the December FOMC meeting, offers further evidence that inflation is cooling.

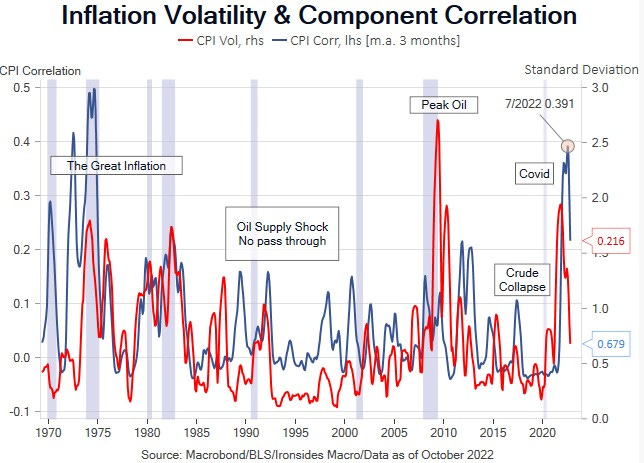

The 215-point rally in the S&P 500 and 30bp drop in 5-year Treasury yields were both impressive. But the 13bp drop in fixed implied volatility MOVE index, 54bp drop in the Fannie Mae Current Coupon 30-year rate, and 3% rally in the yen and pound, steepening of the VIX futures curve all highlighted how out of consensus our inflation, Fed policy path and year-end risk-on rally forecasts are. As we listened to a parade of economists and FOMC participants, who all thought the pandemic was a deflationary shock, urge caution because shelter and services inflation remains hot, the contrarian hairs on the back of our neck stood up and we got even more bullish. The quarterly annualized rate of the Case Shiller 20-City Composite House Price Index was -7.3% in August when mortgage rates were 5.5%, the October Apartment List Rents Index was -2.9%. The CPI furnishing and appliance measures are down sharply from peaks in June and March when house prices were surging. Additionally, as we discussed last week, nonsupervisory average hourly earnings have slowed by 1.3% from the March peak. While the CPI shelter and core services annualized measures are not yet falling, our framework for inflation momentum, the correlation of the top 20 components is plunging. Consequently, if Cleveland Fed President Mester is referring strictly to annualized CPI the quote below is defensible, but as an FOMC participant tasked with stable prices, it is either coercive forward guidance or uninformed.

MESTER: INFLATION STILL BROAD-BASED, SERVICE PRICES NOT SLOWING