FOMC Stress Test

Rebalancing, second order dollar effects, curve inversion, monetary policy & banks

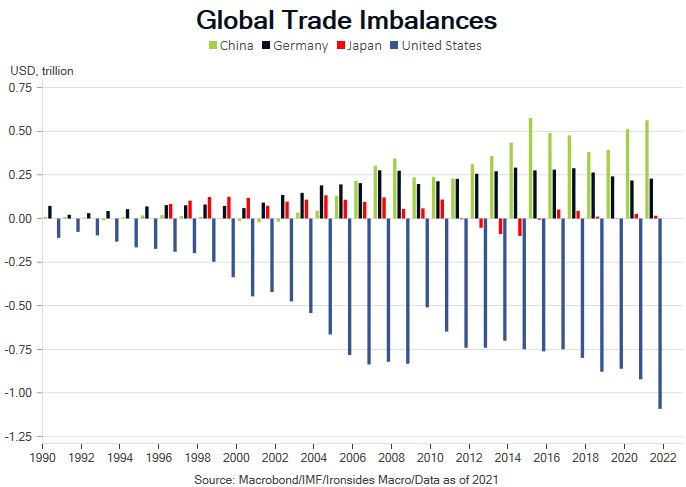

Rebalancing is a Process

Our peak inflation and hawkish monetary policy expectations thesis suffered two major blows this week from the June CPI (see CPI: Ouch) and Atlanta Fed Wage Tracker reports. The Treasury and equity market resilience initially appeared surprising, however the producer price index, import prices and University of Michigan 5–10 year inflation survey were significant offsets consistent with the strong dollar, falling breakeven inflation (the Fed calls this inflation compensation, it is the difference between nominal and inflation protected Treasury yields), and plunging commodity prices. Our view that prior to this week, that the data did not support another 75bp hike was mitigated by the CPI, however by the end of the week the cumulative data did not support a 100bp hike either, leaving our peak hawkishness thesis intact despite the breadth and momentum of 2Q22 consumer price inflation. The initial reaction to the first major bank to report earnings was also an overreaction: bank credit is not deteriorating (more later on this), net interest income is surging, and the profitability outlook for core banking operations is improving due to a favorable asset mix shift. We remain convinced that equities are bottoming and while the term premium on longer term Treasuries is too low, largely due to the Fed’s suboptimal tightening process (passive balance sheet contraction), the worst of the rate shock and liquidity tightening is behind us.

“Bullard: Stronger Dollar Will Mean Less Inflation in the U.S.” Bloomberg, July 15, 2022