CPI: Ouch

Food, Energy, Shelter, Vehicles, and Medical Care

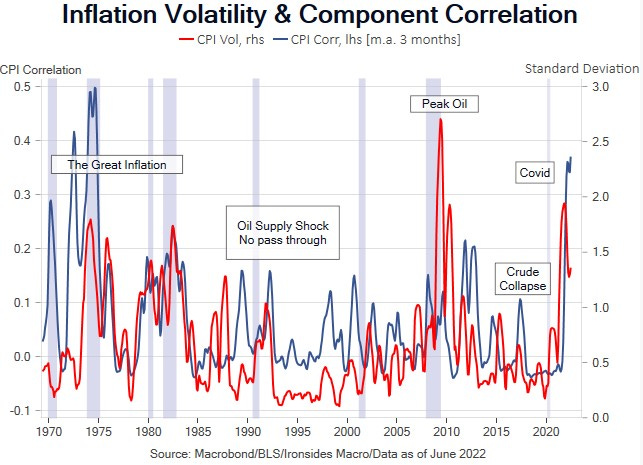

Straight to the ‘70s

While there has been plenty of evidence in futures markets that inflation is peaking, the June CPI report increased the probability that the pandemic policy responses condensed the inflation process that took the entire ‘60s decade, into a single year. Given 20+% declines over the last month in front month crude, gasoline, natural gas, copper, industrial metals, wheat and corn, an 11% year-to-date increase in the trade weighted dollar, 7% drop in the Manheim used car price index, deceleration in average hourly earnings from 0.5% per month in 4Q21 to 0.4% in 1Q22 and 0.3% in 2Q22, the sharp slowdown in housing activity following the 300bp mortgage rate spike, a 50bp drop in 10-year breakeven inflation and 122bp plunge in the near term forward spread, our base case is still that as the economy rebalances, inflation will ease, albeit to levels above the globalization disinflation regime of the ‘90s, ‘00s and ‘10s. In other words, despite the breadth of inflation in the June report, our base case that inflation and market expectations of monetary policy tightening are peaking, remains intact. That said, the impact of the pandemic policy errors was larger than we expected, and the probability of additional policy blunders remains high.