Dynamism Destruction

U3 4.25% is 'Unexpected Weakness, less skilled workers UE rising, dynamism destruction, another monetary policy mistake, hold onto your cash and your seat

The Chickens Came Home This Week

We’ve been arguing for some time that the foundation of the labor market, small businesses, was weak due to misguided monetary policy, and though the BLS struggled to measure the largest contributor to total employment, it would be increasingly evident that the Fed needed to disinvert the yield curve by cutting to 4%. This week’s Conference Board Labor Differential, JOLTS, Employment Cost Index, Jobless Claims, and the shocking (not to our readers) jump in the U3 unemployment rate to 4.25% from 4.05% and U6 underemployment rate to 7.8% from 7.4%, sent a clear signal that Fed Chair Powell’s characterization of the labor market as normalizing is overly optimistic and inconsistent with a risk management policy approach. In our preview note, Labor Demand Convexity, we modeled the risk of any further weakening of labor demand on unemployment. Friday morning the chickens came home to roost. We never changed our 2024 outlook note’s forecast for 100bp of cuts this year, after a wild ride that forecast looks increasingly likely to be realized beginning with a 50bp cut in September.

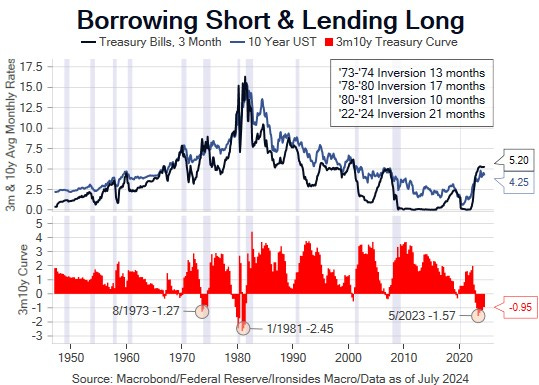

At Wednesday’s press conference Chair Powell violated the first rule of Ironsides Macroeconomics, ‘it’s never different this time’, when he dunked on the Sahm Rule by dismissing it as a ‘statistical regularity’ and went on to describe the ‘unique’ conditions the pandemic (policy reaction) created. We place his approach alongside politicians who dismiss Hauser’s Law, an empirical observation that regardless of the progressivity of the income tax code, government receipts have never exceeded 20% of GDP. In short, when Congress spends 24% of GDP, the deficit cannot be closed through changing the tax code, though we acknowledge a national value-added tax like we see in many European countries might be a different story. More to the point, Powell’s dunking on the Sahm Rule is similar to the widespread dismissal by FOMC participants and market participants of the deepest inversion of the yield curve since the Volcker Fed that sent the Thrift Industry down the road to ruin. The deep inversion of the curve, a consequence of aggressive purchases of longer maturity Treasuries and mortgage-backed securities in ‘20-’22 and passive reduction of those holdings, created inequality between large businesses with access to longer-term financing and small businesses, large and small banks, as well as within the household sector where owners of assets benefited while those living paycheck to paycheck continue to struggle with the price level inflation shock.

The FOMC does have the ability to disinvert the curve, however the impact of their holdings of longer maturity Treasuries and mortgage-backed securities, as well as the inflationary impulse from accommodative fiscal policy, implies the magnitude of the cuts required for curve normalization is greater than what is justified by the inflation mandate. Accommodation emanating from the balance sheet was evident in the bank profitability proxy 3m10y UST curve that deepened its inversion 29bp to -1.43% this week due to the sharp rally in the belly of the Treasury curve. The FOMC is likely to be reluctant to cut to 4%, the level our work suggests will relieve pressure on small banks and businesses, and with the belly rally bank losses on securities are smaller, but curve disinversion is further away. The most likely conditions that will prompt the FOMC to cut to 4% is ‘unexpected’ labor market weakness. We’ve been making the case for most of ‘24 that the equity market is unlikely to look through below potential growth and a labor market with an excess of supply. Thursday’s big rethink of the Fed cutting because they have to (employment mandate miss), rather than because they can (disinflation), is the latest warning sign that bad data, likely to get worse, is bad for stocks. The Fed’s policy mistake runs much deeper than not cutting in July, it began in early ‘22 with passive balance sheet contraction and aggressive rate hikes that caused the deepest curve inversion since the Volcker Fed.

One quick point before we move to the details: unemployment for less skilled workers jumped sharply in July, with less than a high school education going to 6.5% from 5.3% and no college to 5.5% from 4.9%, combined with the pressure on wages in sectors requiring low skills suggests immigration is weighing heavily on the lowest income workers. Additionally, prime age participation, both men and women, jumped sharply and are well above pre-pandemic levels to 90.0% from 89.2% and 78.1% from 76.9%. This is likely due to the wide gap between the consumer price and wage level pandemic policy shocks. In other words, lower income workers are struggling to make ends meet. The FOMC has taken comfort from the increase in supply of labor, the public is struggling with immigration and the inflation price level shock.

In this week’s note we will review the July employment report, the Fed’s policy mistake, monetary policy deleterious impact on economic dynamism and provide our latest thoughts on sector and asset allocation.