Don't Fight the 2s

Fed fighting the 2s, 3-month macro rule, disinflation, banks on track for a face ripping rally

It’s Their Story and They’re Sticking Too It

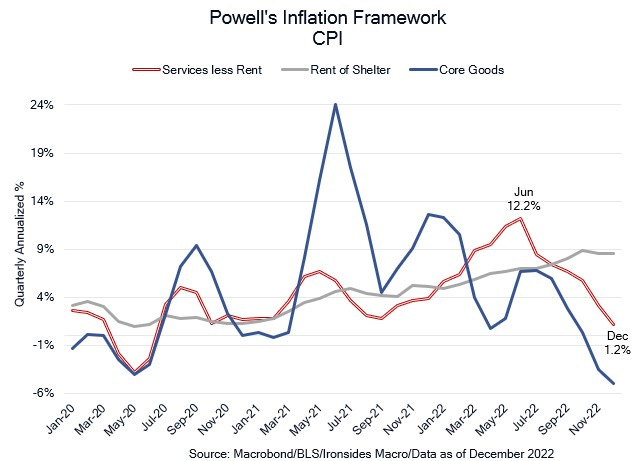

In last week’s note, Return to Normalcy, we explained why the Fed’s case for additional rates hikes had been weakened considerably by sharply decelerating nonsupervisory average hourly earnings in services producing industries. Thursday’s CPI services less rent of shelter reading was yet another significant setback. In Q4, while Chairman Powell and the Committee were concerned that excessive labor demand was causing cost-push wage spiral in the services sector, CPI services less rent of shelter increased 1.2% annualized from a peak of 12.2% in June and average hourly earnings for nonsupervisory service producing industries increased 4.1% from a peak of 7.8% in December 2021. This softening of wages and deceleration of prices occurred despite strong demand for services due to reopening dynamics in 2Q and 3Q. Weakening their case for a wage price spiral further is that two sectors, education & health and professional & business services, that account for 55% of the excessive job openings over hiring, have annualized wage growth of 4.1% and 4.8%, well off early 2022 peaks of 8.4% and 7.5%. We also received the December Atlanta Fed Wage Tracker report this week. It is a 3-month average, consequently it lags the AHE series. Wage growth for paid hourly workers was 6%, down from 7.1% in July, wage growth eased for job switchers, prime age, services, the headline series and the spread between the bottom and top quintile as well as switchers less stayers. The 4Q22 employment cost index is released on the first day of the Fed’s January 31-February 1 meeting, and it will be shocking if it doesn’t confirm the average hourly earnings and Atlanta Fed Wage Tracker wage deceleration.

Early on in Powell’s tenure as Chair he gave a speech expressing humility about the Fed’s ability to set policy based on models for u*, the equilibrium unemployment rate, and r*, the neutral policy rate. Here we are 5 years later, and they threw lighter fluid on a forest fire set by fiscal authorities in 2021 and a year later they still have no idea how the inflation process works. Yet if we are to take their attempts at forward guidance literally, they have supreme confidence that r* is greater than 5% even as the 2-year Treasury falls further below their current setting of 4.25%-4.5% at 4.15%. The near term forward spread, which they assert has more information content concerning the economic and policy outlook than curves anchored to 10-year notes, is 89bp inverted. The traditional recession curve, the 10-year note less the 3-month bill, is 114bp inverted. So much for humility. We do not take them at their word, and various officials have acknowledged the next hike is likely to be only 25bp and based on our expectations for the trajectory of inflation, wage and activity data, that will be the last for some time. Their word is in fact a form of forward guidance; they won’t change the ‘we are going above 5% and staying there all year’ story, until they do.