Return to Normalcy

Wage gamechanger, asset deflation and QT, a bank credit deep dive and a return to normalcy in labor markets.

Will the Federalies Move the Goal Posts?

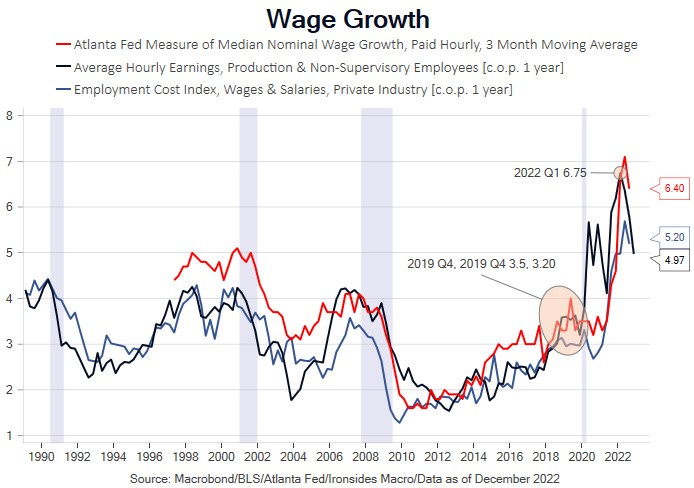

The Fed’s mandate pivot to wage growth received indisputably good news on Friday morning. As Chairman Powell detailed in his Brookings speech, core goods prices are cooling rapidly, this week’s ISM manufacturing survey had a lower prices-paid reading at 39.4 than the low during the US/China trade war global manufacturing recession in 2019. Rents are headed lower as well; the Apartment List rents measure fell 10.3% in Q4 annualized. This leaves services less rent of shelter, and the Chairman’s view that view that this component of inflation, despite two very tame CPI readings, is the major area of inflation risk due to unsustainably high wage growth. Assuming the Fed sticks to this framework the December employment report was a game changer. Nonsupervisory average hourly earnings for service providing industries eased from a downwardly revised 5.44% November reading to 4.88% in December and a peak of 6.99% in January. Disinflation in services wage growth is all the more impressive given the surge in demand for services in 2022 (3Q 3.7%, 2Q 4.6%) as consumption rebalanced from goods to services. While the unemployment rate fell back to 3.5%, the low for this cycle, nonsupervisory average hourly earnings, the employment cost index and Atlanta Fed wage tracker were all in the 3-3.5% range with a 3.5% unemployment rate pre-pandemic. We will have more on this later in the note.

We heard from two of the more hawkish regional Fed Presidents this week, Bullard and Bostic, that the debate was now 25 or 50bp for the next meeting. We suspect the data will continue to warrant a 25, and the early Feb hike will be followed by a pause. We’ve called them out on the lack of data dependency, as the 50bp increase in the summary of economic projections (SEP) terminal rate forecast in December followed two very weak readings for services less rent of shelter CPI (-0.1% in October and 0.0% in November). The Treasury market wasn’t buying the SEP forecast in December and following this morning’s wage data and sharp contraction in the ISM services survey led by new orders and employment, 2-year notes are 80bp below the Fed’s terminal rate forecast, the 3-month/10-year curve is 104bp inverted and the near-term forward Treasury spread is -68bp. Interest rate implied volatility dropped sharply, mortgage spreads tightened, real rates led the drop in nominal yields, and though the curve flattened sharply, it steepened 1 and 2-years forward in anticipation of easier policy.

There is no justification for continued rate hikes, the rebalancing of consumption and associated inventory and trade cycle are largely complete, consumer prices and wages have been cooling since 1Q22. The rates and equities markets are screaming stop at the Fed, and it is time to listen. In this week’s note we are going to provide additional support with a deep dive into bank credit creation for our view that the appropriate analog is 1995, when the markets took off ahead of a secular boom in capital spending.