April Payrolls: Churn Collapse

April Payrolls: Churn Collapse

Immigration, Churn, Fewer Vacancies, Fiscally Driven Demand, Jobs Less Plentiful, Fewer Hours, Too Early for our Quadrilemma Resolution

Churn Collapse

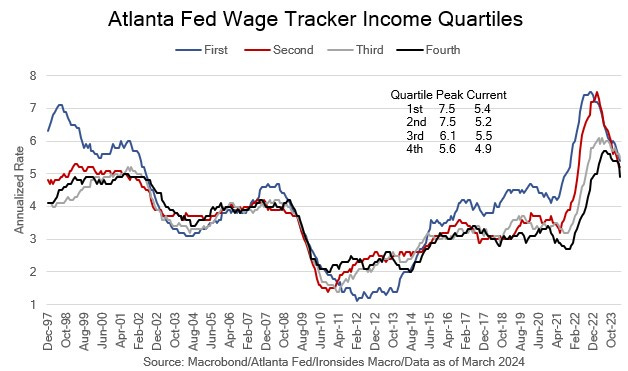

As we started digging into labor market data in preparation for this note, our Bayesian prior was that the stabilization of demand for labor at a relatively robust pace that developed in 1Q24, was likely to have continued in April. Initial and continuing jobless claims were remarkably (unbelievably) stable at low levels. The April ADP report was close to the consensus forecast for BLS private sector payrolls and March was revised up marginally. April Regional Federal Reserve manufacturing employment surveys were marginally weaker at contractionary levels, however the ISM manufacturing employment increased, though it is below the expansion level. Regional Fed services surveys were flattish in expansion territory despite S&P Global concluding that services employment is weakening. In other words, the most widely watched labor data was inconclusive, however, as we dug into the data, we found several potential cracks in the surging foreign-born labor supply is efficiently bringing the labor market into balance FOMC participant narrative. As we detailed in our April 20 note, Unhealthy Broadening Out, we are unconvinced that the increase in immigration was putting downward pressure on wage growth for most of the income strata, yesterday’s stronger than expected employment cost index, led by the public sector (government), offered further evidence supporting our thesis.

The most disturbing labor market trend is the collapse in churn. Worker reallocation, the quarterly sum of hiring and separations expressed as a percent of total employment, has plunged 2.6% over the last year to levels last seen in the summer of ‘14 when the Kansas City Fed was organizing their annual conference to focus on labor market dynamics to explain why the recovery from the financial crisis was so weak. At that Jackson Hole conference Davis and Haltiwanger presented their paper that introduced the reallocation concept, Labor Market Fluidity and Economic Performance. FOMC participants view the falling quits rate as a sign of softer demand and better balance, and while lower churn will bring down wage growth in the near term, in the longer run it is a productivity killer.

Additional issues we will discuss in the note include a sharp drop in the Conference Board Labor Differential and potential increase in the unemployment rate, regional Fed manufacturing and services work week declines in August and a sharp negative revision to 3Q23 employment due to new data on small business ‘deaths.’ Of course, we will also provide our outlook on labor demand, supply and wage growth. A lot is riding on Friday’s report, strong wage growth following the 1Q24 employment cost index, particularly if non-housing services CPI continues to run at the 10-month median monthly rate of 0.4%, should cause the FOMC to rethink their ‘sufficiently restrictive’ view. A risk-off episode triggered by 10-year Treasuries retesting 5% hangs in the balance.