Waller's World

Stable, Above Potential Demand, Waller and r*, Post-Election Policy Calculus, Our Field Trip to NYC

“A couple of participants commented that it would be useful to begin discussions regarding the appropriate longer-run maturity composition of the SOMA portfolio.”

“Various participants mentioned a willingness to tighten policy further should risks to inflation materialize in a way that such an action became appropriate.”

Minutes of the Federal Open Market Committee April 30–May 1, 2024

Various Hawks

In our meetings in NYC this week we were frequently asked about our highest conviction position, and we responded it was short duration, in other words no maturities longer than 2-year Treasuries. Our healthy cash allocation alongside healthy positions in high volatility industrial, energy, materials technology, communication services, and consumer discretionary sectors, combined with a fixed income underweight concentrated in the front-end, leans into our view that the dynamic private sector will overcome misguided policy, but not without periodic policy shocks. As we explained on CNBC Squawk Box on Tuesday, even with a healthy cash position the total portfolio volatility is marginally greater than the S&P 500 and we are in a position to add exposure if we get a risk-off correction due to a real rate driven bear steepening that retests 5% for 10-year USTs or a labor market growth scare related correction.

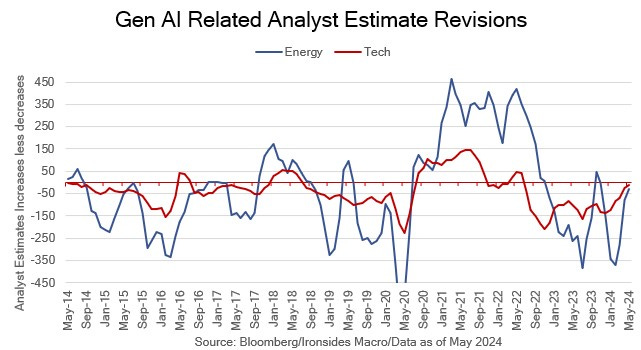

We were also asked early in the week if disappointing Nvidia earnings would have a bigger impact on the equity market than a hot May employment or CPI report that pushed the promised rate cut beyond the election. In broad terms we expect the dynamic private sector to overcome the inflationary impulse from excessively accommodative fiscal and monetary policy, and although forecasting results from specific companies is not our focus, the ‘hyperscalers’ had already told us they planned on spending ~$200 billion on capex in ‘24. Said differently, the probability of an uncomfortable inflation report was marginally higher than a soft employment report and far higher than the Gen AI boom losing momentum anytime soon. Sure enough, the Godfather of Gen AI didn’t disappoint and during overnight Wednesday and early Thursday trading it appeared the battle of the productivity boom against the policy bust was being won by the dynamic private sector. A one-day risk-off following the release of the FOMC meeting minutes on Thursday was reversed on Friday, and we finished our week with lunch with our friend and former neighbor Dan Ives, he sounded like Al Pacino in ‘Scent of a Woman’: Gen AI is just getting started.

The data flow was light, weaker than expected existing and new home sales followed the prior week’s softish housing starts report but April durables, initial claims for the BLS establishment survey week, Kansas City Fed manufacturing survey and S&P Global preliminary May manufacturing and services PMIs were all stronger than expected. It is still early to make much of a call about 2Q growth but the Atlanta Fed GDP and PCE tracking models at 3.5% and 3.3% are right on the trend of underlying domestic demand for the last 3 quarters with no reason for us to think growth is slowing.

The only consequential macro event of the week was the minutes of the late April/early May FOMC meeting. Some were quick to dismiss the tone given the friendly ‘big four’ reports (ISM manufacturing, payrolls, CPI and retail sales) that followed the meeting, but that is not the correct read. The minutes are heavily redacted. The Board and staff likely convinced Chair Powell his presser did not capture the tone of the meeting. Nevertheless, by Friday the market had returned to its focus on the technology sector and the bear steepening of the Treasury curve that led to a 4.4% drop in the regional bank ETF (KRE) was no obstacle to a 3.4% increase in the S&P information technology sector.

Next week is Treasury ‘belly week’, with $183 billion of 2s, 5s and 7s supply with the yield curve even more deeply inverted than last month’s auctions. These belly auctions have tended to require a modest price concession, however longer maturity USTs have frequently backed up even more than the belly during these auctions. Offsetting Treasury supply is the first month of the reduction in the QT Treasury redemption cap from $60 billion to $25 billion and Treasury begins their buyback program for illiquid securities. These are modest factors that will improve liquidity, but as we will discuss liquidity is plenty ‘abundant’ already. The question is whether banks will help Treasury place 5s and 7s, 2s near 5% are good value in our view. We suspect next week’s data cannot change the market expected policy path, for that we will have to wait for the following week’s employment data. In this week’s note we will cover an important speech from Fed Governer Waller, offer first look at the post-election policy outlook and discuss our takeaways from our field trip to NYC.

Keep up with our instant updates during the trading week.