Until They Break Something

The Fed tail risk is getting fatter, the data does not justify 75bp in September

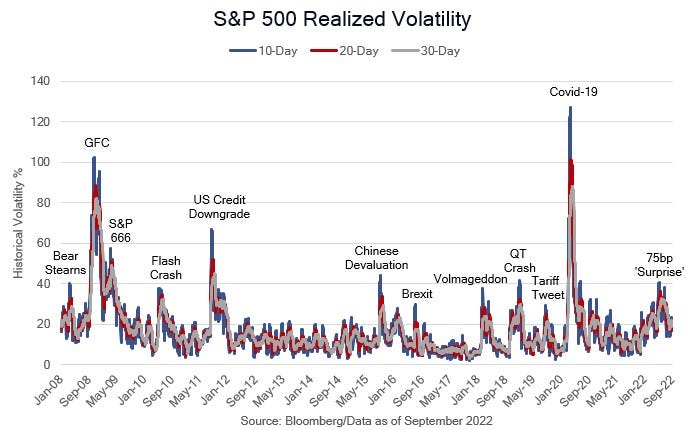

Time for Caution Federalies

Economic activity, labor market and inflation and expectations data released since the July 27 FOMC meeting does not justify another ‘unusually large’ 75bp rate hike. We viewed the August employment report as optimal from a slowing the pace of hikes perspective, however markets remain concerned about the Fed driving the economy into a ditch dragging the rest of the world amidst an energy crisis with it. If the FOMC decides to proceed with another 75bp rate hike, after declaring the ‘frontloading’ process complete, they risk 1987 level cross-asset level macro instability. That may sound uncharacteristically hyperbolic; however, while at Guggenheim Securities we warned in a note titled ‘Echoes of ’87’ written in late January 2018, that monetary policy, a trade war, tax reform, an energy price collapse and subsequent recovery in earnings that led to a 50+% rally in the S&P 500, were similar to 1987 and a market crash was increasingly likely. We had two that year triggered by sharp increases in real rates in the belly of the Treasury Curve, Volmageddon in February and the QT Crash in 4Q18. During the Fed’s front-loading process in 2022 we had the mother of all taper tantrums, we have now had a decent size aftershock led by a 50bp spike in 10-year real rates (TIPS) with the S&P 500 meeting our price target of a 50% retracement of the rally off the lows, albeit in a shorter time frame than we expected. What really should concern the FOMC is not the US Treasury, credit or equity markets — the potential source of extreme macro instability is the currency market. Since the aftershock began, the Japanese yen has fallen to its weakest level since the Asian currency crisis in August 1998, to below 140. The Euro is at its weakest level since its origin in the early ‘00s when it was below parity. The pound sterling is at its weakest levels since the Plaza Accord in 1985, and while the Chinese yuan is above the levels it touched towards the end of the trade war, the rate of decline is rapid and chart patterns project to the trade war lows above 7. While monetary policy is the clear catalyst, there is a large, underappreciated change in the economics of a weaker exchange rate for export dependent China, Germany and Japan. The dollar is now a petrocurrency, and its recent strength is exacerbating the energy crisis.

Recent FOMC participants’ comments on the dollar as helping their inflation fight exemplify the focus on first order risks and ignore the implications of forcing energy exporters into either responding with similar sized policy tightening despite larger contributions from supply-side inflation, or even faster exchange rate devaluations. The European Central Bank and Bank of England appear likely to choose keeping up with the Federalies, while the Chinese and Bank of Japan appear likely to choose exchange rate devaluation. This could become a global source of instability were Chinese outflows to force the sale of reserves like in 2015, or if extreme yen weakness finally breaks the BOJ’s yield curve control. During our holiday weekend the PBoC reduced exchange rate reserves and set their longest run of strong yuan fixes since 2019 during the trade war. We think equity investors, and strategists even more so, generally get the dollar wrong, in periods of strength the focus is on the negative revenue translation and not the impact on cost of goods sold (input prices). Perhaps understandably, given the product focus of street research departments (equity, interest rates, exchange rate strategists and economists all encouraged to stay in their own lane), as well as the focus on first order effects, periods of exchange rate instability, like prior to the Crash of ‘87, tend to get ignored until they reach crisis level. In the rest of the note, we will work through the data since the last meeting and explain why we think it justifies a slower pace of tightening. Our concerns about macro instability are not our base case; we still expect the equity market to stabilize and recover from the mother of all taper tantrums. However, it is time for the Fed to proceed cautiously, and with little capital markets experience on the FOMC and based on recent Fed speak, the tail risk is looking fatter than normal. If you followed our call for an aftershock and added equity market hedges, we would cover part, but not all, of your short.