Unstable Equilibrium

Deepening inversion, earnings recovery, FOMC preview

Please note next week’s note will be delayed until Monday morning. We will likely release a brief note on Wednesday following the FOMC meeting.

Unstable Equilibrium

The equity market, and the economy, are in an unstable equilibrium that seems likely to persist for another quarter, perhaps through the balance of the year, but not indefinitely. We expected the equity market to retrace last year’s 27% decline by 3Q23 due to four factors: disinflation (The path from 9 to 4, turns out 3); a favorable liquidity environment until a debt ceiling deal; earnings resilience due to the history of inflationary recessions when nominal growth continued to expand even as real growth contracted; and the ’94-’95 analog when the equity market rallied 22% from peak tightening expectations in November ’94 through the confirmation of a pause in June ’95.

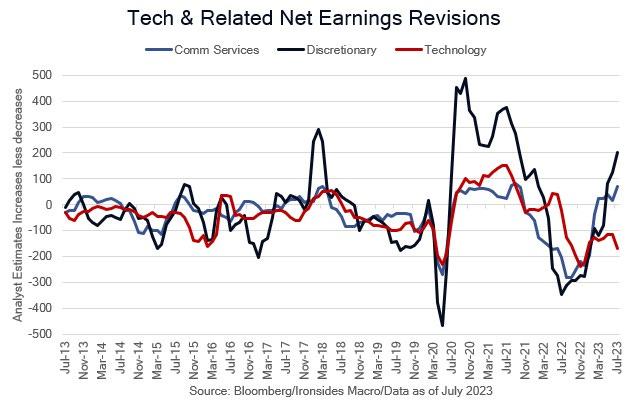

The disinflation process exceeded our expectations, as we forecasted all items CPI at 4% in June, instead it is 3%. The progress in headline (all items) inflation is likely complete; although core is lagging headline, it is on a disinflationary path through 1Q24 primarily due to lag impaired shelter inflation. Disinflation is unlikely to be the driver of markets it was in 1H23, however, at a minimum it should end the Fed’s tightening cycle. The liquidity regime was not as favorable as we expected through 1H23 due to the policy-driven balkanization that stressed the banking system and led to a sharper contraction in bank credit than we expected. However, once the Financial Responsibility Act was passed, the rebuilding of the Treasury General Account has not drained as large a quantity of reserves from the banking system as we anticipated. Consequently, the liquidity environment is better than we expected in 3Q. While only 17% of the S&P has reported, a continuation of the 6.3% earnings surprise rate would turn earnings positive and end the earnings/real GDI recession. Consumer discretionary (the ‘leadingist’ of early cycle sectors) earnings revisions continue to increase sharply, thereby increasing the probability that the GDI/earnings recession has ended.

Similarities to the ‘94-’95 aggressive rate hike cycle include a burgeoning capital investment boom led by the technology sector that wasn’t particularly vulnerable to higher rates but likely benefited from stable prices (low standard deviation of 3-4% CPI) and a banking system carrying low levels of credit risk. The big difference, and reason we believe the earnings recovery is unstable, is the deep inversion of the yield curve. The 3-month/10-year and 2-year/10-year curve flattening during the Fed’s 300bp of rate hikes from a zero to 3% real policy rate in ‘94 that led to fixed income chaos — with the Orange County bankruptcy the poster child for the disruption — was only ~70% of the curve flattening this cycle. Neither of those curves actually inverted in ‘94, while currently they are -159bp and -101bp respectively. Meanwhile the 2-year/10-year real rate (TIPS) curve is making new lows at -152bp, while the breakeven inflation curve steepens as investors price a bottoming in the disinflation of headline CPI. Nonfinancial corporates and households have generally termed-out their debt and avoided excessive leverage, consequently the Fed’s balance sheet driven rate suppression of longer-term rates implies these crucial sectors are not under much pressure from the Fed’s rate hike cycle. Small and medium banks, as well as small businesses, tend to have shorter duration liabilities, consequently the rate hikes are having more impact and are showing signs of pressure. The small bank and business higher cost of capital has not risen to the level of impacting consumption or employment broadly, in part due to continued strong nominal growth, at least not yet.

This brings us to next week’s Fed meeting. In our view, the deeply inverted curve needs resolution prior to 2024’s maturity wall for commercial real estate, leveraged loans and rising cost of deposits for banks. There is every reason for the Fed to stop hiking, however, if inflation stalls above 3% it will likely require either a banking crisis or pressure on small business to intensify to the level that causes an increase in the unemployment rate. There is another path to curve disinversion, which is a restructuring of balance sheet contraction (QT), but that implies bear steepening, a much less favorable environment for equities, Treasuries, commodities, and emerging markets. In other words, risk off. For now, we expect the unstable equilibrium to persist and the S&P to complete the ‘94 analog by rallying to 4800. A rally beyond that level likely requires more disinflation than we expect, a series of 0.2% monthly prints in core CPI and PCED would likely be sufficient. Expansionary fiscal policy is working at cross purposes with monetary policy, as in the ‘70s, however, there is increasing evidence that China, Asia and Germany’s export dependent export economies are struggling badly, implying a second wave of goods disinflation is possible.