Unconundrum

BOJ defends YCC, Cyclical stocks discounting destocking completion, revisions rising

Unconundrum

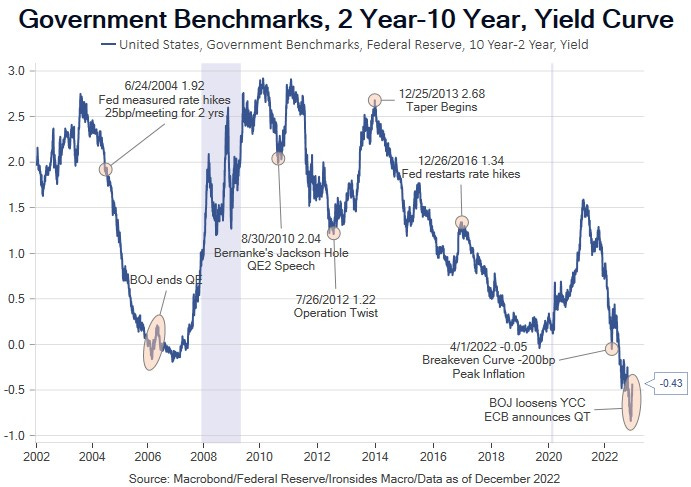

During a quiet holiday week there was one important macro development: the BOJ bought a record amount of bonds over the last three days in unscheduled purchases to defend the widened 50bp cap for 10-year JGBs, dragging the soft underbelly of the UST curve higher. In preparation for a meeting this week we looked at one- and three-month changes in global government bond yields, and three things jumped off our Bloomberg screen: The first was 50-60bp increases in European bond yields following the ECB’s QT announcement; second, the BOJ’s yield curve control band widening; and finally, the steepening of the UST curve. This brought to mind March 2006 when the Bank of Japan ended their initial quantitative easing program by draining 30 trillion yen ($305 billion USD) leading to disinversion of the 2s10s US Treasury curve. The Bank of Japan did not intend for the bulk of the bank reserves to get invested in USTs; however, their banking system was struggling with bad loans despite two rounds of recapitalization, one in the late ‘90s and another in the early ‘00s, following the twin bubbles bursting two decades earlier. The BOJ driven steepening did not persist due to continued buying from China, despite the June 2005 change in the Chinese currency regime from a hard to a crawling peg due to a surging trade surplus. Petrodollar recycling demand for USTs was also robust as the US was headed towards record energy deficits. In 2023, we expect the Bank of Japan to take additional tightening steps as a new regime unfolds with Haruhiko Kuroda’s retirement.

The US current account deficit is likely to be narrowing in 2023, unlike 2006 when it was widening, which should reduce foreign demand for USTs. The coming pause in rate hikes is likely to steepen the curve. However, a normalization of the yield curve that will take some time due to Fed holdings will continue to exert downward pressure on rates in the belly of the curve. Our expectation is that there will not be rate cuts in 2023, assuming they are not on a preordained path to a 5 1/4% policy rate and the passive ECB QT plan. We like steepeners, do not like the belly of the UST curve, 150bp real rates remain historically on the low side and -50bp term premium is unattractive. Still, outright 10-year Treasury shorts are likely to be frustrating in the first half of 2023 as inflation falls, the Fed pauses, and the recession debate rages on.