Uncle Milty is Smiling

A deep dive into the implications of Chairman Warsh's five task forces, fading headwinds from the four adverse demand shocks, and positioning changes

We strongly support Chairman Warsh’s five task forces objectives, like Chairman Warsh our criticism of what Treasury Secretary Bessent calls ‘gain of function’ monetary policy began with the launch of QE2 in November 2010. Non-crisis long duration asset purchases (QE) and the abundant reserves regime were an overreaction to the deleveraging impaired growth following the financial crisis. The second order effects on the capital allocation process of the Fed’s expanded footprint are vastly underappreciated, particularly by the FOMC participants focused on volatility of repo rates. The wealth of the nation depends on returning the setting of the cost of capital to market participants, reducing the influence of FOMC participants.

Friedman’s Revenge

The bottom line: the sharp bear flattening of the Treasury curve, presumably due to a hawkish DOT plot that is living on borrowed time, as well as Chairman Warsh’s commitment to the Fed’s stable price mandate, like the reporters in the room, completely missed the implications of eliminating forward guidance, shrinking the balance sheet and shortening the duration of the System Open Market Account portfolio, integrating market prices into economic forecasting, and a greater emphasis of supply side economic analysis on their employment mandate and inflation forecasts.

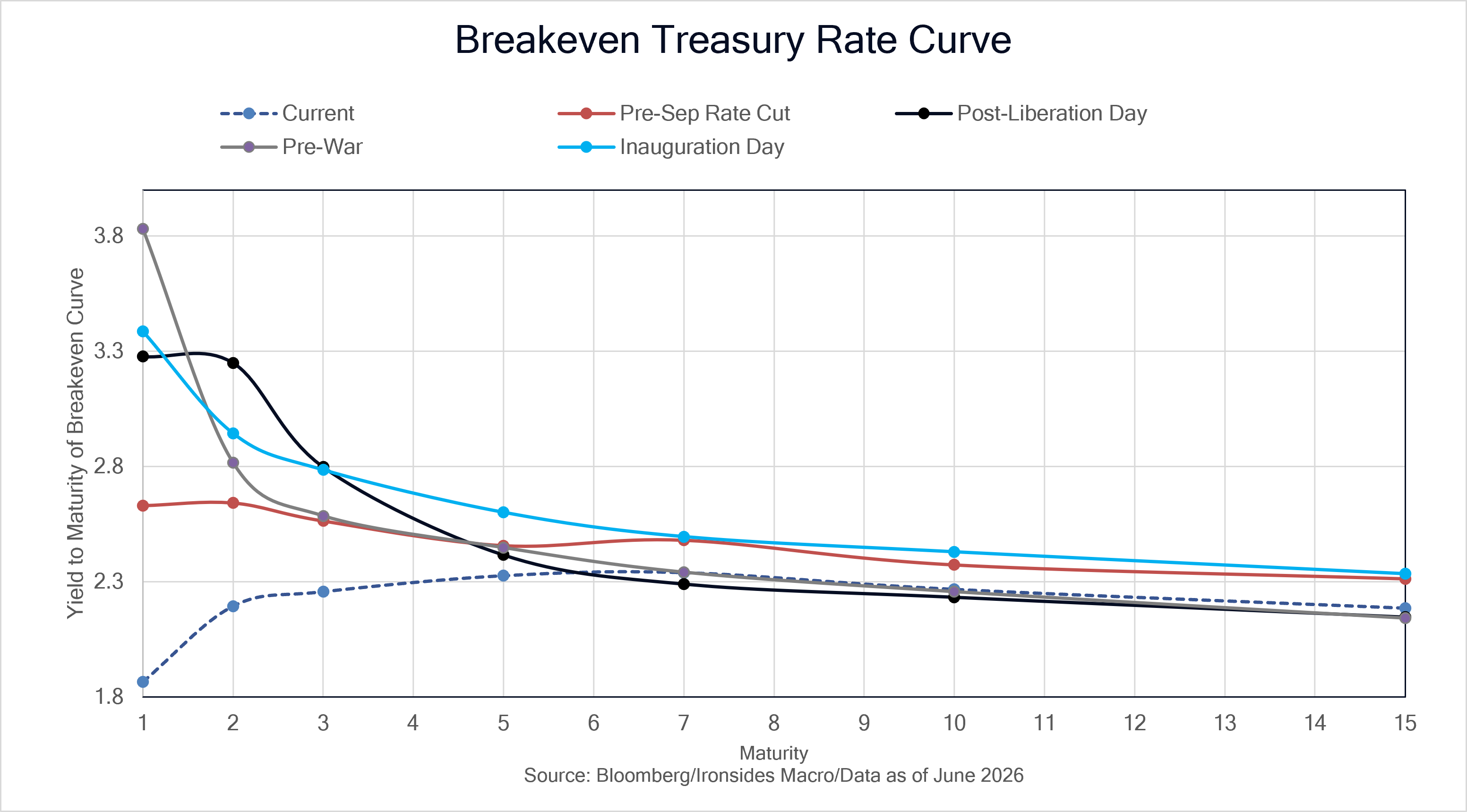

The Fed is not going to hike the policy rate. If our forecast for a resumption of disinflation later this summer is early or less likely, directionally incorrect, the Fed is more likely to respond by tightening using their balance sheet. 2s are a buy and the curve will bull steepen. We’ve been critical of the FOMC’s lack of capital markets expertise, and inability to integrate market signals into their forecasting process. A stark example was the reaction to Trump Administration tariffs, the market message was unequivocal, tariffs were a bigger risk to growth than inflation, yet the Fed focused on the first order price effect. The same is true with the Iran War and energy spike, our first chart below shows the breakeven inflation curve below where it was in September before they cut the policy rate.

The unspoken objectives of the five task forces are to reduce the Fed’s footprint and shift power to determine the cost of capital back to markets or what Hayek called the spontaneous economic order. This was an exceptionally consequential meeting, the most important since the launch of QE2 in November 2010 when the Bernanke Fed took a crucial step towards what Treasury Secretary Bessent called gain of function monetary policy.

“Financial market prices are probably the most important source of information to guide central bankers. But when all the financial markets are doing is reflecting back what we’ve said, then we’re taking the most important source of information and we’re being blind to it.” Fed Chairman Warsh

“Central bankers naturally pay close attention to interest rates and asset prices, in large part because these variables are the principal conduits through which monetary policy affects real activity and inflation. But policymakers watch financial markets carefully for another reason, which is that asset prices and yields are potentially valuable sources of timely information about economic and financial conditions. Because the future returns on most financial assets depend sensitively on economic conditions, asset prices--if determined in sufficiently liquid markets--should embody a great deal of investors' collective information and beliefs about the future course of the economy.”

What Policymakers Can Learn from Asset Prices, Ben Bernanke, 2004