Twin Peaks

Twin Peaks

Slowing inflation momentum, the natural rate, QT to the Max

Slowing Inflation Momentum

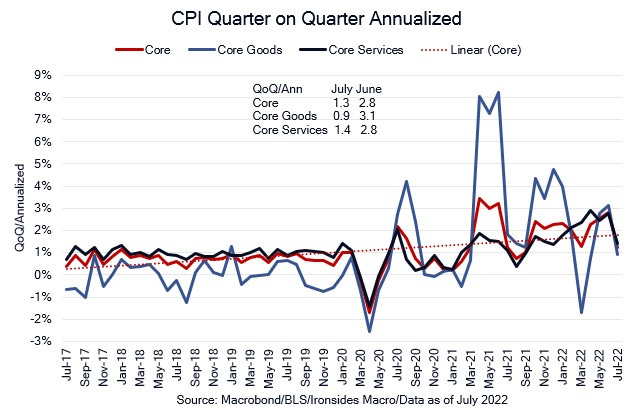

This week’s inflation reports were reasonably definitive in confirming our peak inflation outlook. In our recent note, Neutrality, we worked through three inflation themes. First, the inflation soft patch in 3Q21 was likely to bias the year-on-year inflation measures higher. Second, there was a preponderance of evidence that food, energy, core goods and even core services inflation had peaked. Finally, inflation was likely to stall at an uncomfortably elevated level of ~4%, in 2023. While base effects have little to no impact on capital markets, they are important for political markets — as evidenced by the Administration characterizing inflation as zero based on the monthly change and their opponents focusing on 8.5% annualized CPI. We heard a shocking (but from a contrarian sentiment perspective encouraging) number of takes on financial television to the effect that inflation was still high, wait for the Fed pivot to deploy cash, even as equities and the front end of the Treasury market rallied, and the dollar fell. Momentum, or rate of change, moves markets and here the news was all good. The quarter-on-quarter annualized all items CPI slowed to 5.2% in July from 9.2% in June. We knew that energy prices had fallen, consequently what really positively surprised the markets was a drop in the quarterly core CPI annualized rate to 1.3% from 2.8%, core goods to 0.9% from 3.1% and most importantly, core services 1.4% from 2.8%. Even shelter inflation eased to 4.6% from 4.9%. The same pattern was evident in PPI where total final demand quarterly annualized slowed to 5.3% from 9.5%, core to 5.3% from 9.0% and core excluding trade services to 3.8% from 4.9%. The effect of the dollar, clearing supply chains and rebalancing from goods to services was even more pronounced in import prices. Ex-fuel import prices peaked in March at 7.7%, in July were 4.1%. Further down the supply chain, China reported July manufacturing PPI at 0.9% from a peak of 10.8% in October 2021. The broad-based easing of price pressures from direct pandemic effects (goods), the Russian Invasion (energy), and pandemic fiscal and monetary policy mistakes (services and housing), left little doubt the economic rebalancing process is progressing. While our recent outlook to the effect that we passed peak inflation positions us as an optimist, that was not always true. Here is a quote from our 2021 outlook note published in December 2020, prior to the surprise Georgia Senate elections that led to the additional $1.9 trillion fiscal spending bonanza that threw lighter fluid on a campfire.

The pandemic was an inflationary shock, while the financial crisis was a deflationary shock.

2021 Outlook: Creative Destruction

Our 2023 outlook for stubborn inflation due to the combination of an undersupplied energy market, deglobalization ending decades of goods deflation, the Fed’s passive balance sheet tightening continuing to misallocate resources by suppressing longer rates, and fiscal policy impairing supply, will be an issue for markets, in 2023. The worst of the shock is over: peak tightening expectations, like November ‘94, occurred at the June FOMC meeting when they accelerated the size of hikes to 75bp. Pivot is the Wrong Word, the turning point for markets comes far before the Fed acknowledges the storm is over. Equities have had a big run off the lows (50% retracement) and momentum looks stretched, but our confidence in our outlook that the second half is likely to be a mirror image of the first was increased by the July inflation data. We have clearly passed the twin peaks of the inflation shock and monetary policy tightening expectations and our framework is far from widely accepted. This makes us cautious, about getting cautious.