Trouble with the Curves

Trouble with the Curves

Uncooperative Payrolls, widening policy gap, bear flattening and small banks

This week’s note is a brief update, we are focusing on our macro thematic annual note

Barron’s Managing Editor Lauren Rublin interviewing Saira Malik, CIO of Nuveen and Barry Knapp, Ironsides Macroeconomics

Barron's Reading the Tea Leaves

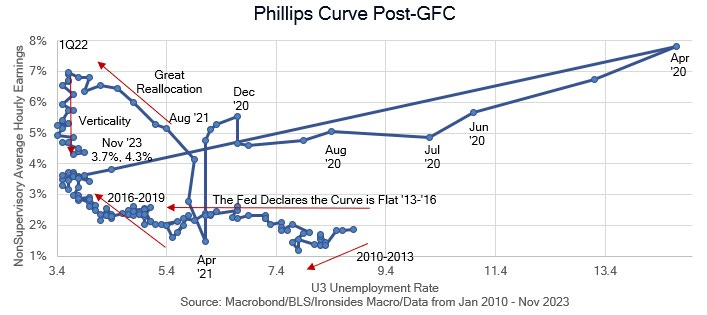

Trouble with the (Beveridge and Phillips) Curves

Friday’s November employment report was a setback for our FOMC rate cut forecast, but not our expectation that the equity market will struggle in early 2024. Total nonfarm and private payrolls were in line with consensus, although there was a negative revision to the prior two months for the 10th time in 2023. Job creation was concentrated in state & local governments and healthcare, in other words non-economically sensitive sectors. The monthly change in wage growth accelerated marginally, as did the work week and participation though not in the prime age (25-54) cohort. The shocker was a surge in employment in the household survey that reduced the U3 unemployment rate to 3.739% from 3.879%. The strong relationship between the Conference Board’s labor differential that has been weakening decidedly since July and the BLS Survey broke down in November, we expected a 4% or greater U3 rate. We strongly suspect changes in seasonal hiring patterns corrupted BLS seasonal adjustment factors and the drop will be reversed in coming reports. That said, the FOMC meets this week and participants will be writing down their forecasts for inflation, employment, growth and the policy rate. The divergence between the FOMC’s YE24 policy rate forecast that was 5.1% in September and market expectations roughly 100bp lower seems likely to make potential buyers of $50 billion of 3-year USTs and $37 billion of 10s on Monday as well as $21 billion of 30s on Tuesday skittish. Before you are tempted to dismiss the Summary of Economic Projections (SEP) forecasts, in September ‘22 and September ‘23, hawkish forecasts were catalysts for significant cross asset risk-off events.