Tightening Financial Conditions

Disorderly Disinversion, Rate Sensitivity, The Petrodollar Doom Loop, Jackson Hole Preview, Over? Did you say the risk-off episode is over?

We may delay next week’s note until Sunday to enable us to read the Jackson Hole papers presented on Friday and Saturday and provide you with our thoughts.

Disorderly Disinversion

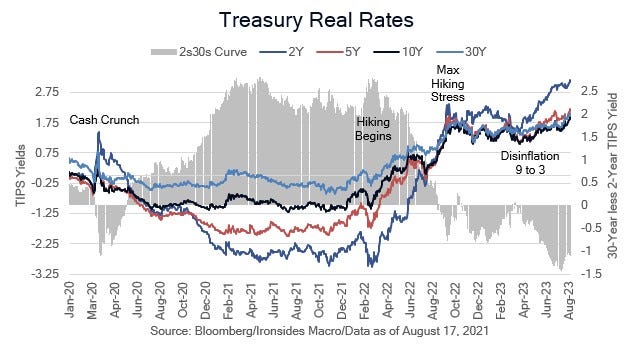

As 10-year Treasuries (USTs) decisively broke above the October ‘22 closing high of 4.24% and real 10s (TIPS) surged towards 2%, their highest level since the financial crisis, the explanatory narrative evolved from increased Treasury supply and reduced foreign demand to stronger growth. Our long-standing view is that since the global savings glut, when China and Japan accumulated large UST positions to suppress their exchange rates, and later due to QE, the market implied growth outlook is a tertiary factor in determining real rates. While retail sales decidedly beat consensus forecasts, as previewed last week, the August NAHB Housing Market Index slipped back to the 50 boom/bust line, much weaker than expected, July housing starts were in line, the first two August regional Fed manufacturing surveys were mixed, while July industrial production was strong. The Atlanta Fed GDP Now tracking estimate jumped after retail sales, but we view this indicator as noise at this point (1 month of data) of each quarterly cycle. The control portion of retail sales (ex-autos, gas & building materials) is roughly 20% of personal consumption expenditures (PCE), we have no data on services (2/3’s of PCE), nothing on trade or capital investment. We do think the gross domestic income/earnings recession is ending, but the macro and micro (retailer earnings) data this week did little to change our view. Another way to illustrate this point is with the NY Fed’s weekly index (WEI), here is their commentary explaining the weekly decline.

“The decrease in the WEI for the week of August 12 (relative to the final estimate for the week of August 5) is due to falls in steel production, tax withholding, consumer confidence, railroad traffic, and fuel sales, which more than offset increases in retail sales and electricity output and a decrease in initial unemployment insurance claims.”

What was significant, and likely played a larger role in the continuation of the real rate bear yield curve steepening, was yen and yuan exchange rate weakness. Following a round of decidedly negative Chinese industrial production, fixed asset investment, retail sales and new house prices, as well as struggles with a major real estate developer and nonbank credit provider (trust manager), the PBoC intervened to slow the decline in the yuan. The stale June Treasury International Capital Flow report showed China continuing to reduce their holdings, and selling dollars to support the yuan is a clear signal they have more USTs for sale. Given that Treasury Secretary Yellen’s best customers — the Fed, banks and export dependent Asian sovereigns —are better sellers, she needs lower prices to convince hedge funds to cover/unwind steepeners and unlevered pension funds, money managers and US households to extend duration to absorb the extra $500 billion of coupon securities she has for sale after Labor Day.

There are two major events between now and Labor Day that could alter the outlook and potentially halt the unfolding risk-off episode. First up is the Kansas City Fed’s 2023 Economic Policy Symposium, "Structural Shifts in the Global Economy," Aug. 24-26. The second is an early employment week this month, with July JOLTS and the August Conference Board Labor Differential on Tuesday August 29 and the August Employment Situation report on Friday September 1. The first look at 2Q gross domestic income and the August personal consumption deflator report on August 30 and 31 could solidify the disinflation and improving growth narrative but are unlikely to significantly alter the outlook. On balance the Treasury market move is looking extended, but equities are lagging, implying until and unless the S&P gets closer to 4300, the velocity of the decline accelerates, and our measures of cross asset class risk increase, we would keep our powder dry. Later in the note we will discuss a macro doom loop that we would consider expressing through long energy and short banks.