The Soft Underbelly

Taper Tantrum aftershock risks, really low real rates, the dubious recession narrative, additional risks

Note to Readers: On August 26 we will be traveling to Portugal through Labor Day weekend. It is unlikely we will release a note the weekend of the Jackson Hole central banker conference, we will try to release a podcast with our thoughts. We will release a delayed note the following weekend after returning to Colorado.

The Mother of All Taper Tantrums, Aftershock?

In the 19th century when farmers harvested their crops, local banks demanded cash from the NY money center banks who called in margin loans from brokers, and the stock market frequently crashed. The seasonality of market volatility persists to this day; in our 38 years in the markets, we have had a front row seat for some tremendous volatility events as the leaves turned and winter approached. The Crash of ‘87, mini-Crash of ‘89, Iraq’s invasion of Kuwait in ‘90, Thai baht & Asian crisis of ‘97, Long Term Capital Management in ‘98, Tech bubble bursting in ‘00, 9/11, telecom bankruptcies in ‘02, and the mother of them all, Lehman bankruptcy in ‘08. Consequently, we cannot help but get jittery in late August so take this note with this in mind, this is our first cautious note in months.

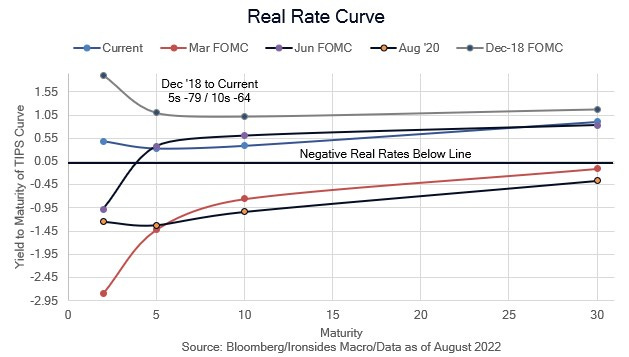

That said, there is no change to our outlook that the S&P 500 will retrace the 1H22 taper tantrum in 2H22. We view the generalized bearish narrative, namely that the Fed is going to drive the US economy into recession and earnings will plunge as in ‘91, ‘01 or ’08, to be a low probability outcome. We are concerned, however, about a taper tantrum aftershock originating with the ‘soft underbelly’, 5-10-year real rates (TIPS yields), which is the one QE/QT channel that is not appropriately priced given our expected monetary policy path. We are unmoved by the recent hawkish Fed speak, however at Jackson Hole the leadership could start talking about, talking about, active balance sheet management including outright mortgage sales. There are additional potential sources of macro instability: the euro, yen and yuan are all close to or at 2022 lows, the energy market remains undersupplied, and with the dollar evolving into a petrocurrency, these countries cannot devalue their way out of economic weakness as has been their strategy since World War II. In this note we will work through how we are not suggesting a large reduction in equity market exposure, instead we are going to offer trade suggestions that will both hedge in the event of a taper tantrum aftershock and could add alpha even if we have a benign volatility season.