The Recalibration Cycle

The Recalibration Cycle

QRA, FOMC, Payrolls, Big Tech Earnings and Slowing Growth

A Really Big Week

Next week’s lineup of economic data, corporate earnings and policy announcements is likely to set the tone for the markets through the balance of the summer. These include the June Job Openings and Labor Turnover Survey (JOLTS), 2Q Employment Cost Index (ECI), July Employment Report, Microsoft, Meta, Amazon and Apple earnings reports, the Quarterly Refunding Announcement (QRA), and the FOMC and Bank of Japan meetings. Together, they could return the markets to the 1H24 higher rates in the belly of the Treasury curve, the tech led equity market, and the strengthening dollar against the euro, renminbi and yen. More likely, though, they will increase concerns that growth is weakening, and Fed policy is too tight. Growth concerns, not non-monetary policy questions, were the primary factor in the 5% S&P 500 pullback over the last two weeks. This was to have been the quarter when we saw the recovery in earnings from the 4Q22 to 2Q23 8% contraction, however with 40% of S&P 500 constituents reporting thus far, technology and communication services sector earnings are growing 19% and 14% respectively, while industrial earnings are 0.5% below 2Q23 results, consumer discretionary are barely positive at 2.6% and staples are similarly soft at 2.2%. Revenue growth for the entire index is 4.1%, right at the level our works suggests negative operating leverage for high fixed cost sectors.

Thursday’s advanced estimate of 2Q24 GDP calmed nerves due to a solid 2.6% increase in real final sales for private domestic purchasers, implying solid underlying demand. We suspect GDP will be revised lower, equipment investment contributed 0.55% on an 11.6% quarterly annualized increase, however the Census Bureau released June Durable Goods Orders at the same time as the BEA’s GDP report and nondefense capital goods ex-aircraft shipments fell 2.3% annualized in 2Q24. It seems likely that domestic demand is more like 2%, down from 2.6% in 1Q24 and ‘23’s average quarterly pace of 2.9%. A 2% pace is close to most estimates of potential growth and would imply the monetary policy setting is overly restrictive.

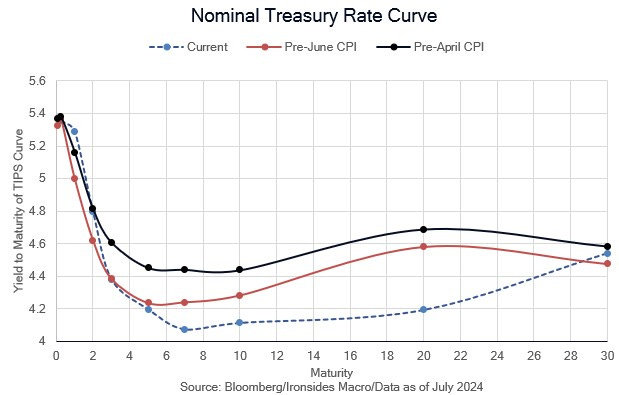

There have been some additional signs that policy is overly restrictive over the last two weeks, the short squeeze in small caps and banks in particular, and a similar squeeze in short yen positions, the first 2% daily drop in the S&P 500 in ‘24 and 11% drop in the Nikkei. The moves are reminiscent of the reaction to the September ‘22 third consecutive 75bp hike and 80bp increase in the terminal rate forecast in the Summary of Economic Projections (SEP) that was followed by the yen plunge and Ministry of Finance intervention, pound sterling ‘flash crash’ and gilt market turmoil and US mortgage-backed securities market plunge. At the core of the recent clutch of warning signs are growing concerns that growth and earnings are cooling fast, and the Fed should be cutting this week, not just talking about, talking about, ‘recalibrating policy’.

We will cover the policy events and growth outlook in this week’s note. Wednesday we will release an employment preview note along with our thoughts from the FOMC meeting and Treasury QRA and we will get back to our Saturday morning note schedule this week.