The Politics of Inflation

The Politics of Inflation

QT, Mortgages Matter, Treasuries Don't, Not as Hawkish as '94, Housing, The Value Factor and Earnings Season

Quantitative Tightening

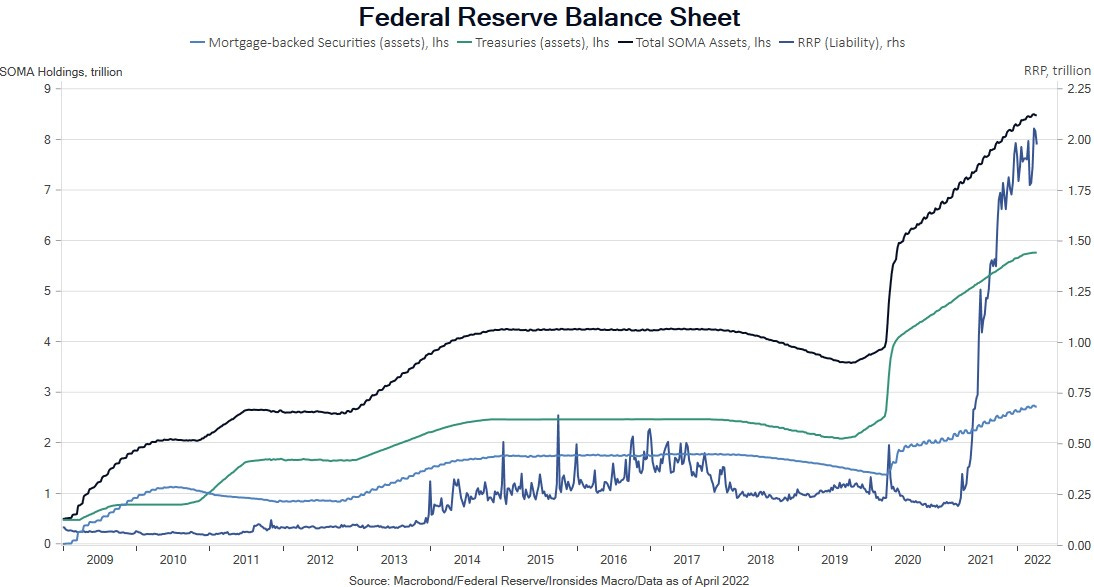

We went to great lengths in last week’s note, Inflation Backwardation, to attribute inversion of longer-term nominal yields to the expectations of lower inflation. Critical to our view is policy suppression of real rates (TIPS yields). If you were skeptical then, the 27bp steepening of the 2s10s curve following Vice Chairman nominee Brainard’s speech and the surprisingly detailed release of balance sheet reduction plans in the FOMC minutes, leaves little doubt that the stock of Fed holdings of Treasuries and mortgage-backed securities are suppressing longer maturity real and nominal rates. Our forecast of $100 billion per month comprised of $75 billion of Treasuries and $25 billion of mortgages with a four month phasing in to peak caps was more hawkish than the CNBC Fed Survey consensus. The Fed’s plan to phase in over 3 months to $65 billion of Treasuries and $35 billion of mortgages is close our forecast given the size of prepayments is likely to be below our forecast and well below the Fed’s cap at $20 billion per month. There are two impacts to consider, liquidity and higher real interest rates. The runoff of the Treasury portfolio is likely to have no impact on liquidity through at least 2022 given $1.7 trillion in the Fed’s reverse repo program and $3.8 trillion in reserves held at Federal Reserve Banks. We saw an estimate from former colleague Joe Abate of Barclays of $3.5 trillion of ‘surplus reserves’ and expectations of only a $400 billion decline in reserves in 2022. Additionally, maturing Treasuries are short term securities, there is little impact on the shape of the yield curve from organic runoff of the Treasury portfolio. Our interest has always been in the mortgage holdings and that is where the Fed’s plans get interesting. In short, balance sheet contraction is likely to increase fixed income volatility, steepen the yield curve, cool house price inflation and further exacerbate pressure on excessively valued stocks and sectors.