The Path from 9 to 3, now what?

The Path from 9 to 3, now what?

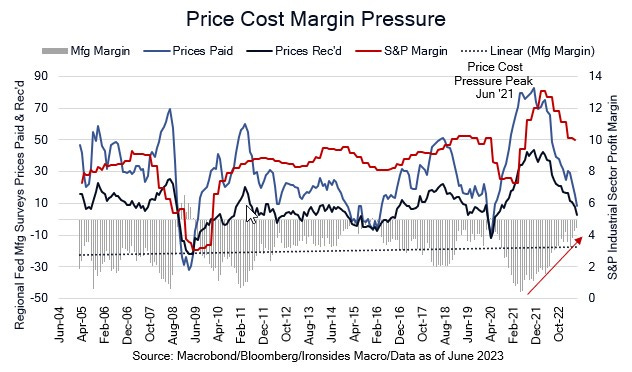

The end of the GDI recession, disinflation had little to do with monetary policy, an unstable equilibrium.

The End of the Easy Part

Our 2023 outlook was for a favorable environment for equities through the first half due to disinflation, liquidity and the ‘94 analog, when the market rallied ~20% from the peak of the hiking cycle in November ‘94 through the confirmation of a pause in June ‘95. As we will discuss in this week’s note, disinflation in All Items (headline) CPI is likely complete, though the most probable path for core inflation is to grind lower towards headline through 1Q24. We’ve spent a considerable amount of time on liquidity in recent months, and our broad measure — Fed assets owned outright less money deposited at the Fed by the Treasury (TGA) and reverse repo programs (RRP) — has slipped below $5 trillion, where it stabilized last October after falling throughout the first 10 months of 2022.

Liquidity is a conditional factor, not the dominant variable. The ‘95 analog, as well as the history of Fed tightening related corrections and recessions, implies an extension of the rally to 4800, in other words a full retracement of the ‘22 correction. When we wrote our 2023 outlook, earnings revisions were only beginning to bottom out and we didn’t know that we were in the first quarter of a contraction in real gross domestic income (GDI) driven by the private sector operating surplus (earnings). The 27% S&P 500 correction we were characterizing as the ‘mother of all Taper Tantrums’ (a Fed policy tightening related correction), may have in fact been a recession related correction given the two quarters of negative real GDI and the size of the pullback falling midway between the median (24%) and average (30%) of post-war recession related corrections. The timing of the low was 3 months early, but not unprecedented. Earnings season over the next three weeks should offer substantial evidence as to whether the real, but not nominal, GDI and earnings recession is ending. We will be watching industrials, technology and consumer discretionary earnings and margins particularly closely given the persistent uptrend in earnings revisions in those sectors.

The fly in the ointment, and obvious risk, is the extreme yield curve inversion with only similar episodes in 1973, 1979 and 1980. During the aggressive ‘94 rate hike cycle the 3m10y curve flattened from 250bp to a still positive 50bp, a far more benign outcome than this cycle’s flattening from 150bp to -160bp. Due to deposit betas, which is the rate of change of banks cost of goods sold relative to front end rates, the impact of the deep curve inversion is the proverbial slow moving car crash. We will learn more this week from bank earnings. Net interest expense is expected to increase sharply, leading to net interest margin pressure. Earnings revisions have plunged through the quarter. Small and medium banks have no options other than shrinking assets and this is reflected in rapid deceleration of bank credit growth. We expect very downbeat guidance. Three of the largest banks kicked off earnings season Friday and the reaction even to these banks with some of the ‘stickiest’ deposits was less than enthusiastic. Credit is not the issue, household and large nonfinancial corporate balance sheets are pristine, the issue is profitability or lack thereof. We will reconcile our favorable view of economically sensitive cyclical sectors, and negative outlook for financials later in the note. While these views might seem incongruous, there is an explanation, however in the intermediate term the pressure on banks creates an unstable equilibrium that is likely to require a monetary policy response.