The Natural Rate

Policy remains accommodative, balance sheet in the background, growth is slowing but not slow

Note: This week’s note will be delayed until Monday, wish us luck in our annual member guest golf tournament.

Blunt Instrument Credibility

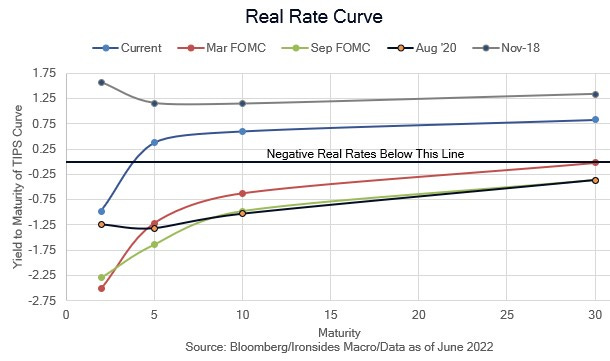

The major changes to the Fed’s policy path were a 75bp hike, an increase in the summary of economic projections (SEP) guidance to theoretically restrictive policy in ‘22 and ‘23, and no change in the balance sheet plan. The FOMC consensus forecast is only theoretically tight because the benchmark is the elusive neutral rate (or as we prefer, natural rate). During the aggressive February ‘94 to ‘95 tightening cycle, the Fed raised the funds rate from 3% to 6% with CPI stable at 3% through the process. These rates were not just theoretically restrictive, real rates benchmarked to realized inflation increased from 0 to 3% and despite Chairman Greenspan’s concerns in May ‘95 they may have overdone preemptive policy tightening, the economy was on the verge of a real capital investment boom. In today’s post-meeting presser, Chairman Powell said the bottom line on the SEP is that ‘participants want modestly restrictive policy by year-end’. We are squarely in the inflation has peaked camp, however, a 3.4% policy rate with the bloated balance sheet continuing to exert pressure on the back end of the rates market will not be modestly restrictive, it will remain accommodative. The June FOMC meeting was neither a Draghi ‘whatever it takes’ moment or Vocklerism, however, they did regain some lost credibility from the 2021 monetary policy mistake. Unfortunately, the bigger culprit in turbocharging demand into massive supply shocks, the Administration and Democratic Party controlled Congress, isn’t helping inflationary expectations by proposing counterproductive policies like energy windfall profits taxes that would further impair supply. On the plus side, Congress is heading for leadership changes so their policy proposals are political slogans and are not likely to become legislation. Let’s skip to the bottom line, at current levels, stocks are cheap, mortgages are exceptionally cheap but the most important security in the global markets system, the 10-year Treasury, still has a negative term premium and consequently, is not cheap.