The Nascent Labor Market Recovery

The Nascent Labor Market Recovery

The May ADP report was a shocker, but not for us...

This morning’s May ADP employment report showed a 2.76 million decline, far fewer than the consensus forecast of 9.0 million. This is consistent with the second section of our report on Saturday, consequently we are republishing that section and making it available to both free and paid subscribers ahead of Friday’s May employment report from the Bureau of Labor Statistics.

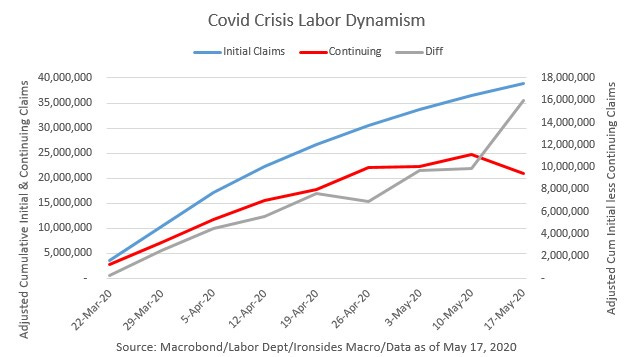

On Friday, the Bureau of Labor Statistics (BLS) will release the May employment situation report. Recent incoming data hints that by June, total payrolls may turn positive, albeit following the sharpest decline since the Great Depression. The trajectory of the recovery is critical, reports this week on jobless claims and the Conference Board’s May survey pointed to a much quicker than consensus rebound. From mid-March through mid-May, there was an increase of 36.8 million initial jobless claims from the February baseline of 210,000 per week. This is the number that grabs the headlines; however, adjusted continuing claims are 17.4 million lower than the cumulative increase in initial claims. In the latest reporting week they declined by 4.9 million while consensus expected a 600,000 increase. Additionally there have been reports that ~2/3’s of workers on unemployment insurance have seen their incomes increase due to the expansion of eligibility (notably the Gig economy) and benefits. The spread between initial and continuing claims implies there is considerably more hiring than the 38 million newly unemployed narrative would lead you to believe.

Figure 1: Last week’s sharp drop in continuing claims was the most encouraging economic indicator since the crisis began in March.

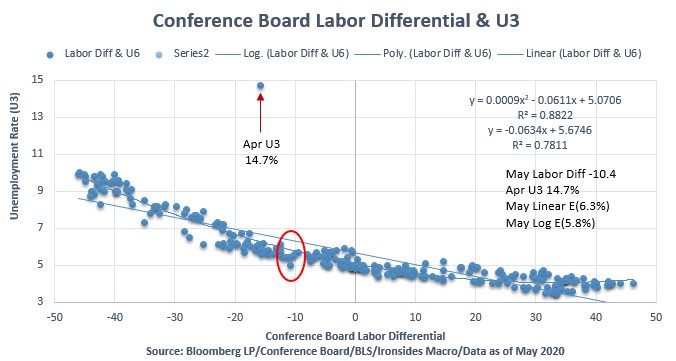

The Conference Board’s May consumer confidence survey was another positive labor market data point in that the labor differential - respondents describing jobs as plentiful less those who described jobs as hard to get - improved to -10.4% from -15.7% and +32.6% in February. While the drop appears significant, the relationship with this survey and the BLS household survey that derives the U3 unemployment rate has been exceptionally strong and the current reading is consistent with a 6% unemployment rate. Additional evidence of labor market dynamism includes:

1) The jobs openings and labor turnover survey (JOLTS) report of 5 million hires in March.

2) The large majority of newly unemployed responding to the April BLS special question that they believed their status was temporary.

3) The much sharper drop in employment to population relative to participation rates that implied the majority of the new claimants were not looking for work.

Taken together, it looks to us like workers themselves believe the unemployment rate will drop well below double digits in the months following the end of Covid-19 shutdowns. To be sure, the damage from these draconian policies could prove greater than workers believe; however, we have long believed labor market dynamism is vastly misunderstood. In the near term this implies consensus will be too pessimistic for an 8 million decline in Friday’s May Employment report. In another month the expiration of expanded unemployment benefits occurs right about the time when June payrolls are likely to turn positive, providing a test of whether public policy is supportive of, or counterproductive to, the private sector.

Figure 2: The relationship between unemployment rate and Conference Board survey has been remarkably stable since the late ‘90s, the improvement in May implies the majority of newly unemployed believe they either have a job to go back to or will not have an issue finding them. For now, we are going to give the benefit of the doubt to the workers rather than economists.

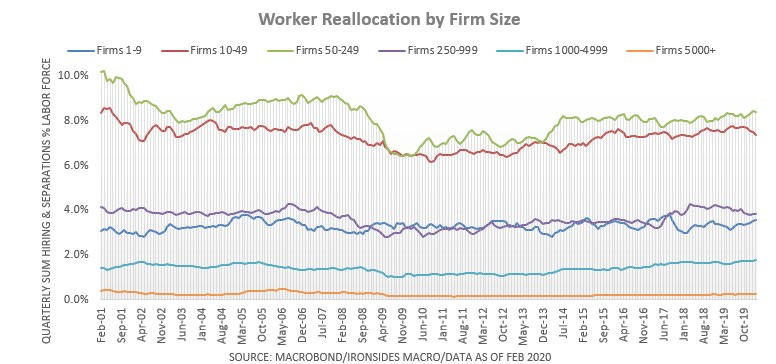

One additional note on ADP; the majority of the job losses in April and May have come from the least dynamic portion of the labor market by size, that is companies of 1000+ employees. Small businesses are the highest turnover, most dynamic, the losses according to ADP have been smaller. This hints that the policy response, PPP is helping, but more to the point these businesses are accustomed to dealing with adversity and are far more resilient than most economists and market participants believe.

Figure 3: Worker reallocation is the quarterly sum of hiring and separations, both voluntary and involuntary, expressed as a percent of the labor force. For the total private sector reallocation was 25% prior to the Covid Crisis. This chart breaks out turnover by firm size, large companies tend to contribute the least to labor market dynamism. The ADP report shows nearly twice as many job losses in large companies as small ones. This is consistent with our view that the US economy is far more dynamic and resilient than most market participants believe.

Barry C. Knapp

Managing Partner

Ironsides Macroeconomics LLC

908-821-7584

https://ironsidesmacro.substack.com

https://www.linkedin.com/in/barry-c-knapp/

@barryknapp

Reading List

“Showdown at Gucci Gulch, Lawmakers, Lobbyists, and the Unlikely Triumph of Tax Reform”, Jeffrey H. Birnbaum and Alan S. Murray

“A Great Leap Forward, 1930s Depression and US Economic Growth”, Alexander J. Field

“1493, Uncovering the New World Columbus Created”, Charles C. Mann

“Great Society, A New History”, Amity Shlaes

“The Second Machine Age”, Erik Brynjolofsson, Andrew McAfee

“Grand Pursuit, the Story of Economic Genius”, Sylvia Nasar

“The Rise and Fall of the Great Powers”, Paul Kennedy

“Capitalism in America, A History”, Alan Greenspan & Adrian Woolridge

“Diversity Explosion, How New Racial Demographics are Remaking America”, William H. Frey

“Clashing Over Commerce, A History of US Trade Policy”, Douglas A. Irwin

“Destined for War, Can America and China Escape Thucydides’s Trap”, Graham Allison

“The Constitution of Liberty”, F.A. Hayek

“Judgement in Moscow, Soviet Crimes and Western Complicity”, Vladimir Bukovsky

“1931, Debt, Crisis and the Rise of Hitler”, Tobias Straumann

My next book: “Nudge”, Richard H. Thaler & Cass R. Sunstein

This institutional communication has been prepared by Ironsides Macroeconomics LLC (“Ironsides Macroeconomics”) for your informational purposes only. This material is for illustration and discussion purposes only and are not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Ironsides Macroeconomics. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This material is for sophisticated investors only. This document is intended for the recipient only and is not for distribution to anyone else or to the general public.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Ironsides Macroeconomics undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Ironsides Macroeconomics, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Ironsides Macroeconomics or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Ironsides Macroeconomics or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Ironsides Macroeconomics or its affiliates may advise issuers of financial instruments mentioned. No liability is accepted by Ironsides Macroeconomics, its officers, employees, affiliates or partners for any losses that may arise from any use of the information contained herein.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules or regulations. This material is not to be reproduced or redistributed to any other person or published in whole or in part for any purpose absent the written consent of Ironsides Macroeconomics.

© 2020 Ironsides Macroeconomics LLC.